Aura Minerals Completes Feasibility Study for the Borborema Project and Increases Ownership Stake in Borborema Inc. to 100%

ROAD TOWN, British Virgin Islands, Aug. 30, 2023 (GLOBE NEWSWIRE) -- Aura Minerals Inc. (TSX: ORA) (B3: AURA33) (OTCQX: ORAAF) (“Aura” or the “Company”) is pleased to announce the results of the Feasibility Study for the Borborema Project (“Borborema” or the “Project”) located in Rio Grande do Norte, Brazil. Borborema will be an open-pit gold mine with anticipated production of 748,000 ounces (oz) of gold over an initial 11.3-year mine life, with additional production upside. The technical report (the “Technical Report”) titled “Feasibility Study for the Borborema Project, Currais Novos Municipality, Rio Grande do Norte, Brazil”, prepared by Aura will be filed by Aura on SEDAR+ and CVM within 45 days of this press release.

Following the completion of this positive Feasibility Study, Aura anticipates the commencement of full construction with an estimated construction budget of US$188 million. Additionally, the Company is reporting that Dundee Resources Limited, a wholly owned subsidiary of Dundee Corporation (TSX: DC.A), (“Dundee”) has elected to convert its 20% equity interest in Borborema Inc. into a net smelter royalty (the “Royalty”) of 1.50% on the first 1,500,000 oz of gold sold, and 1.00% on the next 500,000 oz of gold. Once the production threshold of 2,000,000 oz of gold has been reached, the Royalty will be terminated. Aura is now the sole shareholder of Borborema Inc., controlling 100% of its shares.

Highlights of the Feasibility Study and the Project:

- Robust Project Economics: Net present value (“NPV”) of US$182 million and after-tax IRR of 21.9% when using the weighted average consensus gold prices for the projected period of US$1,712 per ounce. At a US$1,900 gold price and considering US$100 million debt, the IRR is 51.9% and NPV of US$262 million.

- Competitive Costs: Life of Mine (“LOM”) all-in-sustaining costs (“AISC”) on average of $949 oz, including the royalty paid to Dundee (“Dundee Royalties”); if excluded, the AISC would be $923 oz, making it a solid first quartile project among the industry AISC curve. In the first 3 years of complete production, average AISC is $875 per ounce, including the new Dundee Royalties. Excluding such royalties, the average AISC would be $831 oz for such period.

- CAPEX: Total investment of approximately US$188 million with payback in 3.2 years.

- Initial Operating Life of 11.3 Years: Weighted average annual gold production is estimated at 65 koz, with an estimated LOM of 11.3 years, based on Mineral Reserves estimated in accordance with National Instrument 43-101, – Standards for Disclosure for Minerals Projects (“NI 43-101”). In the first 3 years of production, weighted average annual production is 83 koz.

- Strong Reserve Base: The Feasibility Study includes updated Mineral Resource and Reserve estimates under CIM and NI43-101 guidelines for the comprising Probable Reserves of 812,000 oz gold.

- Substantial Resource Profile with Upside for Future Conversion: Borborema’s Mineral Resources consists of 2,077 koz of Indicated and 393 koz of Inferred. Initial measures have already been undertaken to start obtaining the permits to move the road, and upon its successful relocation, Borborema has potential to convert in Mineral Reserves 1,265 koz of Indicated Mineral Resources (exclusive of the current Mineral Reserves), depending on future set of modifying factors, such as gold price, exchange rate and others.

-

Exploration Potential Remains: The ore body of the Borborema deposit remains open along strike and down dip. Aura believes the project will benefit from additional drilling both to extend the Mineral Resource’s footprint and also to add more contained ounces within the current envelope of mineralization.

Rodrigo Barbosa, President and CEO of Aura, comments, "Borborema is expected to contribute significantly to our overall production profile, and we are delighted to announce this highly accretive Feasibility Study. Our optimism extends beyond the current findings, as a potential additional of 1.265 million ounces are expected to be converted to reserves following the completion of a 5.3 km road relocation besides new resources that should be added in the future once ore body remains opened along strike and down dip. Furthermore, Borborema is poised to set new benchmarks with its important contributions to ESG standards by using treated greywater from the local community, utilizing renewable energy sources, and relying on a robust local labor force."

