Fentura Financial, Inc. Announces First Quarter 2021 Earnings

Dollars in thousands except per share amounts. Certain items in the prior period financial statements have been reclassified to conform with the March 31, 2021 presentation.

FENTON, Mich., May 03, 2021 (GLOBE NEWSWIRE) -- Fentura Financial, Inc. (OTCQX: FETM) announces quarterly results of net income of $4,656 for the three month period ended March 31, 2021.

Ronald Justice, President and CEO, stated "I am pleased with Fentura’s strong operating results for the first quarter of 2021. Continued outstanding residential mortgage loan activity, new business loans and core funding levels contributed to solid earnings and strong core balance sheet growth. Asset quality metrics remain strong and COVID-19 related payment deferrals significantly declined as borrowers resumed regular payments. While we continue to navigate the challenges presented by the COVID-19 pandemic, our team remains committed to our mission and we are well positioned and optimistic about our future."

Following is a discussion of the Corporation's financial performance as of, and for the three month period ended March 31, 2021. At the end of this document is a list of abbreviations and acronyms.

Results of Operations

The following table outlines the Corporation's QTD results of operations and provides certain performance measures as of, and for the three month periods ended:

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| INCOME STATEMENT DATA | ||||||||||||||||||||

| Interest income | $ | 11,919 | $ | 11,624 | $ | 12,070 | $ | 11,215 | $ | 11,070 | ||||||||||

| Interest expense | 676 | 972 | 1,189 | 1,618 | 2,145 | |||||||||||||||

| Net interest income | 11,243 | 10,652 | 10,881 | 9,597 | 8,925 | |||||||||||||||

| Provision for loan losses | 212 | 982 | 1,109 | 2,001 | 1,542 | |||||||||||||||

| Noninterest income | 3,854 | 4,676 | 5,159 | 5,292 | 4,513 | |||||||||||||||

| Noninterest expenses | 9,031 | 10,971 | 8,218 | 7,809 | 7,686 | |||||||||||||||

| Federal income tax expense | 1,198 | 642 | 1,377 | 1,036 | 858 | |||||||||||||||

| Net income | $ | 4,656 | $ | 2,733 | $ | 5,336 | $ | 4,043 | $ | 3,352 | ||||||||||

| PER SHARE | ||||||||||||||||||||

| Earnings | $ | 1.00 | $ | 0.58 | $ | 1.14 | $ | 0.87 | $ | 0.72 | ||||||||||

| Dividends | $ | 0.080 | $ | 0.075 | $ | 0.075 | $ | 0.075 | $ | 0.075 | ||||||||||

| Tangible book value(1) | $ | 24.68 | $ | 23.88 | $ | 23.50 | $ | 22.44 | $ | 21.56 | ||||||||||

| Quoted market value | ||||||||||||||||||||

| High | $ | 24.75 | $ | 22.25 | $ | 17.99 | $ | 18.95 | $ | 26.00 | ||||||||||

| Low | $ | 21.90 | $ | 16.93 | $ | 16.80 | $ | 14.90 | $ | 12.55 | ||||||||||

| Close(1) | $ | 23.30 | $ | 22.00 | $ | 16.93 | $ | 17.35 | $ | 15.50 | ||||||||||

| PERFORMANCE RATIOS | ||||||||||||||||||||

| Return on average assets | 1.50 | % | 0.84 | % | 1.68 | % | 1.35 | % | 1.28 | % | ||||||||||

| Return on average shareholders' equity | 15.86 | % | 9.27 | % | 18.86 | % | 15.20 | % | 13.01 | % | ||||||||||

| Return on average tangible shareholders' equity | 16.38 | % | 9.58 | % | 19.54 | % | 15.79 | % | 13.54 | % | ||||||||||

| Efficiency ratio | 59.82 | % | 71.57 | % | 51.23 | % | 52.45 | % | 57.20 | % | ||||||||||

| Yield on earning assets (FTE) | 4.01 | % | 3.75 | % | 3.97 | % | 3.94 | % | 4.47 | % | ||||||||||

| Rate on interest bearing liabilities | 0.37 | % | 0.50 | % | 0.63 | % | 0.91 | % | 1.28 | % | ||||||||||

| Net interest margin to earning assets (FTE) | 3.79 | % | 3.44 | % | 3.58 | % | 3.37 | % | 3.61 | % | ||||||||||

| BALANCE SHEET DATA(1) | ||||||||||||||||||||

| Total investment securities | $ | 89,772 | $ | 76,111 | $ | 78,179 | $ | 75,526 | $ | 76,312 | ||||||||||

| Gross loans | $ | 1,028,117 | $ | 1,066,562 | $ | 1,060,885 | $ | 1,044,564 | $ | 865,577 | ||||||||||

| Total assets | $ | 1,302,794 | $ | 1,251,446 | $ | 1,284,845 | $ | 1,237,694 | $ | 1,071,180 | ||||||||||

| Total deposits | $ | 1,122,508 | $ | 1,071,976 | $ | 1,061,470 | $ | 1,018,287 | $ | 883,837 | ||||||||||

| Borrowed funds | $ | 49,000 | $ | 49,000 | $ | 96,217 | $ | 96,217 | $ | 71,500 | ||||||||||

| Total shareholders' equity | $ | 119,059 | $ | 115,868 | $ | 114,081 | $ | 108,969 | $ | 104,828 | ||||||||||

| Net loans to total deposits | 90.60 | % | 98.48 | % | 98.99 | % | 101.70 | % | 97.11 | % | ||||||||||

