What Explains the Rise in CEO Age?

CEO age has risen sharply over the past several decades. In a recent NBER working paper, we document this striking trend, examine associated trends in career profiles and discuss potential explanations. The evidence suggests that changes in demographics, education, or tenure cannot by themselves account for the age increase. What can? Our results point to firms placing more value on diversified managerial experience in response to operating environments that have become increasingly uncertain and complex. We also establish that prospective CEOs broaden their skill portfolios as demand for generalist skills rises.

These results point to an important trade-off boards face: while older CEOs tend to run firms that are slower-growing and less innovative, their more risk-averse management style can also help navigate difficult market environments.

Mapping Out CEOs’ Career Paths

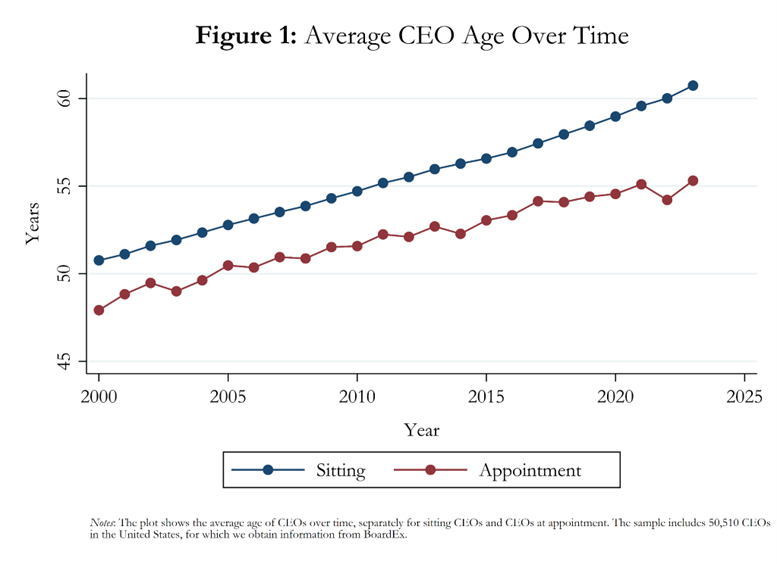

Using data on more than 50,000 CEOs from BoardEx, we document a consistent rise in CEO age since 2000. As shown in Figure 1, CEO age increased by more than 10 years, reaching 61 in 2023. Age at appointment also rose noticeably, from under 48 to 55 years, suggesting that the aging trend cannot be attributed solely to longer tenures, later retirements, or CEO entrenchment. Furthermore, we find that small firms are the primary drivers of this broad aging phenomenon. While CEOs of larger, listed firms are on average older than those of smaller, private firms, the latter group has converged toward the former over the sample period.

These age shifts have been paralleled by fundamental changes in how CEOs build their careers. First, most of the aging is accounted for by an increase in external experience outside the current firm. In contrast, internal experience has remained roughly unchanged over the past decades. Second, before assuming their CEO role, individuals today have transitioned through a greater number of positions, firms, and sectors than in the past. Third, the time spent in each position, firm, and sector has fallen since 2000. Fourth, even internally appointed CEOs now join their firms at a higher age and seniority level. Fifth, although aging has also occurred among lower ranked executives, these changes are more pronounced among CEOs, suggesting that broad external experience has become an increasingly important factor in CEO selection.

Standard Explanations Fall Short

In light of the many changes in the economic environment over this period, it is worth considering a range of potential explanations for the documented age patterns. Demographics can only account for a small fraction of the trend as CEO age has increased more than three times as fast as the age in the labor force as a whole. Furthermore we observe similar patterns across European countries despite widely different demographic trajectories. Moreover, measures of industry concentration are uncorrelated with CEO age at appointment, and other firm characteristics such as firm size and listing status leave the trend largely unexplained. The same holds true for CEO characteristics, including internal hiring rates, gender, and education. Finally, we demonstrate that our results are not driven by a rebound from the dot-com bust.

