Measuring CEO Pay-for-Performance: Demonstrating Alignment with Shareholder Outcomes

Introduction: Why Pay-for-Performance Remains Contested

Demonstrating that executive compensation is meaningfully aligned with company performance and the shareholder experience remains one of the most important, and most debated, issues in U.S. executive pay decision-making and corporate governance in general. While boards, investors, executives, and proxy advisors broadly agree on the principle of “pay for performance,” there is far less agreement on how that alignment should be measured and evaluated in practice.

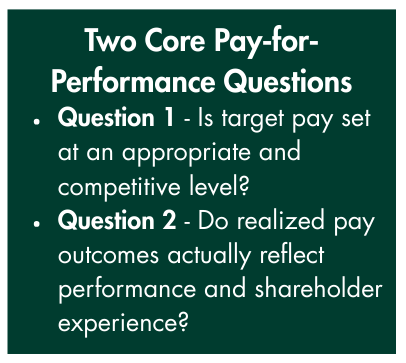

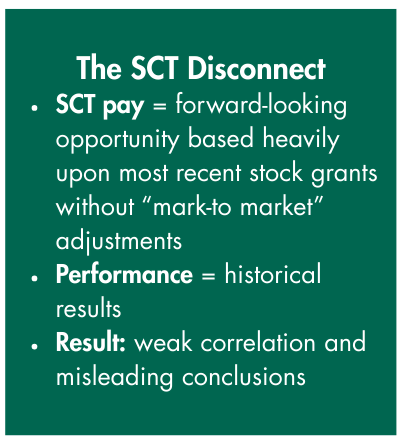

Two analytical challenges sit at the center of this debate. The first is determining a fair and competitive level of target compensation. The second, and more controversial challenge, is assessing whether the compensation ultimately earned by executives appropriately reflects company performance and shareholder outcomes over time. This Viewpoint focuses on the techniques used to evaluate pay‑for‑performance alignment—an area that remains highly contested. Traditional approaches to this analysis have relied heavily on grant‑date values for stock awards included in the Summary Compensation Table (SCT) pay, which reflect future opportunity rather than realized or realizable pay outcomes.

This Viewpoint argues that outcome‑based measures—particularly Compensation Actually Paid (CAP) and realizable pay—provide more credible and decision‑useful assessments of pay‑for‑performance alignment. While these measures are not without limitations, they better capture the economic value delivered to executives relative to shareholder returns and, when used thoughtfully, offer boards and Investors a clearer lens through which to evaluate executive pay outcomes than grant-date or SCT‑based analyses alone.

How Companies Currently Describe Pay for Performance

A significant majority of companies emphasize the importance of paying for performance in the Compensation Discussion and Analysis (CD&A) section of the annual proxy. This disclosure is typically holistic, combining qualitative narrative with quantitative discussion, and is separate from the SEC‑mandated Pay Versus Performance (PVP) disclosure.

The PVP disclosure, by contrast, is entirely quantitative and appears in a different section of the proxy. While stakeholders broadly agree on the importance of pay‑for‑performance alignment, there remains little consensus on how that alignment should be measured.

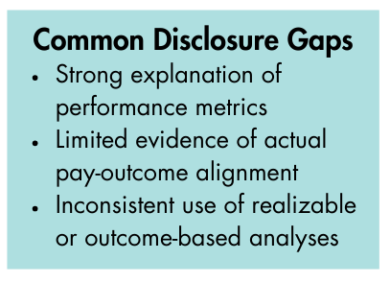

The lack of a generally accepted approach for measuring pay-for-performance alignment is further complicated by the wide range of disclosure companies use to describe pay-for-performance alignment. Most companies describe the rationale for their performance measures ¾ and in some cases the rigor of their performance targets ¾ but provide limited disclosure demonstrating how pay outcomes align with performance. Some companies use realized or realizable pay [1] analyses and supporting charts to illustrate alignment with shareholder outcomes, while others focus on “take-home” pay as evidence of alignment. These varying disclosure methods make it difficult to readily assess pay-for-performance alignment across companies.