| Common shares outstanding | 4,673,932 | 4,694,275 | 4,691,142 | 4,680,920 | 4,675,499 | |||||||||||||||

| QTD BALANCE SHEET AVERAGES | ||||||||||||||||||||

| Total assets | $ | 1,259,119 | $ | 1,288,199 | $ | 1,264,105 | $ | 1,200,966 | $ | 1,049,245 | ||||||||||

| Earning assets | $ | 1,206,411 | $ | 1,235,895 | $ | 1,210,274 | $ | 1,146,941 | $ | 997,089 | ||||||||||

| Interest bearing liabilities | $ | 735,159 | $ | 773,132 | $ | 750,281 | $ | 711,500 | $ | 672,564 | ||||||||||

| Total shareholders' equity | $ | 119,034 | $ | 117,263 | $ | 112,565 | $ | 106,998 | $ | 103,646 | ||||||||||

| Total tangible shareholders' equity | $ | 115,298 | $ | 113,444 | $ | 108,655 | $ | 102,999 | $ | 99,558 | ||||||||||

| Earned common shares outstanding | 4,664,893 | 4,682,063 | 4,673,629 | 4,664,946 | 4,659,279 | |||||||||||||||

| Unvested stock grants | 21,922 | 14,208 | 14,208 | 14,208 | 13,481 | |||||||||||||||

| Total common shares outstanding | 4,686,815 | 4,696,271 | 4,687,837 | 4,679,154 | 4,672,760 | |||||||||||||||

| ASSET QUALITY(1) | ||||||||||||||||||||

| Nonperforming loans to gross loans | 0.79 | % | 0.75 | % | 0.07 | % | 0.10 | % | 0.10 | % | ||||||||||

| Nonperforming assets to total assets | 0.62 | % | 0.64 | % | 0.06 | % | 0.08 | % | 0.12 | % | ||||||||||

| Allowance for loan losses to gross loans | 1.08 | % | 1.02 | % | 0.95 | % | 0.86 | % | 0.84 | % | ||||||||||

| Allowance for loan losses to gross loans, net of PPP loans | 1.23 | % | 1.23 | % | 1.19 | % | 1.07 | % | 0.84 | % | ||||||||||

| CAPITAL RATIOS(1) | ||||||||||||||||||||

| Total capital to risk weighted assets | 15.02 | % | 15.14 | % | 15.57 | % | 15.06 | % | 14.44 | % | ||||||||||

| Tier 1 capital to risk weighted assets | 13.84 | % | 13.93 | % | 14.40 | % | 14.00 | % | 13.58 | % | ||||||||||

| CET1 capital to risk weighted assets | 12.34 | % | 12.38 | % | 12.77 | % | 12.34 | % | 11.92 | % | ||||||||||

| Tier 1 leverage ratio | 10.31 | % | 9.80 | % | 9.86 | % | 9.91 | % | 10.97 | % | ||||||||||

| (1)At end of period | ||||||||||||||||||||

The following table outlines the Corporation's YTD results of operations and provides certain performance measures as of, and for the three month periods ended:

| 3/31/2021 | 3/31/2020 | 3/31/2019 | 3/31/2018 | 3/31/2017 | ||||||||||||||||

| INCOME STATEMENT DATA | ||||||||||||||||||||

| Interest income | $ | 11,919 | $ | 11,070 | $ | 10,437 | $ | 8,379 | $ | 6,427 | ||||||||||

| Interest expense | 676 | 2,145 | 2,090 | 1,031 | 687 | |||||||||||||||

| Net interest income | 11,243 | 8,925 | 8,347 | 7,348 | 5,740 | |||||||||||||||

| Provision for loan losses | 212 | 1,542 | 213 | 275 | — | |||||||||||||||

| Noninterest income | 3,854 | 4,513 | 1,522 | 1,801 | 1,234 | |||||||||||||||

| Noninterest expenses | 9,031 | 7,686 | 6,509 | 6,279 | 5,095 | |||||||||||||||

| Federal income tax expense | 1,198 | 858 | 633 | 521 | 592 | |||||||||||||||

| Net income | $ | 4,656 | $ | 3,352 | $ | 2,514 | $ | 2,074 | $ | 1,287 | ||||||||||

| PER SHARE | ||||||||||||||||||||

| Earnings | $ | 1.00 | $ | 0.72 | $ | 0.54 | $ | 0.57 | $ | 0.35 | ||||||||||

| Dividends | $ | 0.080 | $ | 0.075 | $ | 0.070 | $ | 0.060 | $ | 0.050 | ||||||||||

| Tangible book value(1) | $ | 24.68 | $ | 21.56 | $ | 18.88 | $ | 15.27 | $ | 12.86 | ||||||||||

| Quoted market value | ||||||||||||||||||||

| High | $ | 24.75 | $ | 26.00 | $ | 21.00 | $ | 20.19 | $ | 18.25 | ||||||||||

| Low | $ | 21.90 | $ | 12.55 | $ | 20.05 | $ | 18.88 | $ | 15.10 | ||||||||||

| Close(1) | $ | 23.30 | $ | 15.50 | $ | 20.89 | $ | 19.75 | $ | 18.00 | ||||||||||

| PERFORMANCE RATIOS | ||||||||||||||||||||

| Return on average assets | 1.50 | % | 1.28 | % | 1.09 | % | 1.07 | % | 0.73 | % | ||||||||||