Mr. Barbosa continues, “We are grateful for Dundee’s technical insights in getting us to this stage. Both of our teams worked hard together and both companies will benefit as we advance this project to construction and production by early 2025.”

Borborema Project Overview

The Borborema Project, located in the southern portion of the state of Rio Grande do Norte in north‐eastern Brazil, is situated 26 km east of the well‐established town of Currais Novos and 35 km west of the town of Santa Cruz. The town of Currais Novos has good infrastructure and a population of approximately 45,000 people. The Project site is strategically located to benefit from direct access to the BR‐226 federal highway linking it to the state capital Natal which lies 172 km east and has a population of approximately 880,000 inhabitants.

Borborema location map, Rio Grande do Norte, Brazil

https://www.globenewswire.com/NewsRoom/AttachmentNg/1fdcd07a-5eb1-4725-a3a0-7b789204497e

The project area was owned variously by several companies, including Xapetuba which recovered approximately 3,000 kilograms of gold using Brazil's second heap leach processing operation. Aura acquired the project in September 2022.

Open-pit stripping is expected to begin in Q2 2024, and construction expected to be concluded by Q1 2025, with first gold pour targeted for Q2 2025 and commercial production for Q3 2025.

Summary of Key Results for the Borborema Feasibility Study

| BORBOREMA GOLD PROJECT1 | Years 1-3 | Life of Mine (11.3 years) |

| Average Plant Feed Grade (g Au/t) | 1.54 | 1.12 |

| Weighted Average Annual Gold Production (koz) | 83 | 65 |

| Average Recovery (%) | 92.1 | 92.1 |

| Total Payable Gold (koz) | 248 | 748 |

| Average Cash Costs (US$/oz) | 862 | 924 |

| Average AISC2 (US$/oz) | 875 | 949 |

| Strip Ratio3 (waste:ore) | 3.61 | 3.77 |

Notes:

- All values except feed grade and strip ratio are rounded.

- Considering Royalties

- Excludes 7.2 Mt of pre-production mining.

Financial Key Performance Indicators (“KPIs”) expected for the Project

Main assumptions:

- Gold price: US$ 1,712/oz (Weighted average – 11.3 years)

- Exchange average rate (BRL / USD): R$5.08:US$1.00

- Discount rate: 5%

| Gold prices (US$/oz) | ||||

| Unleveraged | 1,500 | 1,712 | 1,900 | |

| After-tax NPV | US$ million | 85 | 182 | 262 |

| After-tax simple payback (after Start-Up) | years | 4.6 | 3.2 | 2.9 |

| After-tax IRR | % p.a. | 13.7% | 21.9% | 27.5% |

Results above are shown assuming that the project is financed with 100% equity, in compliance with NI 43-101. However, the Company has established a target to leverage the Project, aiming for at least 50% debt / total Capex.

Sensitivity analyses were conducted in order to simulate project financial performance according to different scenarios of gold price, as well as capital structure with debt on total capital. The table below indicates expected results considering an upfront debt of US$ 100 million to partially fund the construction capex.

| Gold prices (US$/oz) | ||||

| Leveraged | 1,500 | 1,712 | 1,900 | |

| After-tax simple payback (after Start-Up) | years | 2.9 | 2.3 | 2.2 |

| After-tax IRR | % p.a. | 22.3% | 40.8% | 51.9% |

Geology, Mineralization and Drilling

The deposit at the Borborema Project is considered to be a classic mesothermal/orogenic gold deposit type in a sheared and deformed Archaean to Proterozoic greenstone belt sequence comprised of metamorphosed volcanic‐sedimentary rocks units intruded by slightly younger post‐tectonic igneous bodies.

The Borborema deposit is hosted within a sequence of banded arkosic metapelitic schists, subjected to upper‐amphibolite facies regional metamorphism.