Uncertainty and Complexity Have Contributed to Higher Demand for Generalists

To interpret these patterns and formalize the role of changing market forces in shaping CEO appointments, we develop a many-to-one matching model of executives and firms. Executives vary in both age-adjusted ability (which peaks at mid-career) and experience (which increases in age), while firms differ in firm size and have multiple, hierarchically ranked positions. Our main result characterizes how an increase in the value of experience shifts CEO positions to older executives, especially at smaller firms. We also show that, under mild assumptions, CEOs in smaller firms are younger on average, consistent with the patterns observed in the data.

We scrutinize this hypothesis empirically by assessing the impact of two potential drivers behind the rising demand for generalists: economic uncertainty and business complexity. These forces can lead firms to seek leaders with generalist skills, which are more closely tied to accumulated experience than to raw ability. As executives require longer career paths to build such diverse capabilities, firms appoint older CEOs.

To establish causality, we exploit spatial variation in firms’ access to elite strategy consultants, specifically McKinsey, BCG, and Bain (MBB). The key idea is that in uncertain and complex environments, firms value leaders who can draw on experience across many industries and job functions. Elite consultants have gathered these generalist skills in an accelerated fashion and can, thus, act as substitutes for older, more experienced executives. As a result, the effect of rising uncertainty and complexity on higher CEO age should be strongest where (young generalist) consultants are in shorter supply.

We measure access as the flight time to the nearest MBB office, effectively leveraging variation from both office openings and air route expansions. Our analysis reveals that firms in high-uncertainty industries appoint significantly older CEOs when MBB consultants are harder to reach, with stronger effects among smaller firms where generalist human capital is more difficult to accumulate internally. We find very similar results when replacing uncertainty with measures of business complexity, including firms’ diversification across business segments and geographies as well as their exposure to trade-induced variation in economic complexity.

Executives React to Changing Skill Requirements

It is natural to ask how career-oriented individuals such as lower ranked executives would adapt to firms’ growing demand for generalists. We argue that prospective CEOs’ increased turnover across positions, firms, and industries may reflect a strategic response to the increasing premium for broad managerial capabilities. In the paper, we explore whether aspiring executives make sacrifices in order to increase their value to future employers. Specifically, we show an increased willingness to accept lower-level positions and reduced wage growth in the short run, betting that broader experience makes them more attractive CEO candidates in the future.

Drawing on data from the universe of LinkedIn accounts covering half a billion individuals, we document that CEOs appointed in recent years are indeed more likely to have gone through transitions towards less senior positions. Importantly, the patterns are not random. Individuals are more likely to increase their job mobility after a former colleague is appointed as CEO elsewhere, and this response is stronger among those who worked more closely to the newly appointed CEO. Taken together, the evidence suggests that both the demand and supply of generalist skills have shaped the rise in CEO age.

What are the Implications?

Older CEOs tend to manage firms with slower growth rates and less radical innovation, but also reduce firms’ risk exposure. Therefore, what might appear concerning for long-term economic dynamism may be a rational response to business environments characterized by heightened uncertainty and complexity.

Our results can explain why the age trend is most pronounced among smaller firms. Large firms can cultivate generalist skills internally through diverse assignments across divisions and functions, while smaller firms wind up recruiting executives who accumulated that experience externally. The lengthening of external career paths thus translates into older CEO appointments primarily at smaller firms.

Looking ahead, we see no obvious reason to expect the trend to reverse. Artificial intelligence (AI) may further increase economic uncertainty and complexity, strengthening the forces that have driven CEO age upward. At the same time, AI may disrupt the pathways through which generalist expertise has traditionally been acquired, while increasing the value of experienced decision-makers who can effectively leverage these technologies. The rising importance of generalist human capital thus reflects not only its resilience to automation, but also suggests that the patterns we document may prove persistent.

The working paper is available here.

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.