| Return on average shareholders' equity | 15.86 | % | 13.01 | % | 11.09 | % | 13.99 | % | 10.19 | % | ||||||||||

| Return on average tangible shareholders' equity | 16.38 | % | 13.54 | % | 11.66 | % | 15.28 | % | 10.63 | % | ||||||||||

| Efficiency ratio | 59.82 | % | 57.20 | % | 65.95 | % | 68.63 | % | 73.06 | % | ||||||||||

| Yield on earning assets (FTE) | 4.01 | % | 4.47 | % | 4.77 | % | 4.51 | % | 4.19 | % | ||||||||||

| Rate on interest bearing liabilities | 0.37 | % | 1.28 | % | 1.40 | % | 0.83 | % | 0.55 | % | ||||||||||

| Net interest margin to earning assets (FTE) | 3.79 | % | 3.61 | % | 3.81 | % | 3.90 | % | 3.74 | % | ||||||||||

| BALANCE SHEET DATA(1) | ||||||||||||||||||||

| Total investment securities | $ | 89,772 | $ | 76,312 | $ | 82,222 | $ | 49,608 | $ | 72,472 | ||||||||||

| Gross loans | $ | 1,028,117 | $ | 865,577 | $ | 809,863 | $ | 686,140 | $ | 554,415 | ||||||||||

| Total assets | $ | 1,302,794 | $ | 1,071,180 | $ | 946,172 | $ | 789,943 | $ | 730,636 | ||||||||||

| Total deposits | $ | 1,122,508 | $ | 883,837 | $ | 789,533 | $ | 683,775 | $ | 630,055 | ||||||||||

| Borrowed funds | $ | 49,000 | $ | 71,500 | $ | 59,000 | $ | 44,600 | $ | 45,000 | ||||||||||

| Total shareholders' equity | $ | 119,059 | $ | 104,828 | $ | 92,236 | $ | 60,621 | $ | 51,816 | ||||||||||

| Net loans to total deposits | 90.60 | % | 97.11 | % | 101.97 | % | 99.80 | % | 87.54 | % | ||||||||||

| Common shares outstanding | 4,673,932 | 4,675,499 | 4,647,978 | 3,635,098 | 3,620,964 | |||||||||||||||

| YTD BALANCE SHEET AVERAGES | ||||||||||||||||||||

| Total assets | $ | 1,259,119 | $ | 1,049,245 | $ | 934,078 | $ | 789,391 | $ | 716,998 | ||||||||||

| Earning assets | $ | 1,206,411 | $ | 997,089 | $ | 887,974 | $ | 755,281 | $ | 613,904 | ||||||||||

| Interest bearing liabilities | $ | 735,159 | $ | 672,564 | $ | 604,973 | $ | 505,174 | $ | 499,636 | ||||||||||

| Total shareholders' equity | $ | 119,034 | $ | 103,646 | $ | 91,964 | $ | 60,107 | $ | 51,241 | ||||||||||

| Total tangible shareholders' equity | $ | 115,298 | $ | 99,558 | $ | 87,430 | $ | 55,041 | $ | 49,104 | ||||||||||

| Earned common shares outstanding | 4,664,893 | 4,659,279 | 4,635,255 | 3,633,093 | 3,677,143 | |||||||||||||||

| Unvested stock grants | 21,922 | 13,481 | 9,788 | — | — | |||||||||||||||

| Total common shares outstanding | 4,686,815 | 4,672,760 | 4,645,043 | 3,633,093 | 3,677,143 | |||||||||||||||

| ASSET QUALITY(1) | ||||||||||||||||||||

| Nonperforming loans to gross loans | 0.79 | % | 0.10 | % | 0.11 | % | 0.10 | % | 0.33 | % | ||||||||||

| Nonperforming assets to total assets | 0.62 | % | 0.12 | % | 0.09 | % | 0.10 | % | 0.28 | % | ||||||||||

| Allowance for loan losses to gross loans | 1.08 | % | 0.84 | % | 0.59 | % | 0.54 | % | 0.52 | % | ||||||||||

| Allowance for loan losses to gross loans, net of PPP loans | 1.23 | % | 0.84 | % | 0.59 | % | 0.54 | % | 0.52 | % | ||||||||||

| CAPITAL RATIOS(1) | ||||||||||||||||||||

| Total capital to risk weighted assets | 15.02 | % | 14.44 | % | 14.01 | % | 11.03 | % | 11.72 | % | ||||||||||

| Tier 1 capital to risk weighted assets | 13.84 | % | 13.58 | % | 13.38 | % | 10.48 | % | 11.20 | % | ||||||||||

| CET1 capital to risk weighted assets | 12.34 | % | 11.92 | % | 11.55 | % | 8.41 | % | 8.65 | % | ||||||||||

| Tier 1 leverage ratio | 10.31 | % | 10.97 | % | 11.00 | % | 9.01 | % | 8.60 | % | ||||||||||

| (1)At end of period | ||||||||||||||||||||

Income Statement Breakdown and Analysis

| Quarter to Date | |||||||||||||||||||||||||

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | |||||||||||||||||||||

| GAAP net income | $ | 4,656 | $ | 2,733 | $ | 5,336 | $ | 4,043 | $ | 3,352 | |||||||||||||||

| Acquisition related items (net of tax) | |||||||||||||||||||||||||

| Accretion on purchased loans | (151 | ) | (82 | ) | (144 | ) | (110 | ) | (180 | ) | |||||||||||||||

| Amortization of core deposit intangibles | 54 | 71 | 72 | 71 | 71 | ||||||||||||||||||||