The mineralization types are strongly controlled by regional structure with secondary structures providing the preferred host for gold mineralization. In addition to the main mineralized zone, several thinner sub-parallel zones with gold mineralization are identified. Two distinct gold mineralization types are identified in drill cores: 1) disseminated free gold, and 2) gold in association with sulphide mineralization represented by pyrrhotite, chalcopyrite, pyrite, sphalerite, and galena. Additionally, the sulphide mineralization was observed in the outer contact between chert boudins and schist along with or associated with schist foliation.

The main Borborema ore body has overall dimensions of approximately 600 meters in the down-dip direction, 3,500 meters along the strike, and averages of 50 meters in thickness in the central and 30 meters in thickness in the southern and northern portions. The Borborema deposit is located within a NE-SW trending shear zone and displays a penetrative NNE‐trending fabric, dipping southeast at around 40 degrees. The ore body is open down dip beyond current Inferred Mineral Resources.

The Borborema deposit has been drilled out at nominal drill spacing of approximately 50m x 50m. A total of 303 diamond drill holes and 921 reverse circulation (“RC”) holes totaling 109,090m were drilled between 1979 and 2022. The property drilling database contains 74,038 sample intervals within the drilling database used in support of mineral resources.

Historical drilling at Borborema has been completed in various campaigns since 1979 by several companies including Itaperiba, Xapetuba, JICA, Santa Elina, and Caraíba. Crusader began drilling at the Project in August 2010 and drilled consistently until the end of 2012. Big River drilled 13 holes to extend known mineralization at depth and increase inferred mineral resources. Aura Minerals has not conducted any drilling on the Borborema property.

Data Verification

SRK Consulting (U.S.), Inc. (“SRK”) performed data verification and validation procedures on the drilling database prior to modeling and estimation. SRK reviewed the geological, drilling, and Au analytical data which was used to support Mineral Resources. Additionally, QP of Resources conducted a site visit to the Project reviewing pit geology, drill core, sample storage and security, as well conducting interviews with site personnel. It is the QP’s opinion that the raw drilling data used for estimating Mineral Resources have been adequately reviewed and any identified potential risks are accounted for in resource classified, in-line with CIM guidelines.

Mineral Resource and Mineral Reserve Estimates

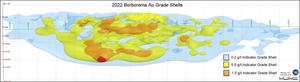

The updated resource block model gold grade was modelled by SRK using Ordinary Kriging (OK) methodology constrained within nested grade shells at 0.2 g/t, 0.5 g/t, and 1.0 g/t indicatory grade shells.

SRK used a nested, soft-boundary grade shell technique with shells at 0.2, 0.5, and 1.0 g/t Au to limit the influence of variable Au grades in the broader mineralized volume which displays general lower grade attributes. Raw drilling data was composted to 2 m lengths with upper capping applied at 20 g/t Au. Kriging neighborhoods and variography were determined for each nested grade shell. The Feasibility Study block model showed acceptable validation against composited and raw data with acceptable smoothing and is considered suitable for use in reporting of Mineral Resources.

Longitudinal View of Au Grade Shells, Viewing West (Source: SRK)

https://www.globenewswire.com/NewsRoom/AttachmentNg/2ca4c653-3470-4103-b520-aadfc844dd53

SRK utilized an oxidation boundary surface constructed in 2012 by Crusader (Cascar) to discriminate oxide from sulfide mineralization as the logging data was considered too variable and of lower confidence to construct this surface. The oxidation model is utilized to code bulk density as well.

Mineral Resources are classified in accordance with NI 43-101 and CIM definitions into Indicated and Inferred categories based on identified uncertainly and risks.

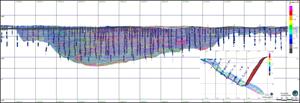

In order to establish reasonable prospects for eventual economic extraction (RPEEE) as per NI 43-101 definitions of Mineral Resources, SRK applied an economic cut-off grade (CoG) to blocks constrained within an economic pit shell on the Borborema property. This shell utilizes a 1.0 revenue factor, 37-degree slope on the west and 60-degree slope on the east, 2 million tonnes per annum (Mtpa) mining rate, and 5% discount rate. A long section of the resource pit shell is shown in figure below.