SEC PVP: Intent vs. Reality

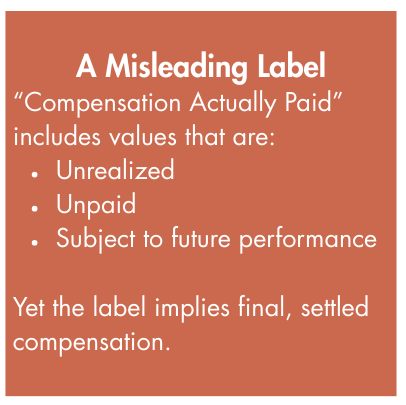

The SEC’s PVP rules, as mandated under Dodd-Frank, were intended to fill this disclosure gap by explicitly linking pay outcomes to performance. However, the significant number of detailed calculations required to reconcile SCT compensation to CAP, the rushed rollout of the requirement, and the subsequent inflexible interpretive guidance have led many boards to view PVP primarily as a compliance exercise rather than a decision-useful analytical tool. Compounding this perception is the mislabeling of CAP, a label mandated by Dodd-Frank, as a significant portion of the reported compensation amount is neither actual nor paid. This is quite unfortunate as our previous detailed research clearly shows a strong correlation between relative CAP and relative total shareholder return (TSR)[2]. We also believe that the CAP data, while not perfect, is a very good approximation of outcome-based pay that can be used for relative comparisons to a company’s peers and industry sector.[3] This method is arguably the best evidence yet that there is alignment between executive pay and the shareholder experience (i.e. total shareholder return).

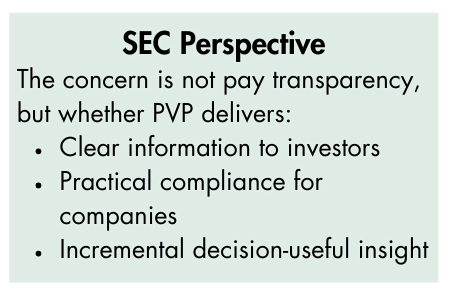

Growing SEC Skepticism Toward PVP Disclosure

It also appears that the SEC may be on the verge of rethinking or possibly suspending its PVP disclosure rules. In a speech given on February 16, 2026, SEC Chairman Cox referred to comments made at the June 26, 2025 disclosure roundtable about the complexity of the PVP rules noting that the complexity “should give us pause as it reflects the opposite of what an SEC disclosure requirement ideally should be—intelligible by a reasonable investor and practical for a company to comply, without the need for a cottage industry of ultra-specialized consultants. Unfortunately, all of the time and money spent on PVP disclosure has scarcely resulted in clear information to investors.”

The reality is the outcome-based compensation data (CAP) currently provided in the PVP disclosure is virtually impossible to replicate with the same degree of accuracy for a company’s peers, and if the SEC revamps this disclosure, at a minimum, it should require that outstanding performance awards disclosed in the Outstanding Equity Awards at Year-End Table include a footnote detailing the probable outcome of these awards.

Proxy Advisors and the Limits of SCT-Based Models

The proxy advisors’ pay for performance models up until now have generally relied on SCT compensation, which reflects the grant date value of long-term incentives, rather than outcome-based compensation—which reflects the actual number of shares earned and the updated stock price. Using the SCT for this purpose is deeply flawed and misleading. One of the proxy advisory firms has added two outcome-based tests to its pay for performance model this year to supplement its SCT compensation tests. As we have demonstrated through extensive research, there is very little correlation of SCT compensation to performance, as SCT compensation largely represents future pay potential whereas performance is based on past results. [2], [4]

Implications for Boards and Investors

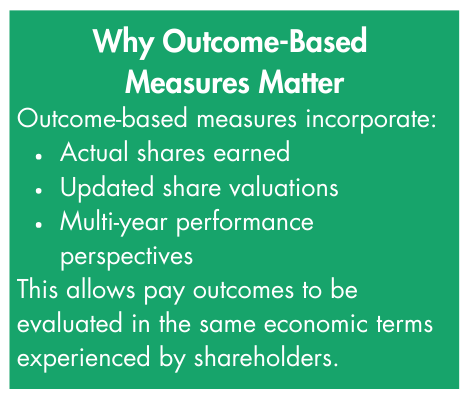

The ongoing debate over how best to measure pay for performance reflects a broader challenge in executive compensation: balancing simplicity, transparency, and analytical rigor while meaningfully capturing economic outcomes. Grant‑date and SCT‑based measures, while useful for disclosure and accounting purposes, are poorly suited to evaluating the relationship between pay outcomes and performance because they reflect forward‑looking opportunity rather than realized value.