| Amortization on acquired time deposits | 2 | 5 | 5 | 5 | 5 | ||||||||||||||||||||

| Total acquisition related items (net of tax) | (95 | ) | (6 | ) | (67 | ) | (34 | ) | (104 | ) | |||||||||||||||

| Other nonrecurring items (net of tax) | |||||||||||||||||||||||||

| FHLB prepayment penalties | — | 1,507 | — | — | — | ||||||||||||||||||||

| Change in fair value of equity investment due to acquisition transaction | — | — | — | — | (578 | ) | |||||||||||||||||||

| Change in fair value of mortgage banking instruments | — | — | — | — | (448 | ) | |||||||||||||||||||

| Interest writeoff from loan transferred to nonaccrual | — | 265 | — | — | — | ||||||||||||||||||||

| Net gain from COLI death benefit | — | — | — | (173 | ) | — | |||||||||||||||||||

| Prepayment penalties collected | (17 | ) | (97 | ) | (16 | ) | (12 | ) | (36 | ) | |||||||||||||||

| Mortgage servicing rights (reduction of) impairment | — | (188 | ) | (176 | ) | 191 | 173 | ||||||||||||||||||

| Total other nonrecurring items (net of tax) | (17 | ) | 1,487 | (192 | ) | 6 | (889 | ) | |||||||||||||||||

| Adjusted net income from operations | $ | 4,544 | $ | 4,214 | $ | 5,077 | $ | 4,015 | $ | 2,359 | |||||||||||||||

| GAAP net interest income | $ | 11,243 | $ | 10,652 | $ | 10,881 | $ | 9,597 | $ | 8,925 | |||||||||||||||

| Accretion on purchased loans | (191 | ) | (104 | ) | (182 | ) | (139 | ) | (228 | ) | |||||||||||||||

| Interest writeoff from loan transferred to nonaccrual | — | 335 | — | — | — | ||||||||||||||||||||

| Prepayment penalties collected | (21 | ) | (123 | ) | (20 | ) | (15 | ) | (46 | ) | |||||||||||||||

| Amortization on acquired time deposits | 3 | 6 | 6 | 6 | 6 | ||||||||||||||||||||

| Adjusted net interest income | $ | 11,034 | $ | 10,766 | $ | 10,685 | $ | 9,449 | $ | 8,657 | |||||||||||||||

| PERFORMANCE RATIOS | |||||||||||||||||||||||||

| Based on adjusted net income from operations | |||||||||||||||||||||||||

| Earnings per share | $ | 0.97 | $ | 0.90 | $ | 1.09 | $ | 0.86 | $ | 0.51 | |||||||||||||||

| Return on average assets | 1.46 | % | 1.30 | % | 1.60 | % | 1.34 | % | 0.90 | % | |||||||||||||||

| Return on average shareholders' equity | 15.48 | % | 14.30 | % | 17.94 | % | 15.09 | % | 9.15 | % | |||||||||||||||

| Return on average tangible shareholders' equity | 15.98 | % | 14.78 | % | 18.59 | % | 15.68 | % | 9.53 | % | |||||||||||||||

| Efficiency ratio | 60.20 | % | 59.02 | % | 52.03 | % | 52.12 | % | 62.83 | % | |||||||||||||||

| Based on adjusted net interest income | |||||||||||||||||||||||||

| Yield on earning assets (FTE) | 3.94 | % | 3.78 | % | 3.91 | % | 3.89 | % | 4.39 | % | |||||||||||||||

| Rate on interest bearing liabilities | 0.37 | % | 0.50 | % | 0.63 | % | 0.92 | % | 1.29 | % | |||||||||||||||

| Net interest margin to earning assets (FTE) | 3.71 | % | 3.47 | % | 3.52 | % | 3.32 | % | 3.52 | % | |||||||||||||||

To effectively compare core operating results from period to period, the impact of acquisition related items and other nonrecurring items have been isolated.

| Year to Date March 31 | Variance | ||||||||||||||||||

| 2021 | 2020 | Amount | % | ||||||||||||||||

| GAAP net income | $ | 4,656 | $ | 3,352 | $ | 1,304 | 38.90 | % | |||||||||||

| Acquisition related items (net of tax) | |||||||||||||||||||

| Accretion on purchased loans | (151 | ) | (180 | ) | 29 | (16.11 | ) | % | |||||||||||

| Amortization of core deposit intangibles | 54 | 71 | (17 | ) | (23.94 | ) | % | ||||||||||||

| Amortization on acquired time deposits | 2 | 5 | (3 | ) | (60.00 | ) | % | ||||||||||||

| Total acquisition related items (net of tax) | (95 | ) | (104 | ) | 9 | (8.65 | ) | % | |||||||||||

| Other nonrecurring items (net of tax) | |||||||||||||||||||

| FHLB prepayment penalties | — | — | — | — | % | ||||||||||||||

| Change in fair value of equity investment due to acquisition transaction | — | (578 | ) | 578 | (100.00 | ) | % | ||||||||||||

| Change in fair value of mortgage banking instruments | — | (448 | ) | 448 | (100.00 | ) | % | ||||||||||||

| Interest writeoff from loan transferred to nonaccrual | — | — | — | — | % | ||||||||||||||

| Net gain from COLI death benefit | — | — | — | — | % | ||||||||||||||

| Prepayment penalties collected | (17 | ) | (36 | ) | 19 | (52.78 | ) | % | |||||||||||