Long Section, Looking West of the Economic Pit Shell. Inset Image Shows Cross Section, Looking North (Source; SRK)

https://www.globenewswire.com/NewsRoom/AttachmentNg/54010e34-4377-4b7e-915e-1c1c59acce2b

The Feasibility Study includes Mineral Resource and Reserve estimates for the Borborema deposit under CIM guidelines. Only Indicated Mineral Resources was considered for purpose of the Feasibility Study. A summary of the Borborema Mineral Resources estimates which are used in the Feasibility Study and expected to be included in the Feasibility Study are shown in table below.

Borborema Mineral Resource Estimate* as of January 31, 2023

| CLASS | Au Cut off Grade | OXIDATION |

MASS (Mt) |

AVERAGE GRADE (Au g/t) |

TOTAL METAL (Au koz) |

| INDICATED |

0.33 g/t |

OXIDE | 2.4 | 0.79 | 62 |

| SULFIDE | 61.3 | 1.02 | 2,015 | ||

| TOTAL | 63.7 | 1.01 | 2,077 | ||

| INFERRED |

0.33 g/t |

OXIDE | 0.1 | 0.83 | 3 |

| SULFIDE | 10.8 | 1.13 | 390 | ||

| TOTAL | 10.9 | 1.13 | 393 |

* Notes:

- Mineral Resources are reported inclusive of Mineral Reserves. Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability.

- Mineral Resources have been categorized classified as Indicated or Inferred subject to the opinion of a Qualified Person based on the quality of informing data for the estimate, consistency of geological/grade distribution, data quality, and have been validated using visual and statistical analyses.

- Tonnage and contained metal have been rounded to reflect the accuracy of the estimate, and numbers may not be added due to rounding.

- 100% metal recovery assumption is applied for the Mineral Resources statement.

- The economic CoG for Mineral Resources is based on the long-term outlook sale price of US$1,800/troy ounce of gold, 5% mine dilution, 92.1% recovery, average mining costs of US$2.00/t, processing costs of US$14.82/t, G&A of US$1.38, and sustaining capital costs of US$0.62/t.

- An overall 61° (east side) and 37° (west side) pit slope angle, 0% mining dilution, and 100% mining recovery.

- Mineral Resources were reported above the economic 0.33 g/t Au CoG and are constrained by an optimized pit shell.

- The Qualified Person for Mineral Resources is Erik Ronald, P. Geo. (PGO #3050), Principal Consultant with SRK Consulting (U.S.), Inc. based in Denver, USA.

Mineral Reserves amenable to open pit mining methods were estimated through an open pit optimization exercise using the Indicated Mineral Resources in the block model provided by SRK. Mineral Reserves were reported within detailed engineered pit designs and life-of-mine (LOM) plans based on this pit shell. A high voltage transmission line (HVTL) constraints the pit to the north and a highway paved road (BR-226) constraints the pit to the south.

A summary of the Borborema Mineral Reserves estimates which is expected to be included in the Feasibility Study are shown in table below.

Borborema Mineral Reserves Estimates* (P&P) as of July 31, 2023*

| BORBOREMA PROJECT PROVEN AND PROBABLE (P&P) MINERAL RESERVES | |||

|

Reserves Classification |

Tonnage (kt) | Au (g/t) | Au (koz) |

| Proven | - | - | - |

| Probable | 22,455 | 1.12 | 812 |

| Proven + Probable | 22,455 | 1.12 | 812 |

Notes:

- CIM (2014) definitions were followed for Mineral Reserves.

- Mineral Reserves have an effective date of July 31, 2023. The Qualified Person for the estimate is Bruno Yoshida Tomaselli, B.Sc., FAusIMM, an employee of Deswik Brazil.