Outcome‑based approaches—most notably CAP and realizable pay—offer a more informative perspective by incorporating actual equity earned, updated stock prices, and historical performance results over time. Although the SEC’s PVP framework has been widely viewed as too complex and compliance‑driven, the underlying CAP data nevertheless represents one of the best available approximations of outcome‑based compensation and has demonstrated a strong relationship to shareholder returns in relative comparisons.

Indeed, Vanguard has incorporated outcome-based measures in evaluating pay for performance in its proxy voting guidelines, and it is likely that other institutional investors are also relying on similar approaches to inform their voting decisions.[5]

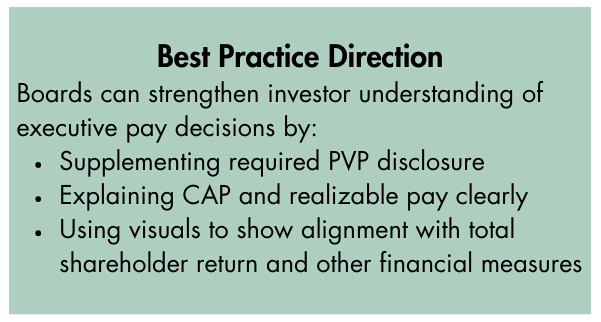

As proxy advisors begin to supplement traditional models with outcome‑based tests and large institutional investors increasingly rely on proprietary pay‑for‑performance methodologies, boards would be well served to proactively adopt and disclose more robust, outcome‑oriented analyses.

Supplementing required PVP disclosure with clear, contextual explanations of CAP and realizable pay—and visual demonstrations of alignment with shareholder outcomes—can enhance credibility, improve investor understanding, and strengthen the overall pay‑for‑performance narrative.

Conclusion: Toward More Decision-Useful Pay-for-Performance Analysis

Ultimately, no single metric perfectly captures pay‑for‑performance alignment. However, a thoughtful emphasis on outcome‑based measures represents a meaningful step toward more transparent, economically grounded, and decision‑useful evaluations of executive compensation.

As proxy advisors and institutional investors continue to evolve their methodologies, boards that proactively adopt and clearly communicate outcome‑oriented analyses will be better positioned to demonstrate credible alignment between executive pay and shareholder outcomes.

_______________________

1 Realized/realizable pay generally includes base salary, annual bonus, and long-term incentives granted and paid during the applicable performance period being measured to evaluate pay for performance, plus the estimated value of compensation still in-flight and subject to future performance. This includes unvested long-term incentives such as RSUs, PSUs, and outstanding unexercised stock options granted during the applicable performance period. These values can be estimated based on the current company share price and to the extent disclosed, the estimated performance factor for inflight PSUs.(go back)

2 SEC 2024 PVP Using CAP “Does CAP Continue to Demonstrate Strong Alignment with TSR in the Second Year of Disclosure? https://www.paygovernance.com/resource/sec-2024-pvp-using-cap-does-cap-continue-to-demonstrate-strong-alignment-with-tsr-in-the-second-year-of-disclosure/ Ira T. Kay, Mike Kesner, and Ed Sim (go back)

3 Demonstrating Pay and Performance Alignment: A Comparison of Compensation Actual Paid and Realizable Pay. https://www.paygovernance.com/resource/demonstrating-pay-and-performance-alignment-a-comparison-of-compensation-actually-paid-and-realizable-pay/ Ira T. Kay, Mike Kesner, Linda Pappas, and Ed Sim (go back)

4 Does the SEC’s New PVP Disclosure Facilitate Shareholders’ Assessment of Pay for Performance Alignment? https://www.paygovernance.com/resource/does-the-secs-new-pvp-disclosure-facilitate-shareholders-assessment-of-pay-for-performance-alignment/ Ira T. Kay, Mike Kesner, Linda Pappas, and Ed Sim (go back)

5 Vanguard Portfolio Management: Proxy Voting Policy Portfolio Companies.https://corpgov.law.harvard.edu/2026/02/26/vanguard-portfolio-management-proxy-voting-policy-for-u-s-portfolio-companies/ Carolyn Cross (go back)

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.