| Mortgage servicing rights (reduction of) impairment | — | 173 | (173 | ) | (100.00 | ) | % | ||||||||||||

| Total other nonrecurring items (net of tax) | (17 | ) | (889 | ) | 872 | (98.09 | ) | % | |||||||||||

| Adjusted net income from operations | $ | 4,544 | $ | 2,359 | $ | 2,185 | 92.62 | % | |||||||||||

| GAAP net interest income | $ | 11,243 | $ | 8,925 | $ | 2,318 | 25.97 | % | |||||||||||

| Accretion on purchased loans | (191 | ) | (228 | ) | 37 | (16.23 | ) | % | |||||||||||

| Interest writeoff from loan transferred to nonaccrual | — | — | — | — | % | ||||||||||||||

| Prepayment penalties collected | (21 | ) | (46 | ) | 25 | (54.35 | ) | % | |||||||||||

| Amortization on acquired time deposits | 3 | 6 | (3 | ) | (50.00 | ) | % | ||||||||||||

| Adjusted net interest income | $ | 11,034 | $ | 8,657 | $ | 2,377 | 27.46 | % | |||||||||||

| PERFORMANCE RATIOS | |||||||||||||||||||

| Based on adjusted net income from operations | |||||||||||||||||||

| Earnings per share | $ | 0.97 | $ | 0.51 | $ | 0.46 | 90.20 | % | |||||||||||

| Return on average assets | 1.46 | % | 0.90 | % | 0.56 | % | |||||||||||||

| Return on average shareholders' equity | 15.48 | % | 9.15 | % | 6.33 | % | |||||||||||||

| Return on average tangible shareholders' equity | 15.98 | % | 9.53 | % | 6.45 | % | |||||||||||||

| Efficiency ratio | 60.20 | % | 62.83 | % | (2.63 | ) | % | ||||||||||||

| Based on adjusted net interest income | |||||||||||||||||||

| Yield on earning assets (FTE) | 3.94 | % | 4.39 | % | (0.45 | ) | % | ||||||||||||

| Rate on interest bearing liabilities | 0.37 | % | 1.29 | % | (0.92 | ) | % | ||||||||||||

| Net interest margin to earning assets (FTE) | 3.71 | % | 3.52 | % | 0.19 | % | |||||||||||||

To effectively compare core operating results from period to period, the impact of acquisition related items and other nonrecurring items have been isolated.

Average Balances, Interest Rate, and Net Interest Income

The following tables present the daily average amount outstanding for each major category of interest earning assets, nonearning assets, interest bearing liabilities, and noninterest bearing liabilities. These tables also present an analysis of interest income and interest expense for the periods indicated. All interest income is reported on a FTE basis using a federal income tax rate of 21%. Loans in nonaccrual status, for the purpose of the following computations, are included in the average loan balances.

| Three Months Ended | |||||||||||||||||||||||||||||||||

| March 31, 2021 | December 31, 2020 | March 31, 2020 | |||||||||||||||||||||||||||||||

| Average Balance | Tax Equivalent Interest | Average Yield / Rate | Average Balance | Tax Equivalent Interest | Average Yield / Rate | Average Balance | Tax Equivalent Interest | Average Yield / Rate | |||||||||||||||||||||||||

| Interest earning assets | |||||||||||||||||||||||||||||||||

| Total loans | $ | 1,074,096 | $ | 11,598 | 4.38 | % | $ | 1,099,779 | $ | 11,268 | 4.08 | % | $ | 878,813 | $ | 10,481 | 4.80 | % | |||||||||||||||

| Taxable investment securities | 58,859 | 202 | 1.39 | % | 62,866 | 238 | 1.51 | % | 56,963 | 353 | 2.49 | % | |||||||||||||||||||||

| Nontaxable investment securities | 17,165 | 105 | 2.48 | % | 16,047 | 103 | 2.55 | % | 10,532 | 81 | 3.09 | % | |||||||||||||||||||||

| Federal funds sold | — | — | — | % | — | — | — | % | 33,588 | 116 | 1.39 | % | |||||||||||||||||||||

| Interest earning cash and cash equivalents | 52,803 | 11 | 0.08 | % | 53,715 | 15 | 0.11 | % | 14,043 | 26 | 0.74 | % | |||||||||||||||||||||

| Federal Home Loan Bank stock | 3,488 | 25 | 2.91 | % | 3,488 | 22 | 2.51 | % | 3,150 | 30 | 3.83 | % | |||||||||||||||||||||

| Total earning assets | 1,206,411 | 11,941 | 4.01 | % | 1,235,895 | 11,646 | 3.75 | % | 997,089 | 11,087 | 4.47 | % | |||||||||||||||||||||

| Nonearning assets | |||||||||||||||||||||||||||||||||

| Allowance for loan losses | (11,143 | ) | (10,375 | ) | (5,821 | ) | |||||||||||||||||||||||||||

| Fixed assets | 15,757 | 15,465 | 15,538 | ||||||||||||||||||||||||||||||

| Accrued income and other assets | 48,094 | 47,214 | 42,439 | ||||||||||||||||||||||||||||||

| Total assets | $ | 1,259,119 | $ | 1,288,199 | $ | 1,049,245 | |||||||||||||||||||||||||||

| Interest bearing liabilities | |||||||||||||||||||||||||||||||||

| Interest bearing demand deposits | $ | 206,565 | $ | 121 | 0.24 | % | $ | 218,627 | $ | 128 | 0.23 | % | $ | 170,598 | $ | 475 | 1.12 | % | |||||||||||||||