- Mineral Reserves are confined within an optimized pit shell that uses the following parameters: gold price including refining costs: US$ 1,472/oz; mining costs: US$ 2.40/t weathered material, US$ 2.80/t waste fresh rock, US$ 3.20/t ore fresh rock; processing costs: US$ 14.82/t processed; general and administrative costs: US$ 2.6 M/a; sustaining costs: US$ 0.62/t processed; process recovery of 92.1% (On the assumption basis of 90% sulfide and 10% oxide materials); mining dilution of 5%; ore recovery of 95%; pit inter-ramp angles that range from 35 – 64°.

- Tonnages and grades have been rounded in accordance with reporting guidelines. Totals may not sum due to rounding.

Mine Plan

At Borborema, the ore is near surface and continues at depth. The initial 11 years and 4 months are planned for open pit mining, with operations based on the use of hydraulic excavators and a haul truck fleet engaged in conventional open pit mining techniques. The open pit mining activities were assumed to be primarily undertaken by a contractor-operated fleet.

The stripping ratio is 3.8:1 waste to ore, and 7.2 Mt of pre-stripping is proposed. The mine production schedule delivers 22.5 Mt of ore grading 1.12 g/t gold to the mill over the LOM. Waste tonnage totaling 84.5 Mt will be placed in the waste rock dumps.

Mining costs, including the mining contractor charges, stockpile re-handling and grade control, are estimated to average US$2.78/t mined over the LOM.

Production Schedule

Two low-grade stockpiles are envisaged for the Project to improve grades for the initial years and control the rate of oxide ore on the plant feed. Low grade ore will be stockpiled during the operation and reclaimed at the end of the LOM or when required. The oxide stockpile is also planned to control the maximum rate of oxide material that can be fed to the plant.

The LOM plan shows recoveries of 92.1% with a weighted average production of 83 koz of gold per year for the first three years (2025-2027) with a weighted average AISC of US$875/oz. LOM weighted average production of 65 koz of gold per year with LOM weighted average AISC of US$949/oz.

Processing

The Project includes a process plant capable of treating 2 Mtpa of ore through single-stage primary crushing, grinding semi-autogenous grinding mill in a closed circuit with hydrocyclones, gravimetry and intensive leaching, carbon-in-leach tanks, elution, thickening unit, detox and final thickening unit for tailings filtering.

Processing costs are estimated to average US$12.31/t of ore processed over the LOM. The three largest cost components are power, grinding media, and cyanide. Other significant costs are workforce, carbon, and maintenance materials.

Labor

The process considers the average G&A costs of US$5.01/t over the LOM. This workforce mainly includes management, health, safety and environmental, administration, human resources, IT, law enforcement, procurement, royalties, insurance, etc.

Taxes and Royalties

The financial model incorporates assumptions about the income tax reduction benefit made available under a government regulation. The income tax rate is calculated at 17.58%. The Project will pay royalties of 1.5% of gross revenue to the Federal, State and Local Governments (CFEM).

The Project will also pay royalties equivalent to 1.50% on the sale of any product containing economically recoverable minerals obtained from ore mined and removed from the mine to Dundee Resources Limited. The 1.50% net smelter return applies to the first 1,500,000 ounces of gold sold, then is reduced to 1.00% on the next 500,000 ounces of gold. Once the production threshold of 2,000,000 ounces of gold from the Borborema gold project has been reached, the Royalty will terminate in accordance with its terms.

Engineering, Procurement and Construction Management

Basic engineering and detailed engineering for earthmoving are completed, and engineering design for the mine is completed. Plant detailed engineering is set to begin. Aura commenced early works construction for Borborema in Q2 2023 and vegetation suppression 48% complete, plant site is almost cleared and leveled, and the longest lead-time equipment (mill) has been ordered. Of the US$188 million construction budget, US$1.1 million has been spent as of Q2 2023 and US$11.4 million is planned for the second half of 2023.

Feasibility Study Preparation

Aura retained Promon Engenharia Ltda. (“Promon”), SRK Consulting (U.S.), Inc. Denver, USA. (“SRK”), and MCB Serviços e Mineração Ltda. (“Deswik Brazil") to jointly prepare with the Aura Technical Services group a Feasibility Study on the Borborema Project. The Technical Report provides the open-pit Feasibility Study. The Feasibility Study also provides an update on the ownership status of the project, Mineral Resources (reported inclusive of Mineral Reserves), Mineral Reserves and project economics.