| Savings deposits | 310,830 | 109 | 0.14 | % | 291,856 | 114 | 0.16 | % | 231,188 | 199 | 0.35 | % | |||||||||||||||||||||

| Time deposits | 168,764 | 291 | 0.70 | % | 179,076 | 407 | 0.90 | % | 205,485 | 1,053 | 2.06 | % | |||||||||||||||||||||

| Borrowed funds | 49,000 | 155 | 1.28 | % | 83,573 | 323 | 1.54 | % | 65,293 | 418 | 2.57 | % | |||||||||||||||||||||

| Total interest bearing liabilities | 735,159 | 676 | 0.37 | % | 773,132 | 972 | 0.50 | % | 672,564 | 2,145 | 1.28 | % | |||||||||||||||||||||

| Noninterest bearing liabilities | |||||||||||||||||||||||||||||||||

| Noninterest bearing deposits | 393,751 | 385,032 | 264,699 | ||||||||||||||||||||||||||||||

| Accrued interest and other liabilities | 11,175 | 12,772 | 8,336 | ||||||||||||||||||||||||||||||

| Shareholders' equity | 119,034 | 117,263 | 103,646 | ||||||||||||||||||||||||||||||

| Total liabilities and shareholders' equity | $ | 1,259,119 | $ | 1,288,199 | $ | 1,049,245 | |||||||||||||||||||||||||||

| Net interest income (FTE) | $ | 11,265 | $ | 10,674 | $ | 8,942 | |||||||||||||||||||||||||||

| Net interest margin to earning assets (FTE) | 3.79 | % | 3.44 | % | 3.61 | % | |||||||||||||||||||||||||||

Net Interest Income

Net interest income is the amount by which interest income on earning assets exceeds the interest expenses on interest bearing liabilities. Net interest income, which includes loan fees, is influenced by changes in the balance and mix of assets and liabilities and market interest rates. The Corporation exerts some control over these factors; however, FRB monetary policy and competition have a significant impact. For analytical purposes, net interest income is adjusted to a FTE basis by adding the income tax savings from interest on tax exempt loans, and nontaxable investment securities, thus making year-to-year comparisons more meaningful.

Volume and Rate Variance Analysis

The following table sets forth the effect of volume and rate changes on interest income and expense for the periods indicated. For the purpose of this table, changes in interest due to volume and rate were determined as follows:

Volume - change in volume multiplied by the previous period's rate.

Rate - change in the FTE rate multiplied by the previous period's volume.

The change in interest due to both volume and rate has been allocated to volume and rate changes in proportion to the relationship of the absolute dollar amounts of the change in each.

| Three Months Ended | Three Months Ended | |||||||||||||||||||||||||||||

| March 31, 2021 | March 31, 2021 | |||||||||||||||||||||||||||||

| Compared To | Compared To | |||||||||||||||||||||||||||||

| December 31, 2020 | March 31, 2020 | |||||||||||||||||||||||||||||

| Increase (Decrease) Due to | Increase (Decrease) Due to | |||||||||||||||||||||||||||||

| Volume | Rate | Net | Volume | Rate | Net | |||||||||||||||||||||||||

| Changes in interest income | ||||||||||||||||||||||||||||||

| Total loans | $ | (1,511 | ) | $ | 1,841 | $ | 330 | $ | 6,098 | $ | (4,981 | ) | $ | 1,117 | ||||||||||||||||

| Taxable investment securities | (16 | ) | (20 | ) | (36 | ) | 77 | (228 | ) | (151 | ) | |||||||||||||||||||

| Nontaxable investment securities | 17 | (15 | ) | 2 | 116 | (92 | ) | 24 | ||||||||||||||||||||||

| Federal funds sold | — | — | — | (58 | ) | (58 | ) | (116 | ) | |||||||||||||||||||||

| Interest earning cash and cash equivalents | — | (4 | ) | (4 | ) | 129 | (144 | ) | (15 | ) | ||||||||||||||||||||

| Federal Home Loan Bank stock | — | 3 | 3 | 16 | (21 | ) | (5 | ) | ||||||||||||||||||||||

| Total changes in interest income | (1,510 | ) | 1,805 | 295 | 6,378 | (5,524 | ) | 854 | ||||||||||||||||||||||

| Changes in interest expense | ||||||||||||||||||||||||||||||

| Interest bearing demand deposits | (29 | ) | 22 | (7 | ) | 560 | (914 | ) | (354 | ) | ||||||||||||||||||||

| Savings deposits | 38 | (43 | ) | (5 | ) | 321 | (411 | ) | (90 | ) | ||||||||||||||||||||

| Time deposits | (24 | ) | (92 | ) | (116 | ) | (162 | ) | (600 | ) | (762 | ) | ||||||||||||||||||

| Borrowed funds | (119 | ) | (49 | ) | (168 | ) | (87 | ) | (176 | ) | (263 | ) | ||||||||||||||||||

| Total changes in interest expense | (134 | ) | (162 | ) | (296 | ) | 632 | (2,101 | ) | (1,469 | ) | |||||||||||||||||||

| Net change in net interest income (FTE) | $ | (1,376 | ) | $ | 1,967 | $ | 591 | $ | 5,746 | $ | (3,423 | ) | $ | 2,323 | ||||||||||||||||

| Average Yield/Rate for the Three Month Periods Ended | |||||||||||||||

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | |||||||||||

| Total earning assets | 4.01 | % | 3.75 | % | 3.97 | % | 3.94 | % | 4.47 | % | |||||