The Qualified Persons (“QPs”) are Homero Delboni Jr., Ph.D., MAusIMM – CP Metallurgy, (Independent Consultant), Erik Ronald, P.Geo., Principal Consultant with SRK (U.S,), Inc. (“SRK”), Farshid Ghazanfari, P.Geo., Geology and Mineral Resources Director for Aura Minerals Inc, and Bruno Yoshida Tomaselli, FAusIMM, Consulting Manager with Deswik Brazil. The Mineral Resources were prepared by Erik Ronald. The Mineral Reserves, mine plan and mining sections of the study were prepared by or under the supervision of Bruno Yoshida Tomaselli. The metallurgical testwork, process design and process plant information were prepared by or under the supervision of Homero Delboni, Jr. The study is being summarized into a technical report that will be filed within 45 days on SEDAR at www.sedar.com, in accordance with National Instrument 43-101.

Qualified Persons

The technical content of this press release has been reviewed and approved by the QPs who were involved with preparation of the Borborema study: Homero Delboni Jr., Erik Ronald, Farshid Ghazanfari and Bruno Yoshida Tomaselli.

The QPs are not aware of any known political, legal, environmental or other risks that could materially affect the project development.

Quality Assurance and Quality Control

Analytical work was carried out by two Certified Brazilian laboratories were contracted by Crusader for sample analyses: Bureau Veritas Laboratory (BV) and ALS Laboratory. In addition, check sampling was undertaken at Acme Analytical Laboratories Ltd (Acme) in Santiago, Chile and by Bureau Veritas’ Ultratrace Laboratory in Perth, Western Australia. Big River used SGS GEOSOL Laboratórios Ltda (Rodovia MG010, Km 24,5, bairro Angicos, CEP: 33206-240. Vespasiano/MG.) for 2021-2022 drilling campaign.

Crusader QA/QC program comprised submitting sample blanks, standard reference samples, sample duplicates, and inter‐laboratory check samples. The rate of sample submissions for blanks and reference materials was 1 in 20 samples, duplicates 1 in 25 samples (only for RC holes) and interlaboratory check assays 1 in 10 samples.

The Big River QA/QC program included submittal of both blind and non-blind control samples into the sample stream being analyzed by the SGS laboratory. Big River maintained Internal quality control by inserting minimum of one blank sample in each batch and mainly after each mineralized zone, two standards (one high grade and one low grade in each analytical batch of 40 samples (5%) and a minimum of two core duplicates in each analytical batch of 40 samples (5%); (Duplicate samples analysis were requested to the lab after received the original results – average of 5 samples per hole).

The control sample assay results of the internal QA/QC program were monitored, including the CRMs, Blanks, and coarse duplicates. Additionally, systematic checks of the digital database were conducted against the original signed Certificates of Analysis from the laboratory.

Mr. Ghazanfari has reviewed the sampling and QA/QC procedures and results thereof as verification of the sampling data disclosed above and approved the information contained in this news release.

About Aura 360° Mining

Aura is focused on mining in complete terms – thinking holistically about how its business impacts and benefits every one of our stakeholders: our company, our shareholders, our employees, and the countries and communities we serve. We call this 360° Mining.

Aura is a mid-tier gold and copper production company focused on operating and developing gold and base metal projects in the Americas. The Company has 4 operating mines including the Aranzazu copper-gold-silver mine in Mexico, the EPP and Almas gold mines in Brazil, and the San Andres gold mine in Honduras. The Company’s development projects include Borborema and Matupá both in Brazil. Aura has unmatched exploration potential owning over 650,000 hectares of mineral rights and is currently advancing multiple near-mine and regional targets along with the Serra da Estrela copper project in the prolific Carajás region of Brazil.

For further information, please visit Aura’s website at www.auraminerals.com.