| Total interest bearing liabilities | 0.37 | % | 0.50 | % | 0.63 | % | 0.91 | % | 1.28 | % | |||||

| Net interest margin to earning assets (FTE) | 3.79 | % | 3.44 | % | 3.58 | % | 3.37 | % | 3.61 | % | |||||

| Quarter to Date Net Interest Income (FTE) | ||||||||||||||||||||

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| Interest income | $ | 11,919 | $ | 11,624 | $ | 12,070 | $ | 11,215 | $ | 11,070 | ||||||||||

| FTE adjustment | 22 | 22 | 21 | 18 | 17 | |||||||||||||||

| Total interest income (FTE) | 11,941 | 11,646 | 12,091 | 11,233 | 11,087 | |||||||||||||||

| Total interest expense | 676 | 972 | 1,189 | 1,618 | 2,145 | |||||||||||||||

| Net interest income (FTE) | $ | 11,265 | $ | 10,674 | $ | 10,902 | $ | 9,615 | $ | 8,942 | ||||||||||

Noninterest Income

| Quarter to Date | ||||||||||||||||||||||||

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||||||

| Net gain on sales of mortgage loans | $ | 1,845 | $ | 2,545 | $ | 3,064 | $ | 3,869 | $ | 1,803 | ||||||||||||||

| Trust and investment services | 468 | 445 | 464 | 321 | 389 | |||||||||||||||||||

| ATM and debit card income | 448 | 437 | 460 | 394 | 355 | |||||||||||||||||||

| PPP referral fees | 351 | — | — | — | — | |||||||||||||||||||

| Mortgage servicing fees | 335 | 325 | 293 | 270 | 262 | |||||||||||||||||||

| Service charges on deposit accounts | 166 | 194 | 177 | 119 | 219 | |||||||||||||||||||

| Net mortgage servicing rights income | 138 | 509 | 559 | (163 | ) | (50 | ) | |||||||||||||||||

| Net gain on sales of commercial loans | — | — | — | — | 668 | |||||||||||||||||||

| Net gain from corporate owned life insurance death benefit | — | — | — | 173 | — | |||||||||||||||||||

| Change in fair value of equity investments | (19 | ) | (3 | ) | 2 | 7 | 749 | |||||||||||||||||

| Other income and fees | 122 | 224 | 140 | 302 | 118 | |||||||||||||||||||

| Total noninterest income | $ | 3,854 | $ | 4,676 | $ | 5,159 | $ | 5,292 | $ | 4,513 | ||||||||||||||

| Residential mortgage operations | $ | 2,318 | $ | 3,379 | $ | 3,916 | $ | 3,976 | $ | 2,015 | ||||||||||||||

| Year to Date March 31 | Variance | ||||||||||||||||||

| 2021 | 2020 | Amount | % | ||||||||||||||||

| Net gain on sales of mortgage loans | $ | 1,845 | $ | 1,803 | $ | 42 | 2.33 | % | |||||||||||

| Trust and investment services | 468 | 389 | 79 | 20.31 | % | ||||||||||||||

| ATM and debit card income | 448 | 355 | 93 | 26.20 | % | ||||||||||||||

| PPP referral fees | 351 | — | 351 | — | % | ||||||||||||||

| Mortgage servicing fees | 335 | 262 | 73 | 27.86 | % | ||||||||||||||

| Service charges on deposit accounts | 166 | 219 | (53 | ) | (24.20 | ) | % | ||||||||||||

| Net mortgage servicing rights income | 138 | (50 | ) | 188 | (376.00 | ) | % | ||||||||||||

| Net gain on sales of commercial loans | — | 668 | (668 | ) | (100.00 | ) | % | ||||||||||||

| Net gain from corporate owned life insurance death benefit | — | — | — | — | % | ||||||||||||||

| Change in fair value of equity investments | (19 | ) | 749 | (768 | ) | (102.54 | ) | % | |||||||||||

| Other income and fees | 122 | 118 | 4 | 3.39 | % | ||||||||||||||

| Total noninterest income | $ | 3,854 | $ | 4,513 | $ | (659 | ) | (14.60 | ) | % | |||||||||

| Residential mortgage operations | $ | 2,318 | $ | 2,015 | 303 | 15.04 | % | ||||||||||||

Residential Mortgage Operations

Net gain on sales of mortgage loans represents the income earned on the sale of residential mortgage loans into the secondary market. Throughout 2020, the interest rate environment was advantageous for residential mortgage originations and refinancing, resulting in record gains. Although many consumers continue to face uncertainty related to the overall impact of the COVID-19 pandemic, residential mortgage originations and refinancing activity was robust throughout 2020 and into the first quarter of 2021. Through March 31, 2021, home values continue to rise primarily due to inventory shortages.

Mortgage servicing fees includes the fees earned for servicing loans that have been sold into the secondary market. The increase in mortgage servicing fees is directly related to the increase in the size of the serviced portfolio. Mortgage servicing fees are expected to increase throughout the remainder of 2021 as the Corporation continues to add to the serviced portfolio.

Net mortgage servicing rights income represents income generated from the capitalization of mortgage servicing rights, net of amortization and impairment. In each of the first two quarters of 2020, the Corporation recognized impairments in its servicing portfolio as a direct result of the low interest rate environment and record level of refinancing activity. During the third and fourth quarters of 2020 these impairments had recovered. The Corporation expects net mortgage servicing rights income to continue to increase as the Corporation adds to the serviced portfolio.