Caution Regarding Mineral Resource and Mineral Reserve Estimates

The figures for mineral resources and reserves contained herein are estimates only and no assurance can be given that the anticipated tonnages and grades will be achieved, that the indicated level of recovery will be realized or that the mineral resources and reserves could be mined or processed profitably. Actual reserves, if any, may not conform to geological, metallurgical or other expectations, and the volume and grade of ore recovered may be below the estimated levels. There are numerous uncertainties inherent in estimating mineral resources and reserves, including many factors beyond the Company’s control. Such estimation is a subjective process, and the accuracy of any reserve or resource estimate is a function of the quantity and quality of available data and of the assumptions made and judgments used in engineering and geological interpretation. Short-term operating factors relating to the mineral resources and reserves, such as the need for orderly development of the ore bodies or the processing of new or different ore grades, may cause the mining operation to be unprofitable in any particular accounting period. In addition, there can be no assurance that metal recoveries in small scale laboratory tests will be duplicated in larger scale tests under on-site conditions or during production. Lower market prices, increased production costs, the presence of deleterious elements, reduced recovery rates and other factors may result in revision of its resource and reserve estimates from time to time or may render the Company’s resources and reserves uneconomic to exploit. Resource and reserve data is not indicative of future results of operations. If the Company’s actual mineral resources and reserves are less than current estimates or if the Company fails to develop its resource base through the realization of identified mineralized potential, its results of operations or financial condition may be materially and adversely affected.

All forward-looking statements herein are qualified by this cautionary statement. Accordingly, readers should not place undue reliance on forward-looking statements. The Company undertakes no obligation to update publicly or otherwise revise any forward-looking statements whether as a result of new information or future events or otherwise, except as may be required by law. If the Company does update one or more forward-looking statements, no inference should be drawn that it will make additional updates with respect to those or other forward-looking statements.

Forward-Looking Information

This press release contains “forward-looking information” and “forward-looking statements”, as defined in applicable securities laws (collectively, “forward-looking statements”) which include, without limitation, mineral resources and mineral reserve estimates and the economic analysis resulting from the Feasibility Study (including NPV, IRR and payback periods); expected production from, and the further potential of the Company’s properties; the ability of the Company to achieve its longer-term outlook; the amount of future production over any period and LOM, capital expenditure, AISC and mine production costs, the Company’s target leverage ratio for the Project; and the completion of the conversion of Dundee’s equity interest in the Project into a net smelter returns royalty.

Known and unknown risks, uncertainties and other factors, many of which are beyond the Company’s ability to predict or control, could cause actual results to differ materially from those contained in the forward-looking statements if such risks, uncertainties or factors materialize. The Company has made numerous assumptions with respect to forward-looking information contain herein, including among other things, assumptions from the Feasibility Study, which may include assumptions on gold prices and exchange rates, which could also cause actual results to differ materially from those contained in the forward-looking statements if such assumptions prove wrong. Specific reference is made to the Company’s most recent AIF on file with certain Canadian provincial securities regulatory authorities and the Technical Reports for a discussion of some of the risk factors underlying forward-looking statements, which include, without limitation the ability of the Company to achieve its longer-term outlook and the anticipated timing and results thereof, the ability to lower costs and increase production, the ability of the Company to successfully achieve business objectives, copper and gold or certain other commodity price volatility, changes in debt and equity markets, the uncertainties involved in interpreting geological data, increases in costs, environmental compliance and changes in environmental legislation and regulation, interest rate and exchange rate fluctuations, general economic conditions and other risks involved in the mineral exploration and development industry. Readers are cautioned that the foregoing list of factors is not exhaustive of the factors that may affect the forward-looking statements.

Rodrigo Barbosa President & CEO 305-239-9332

![]()

Borborema location map, Rio Grande do Norte, Brazil

Borborema location map, Rio Grande do Norte, Brazil

Longitudinal View of Au Grade Shells, Viewing West (Source: SRK)

Longitudinal View of Au Grade Shells, Viewing West (Source: SRK)

Long Section, Looking West of the Economic Pit Shell. Inset Image Shows Cross Section, Looking North (Source; SRK)

Long Section, Looking West of the Economic Pit Shell. Inset Image Shows Cross Section, Looking North (Source; SRK)

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.