Throughout the remainder of 2021, overall revenues from residential mortgage operations (net gain from sale of mortgage loans, mortgage servicing fees, and net mortgage servicing rights income) are not expected to reach the elevated levels experienced during 2020 due to the constrained housing inventory and rising interest rates.

All Other Noninterest Income

Trust and investment services includes income the Corporation earned from contracts with customers to manage assets for investment and/or to transact on their accounts. Income generated from trust services has remained stable from fiduciary fees for estate settlement services and portfolio management. Revenue from wealth management has increased due to strong demand from customers for annuities and long-term care insurance products. Both the trust services and wealth management programs are subject to market fluctuations and interest rate changes. Trust and investment services income is expected to increase modestly throughout 2021.

ATM and debit card income represents fees earned on ATM and debit card transactions. The Corporation expects these fees to increase modestly throughout 2021.

PPP referral fees represents the income earned from the second round of the PPP loan program through the SBA. During the first quarter of 2021, the SBA began processing applications for a second round of PPP loans. The Corporation utilized a third-party vendor to process applications and fund these loans. The Corporation is generating referral fee income for the second round of the PPP loan program. The second round of the PPP loan program ends May 31, 2021. The Corporation expects to earn a nominal amount of PPP referral fees during the second quarter of 2021.

Service charges on deposit accounts includes fees earned from deposit customers for transaction-based, account maintenance and overdraft services. The year-over-year decrease in service charges on deposit accounts is primarily due to a temporary reduction in fees charged due to the COVID-19 pandemic. Service charges on deposit accounts are expected to approximate current levels throughout 2021.

Net gain on sales of commercial loans represents the income earned from the sale of commercial loans into the secondary market. During the first quarter of 2020, the Corporation sold the guaranteed portion of one SBA loan and one USDA loan. The Corporation does not expect to receive any gains from the sale of commercial loans in 2021.

Net gain from corporate owned life insurance death benefit is recognized in the event of the death of an insured individual. The death of an insured individual occurred in the second quarter of 2020. The Corporation does not expect to receive any gains from COLI death benefits in 2021.

Change in fair value of equity investments represents the income earned on equities held in the Corporation's investment portfolio. During the first quarter of 2020, the Corporation recorded a $732 gain from an equity investment in a financial institution that was sold. The Corporation does not anticipate any significant changes in fair value from equity sales in the foreseeable future.

Other income and fees includes miscellaneous other income items, none of which are individually significant. Other income and fees are expected to approximate current levels throughout 2021.

Noninterest Expenses

| Quarter to Date | ||||||||||||||||||||

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| Total compensation | $ | 5,004 | $ | 4,958 | $ | 4,531 | $ | 4,252 | $ | 4,248 | ||||||||||

| Furniture and equipment | 637 | 607 | 614 | 618 | 610 | |||||||||||||||

| Professional services | 624 | 938 | 524 | 571 | 522 | |||||||||||||||

| Data processing | 509 | 501 | 503 | 535 | 442 | |||||||||||||||

| Occupancy | 495 | 475 | 491 | 435 | 476 | |||||||||||||||

| Loan and collection | 406 | 359 | 292 | 229 | 162 | |||||||||||||||

| Advertising and promotional | 284 | 184 | 284 | 255 | 252 | |||||||||||||||

| FDIC insurance premiums | 155 | 59 | 55 | 59 | 55 | |||||||||||||||

| ATM and debit card | 122 | 125 | 109 | 92 | 108 | |||||||||||||||

| Telephone and communication | 94 | 64 | 91 | 86 | 96 | |||||||||||||||

| Amortization of core deposit intangibles | 68 | 90 | 91 | 90 | 90 | |||||||||||||||

| FHLB prepayment penalty | — | 1,907 | — | — | — | |||||||||||||||

| Other general and administrative | 633 | 704 | 633 | 587 | 625 | |||||||||||||||

| Total noninterest expenses | $ | 9,031 | $ | 10,971 | $ | 8,218 | $ | 7,809 | $ | 7,686 | ||||||||||

| Year to Date March 31 | Variance | ||||||||||||||||

| 2021 | 2020 | Amount | % | ||||||||||||||

| Total compensation | $ | 5,004 | $ | 4,248 | $ | 756 | 17.80 | % | |||||||||

| Furniture and equipment | 637 | 610 | 27 | 4.43 | % | ||||||||||||

| Professional services | 624 | 522 | 102 | 19.54 | % | ||||||||||||

| Data processing | 509 | 442 | 67 | 15.16 | % | ||||||||||||

| Occupancy | 495 | 476 | 19 | 3.99 | % | ||||||||||||

| Loan and collection | 406 | 162 | 244 | 150.62 | % | ||||||||||||

| Advertising and promotional | 284 | 252 | 32 | 12.70 | % | ||||||||||||

| FDIC insurance premiums | 155 | 55 | 100 | 181.82 | % | ||||||||||||

| ATM and debit card | 122 | 108 | 14 | 12.96 | % | ||||||||||||

| Telephone and communication | 94 | 96 | (2 | ) | (2.08 | ) | % | ||||||||||

| Amortization of core deposit intangibles | 68 | 90 | (22 | ) | (24.44 | ) | % | ||||||||||

| FHLB prepayment penalty | — | — | — | — | % | ||||||||||||

| Other general and administrative | 633 | 625 | 8 | 1.28 | % | ||||||||||||

| Total noninterest expenses | $ | 9,031 | $ | 7,686 | $ | 1,345 | 17.50 | % | |||||||||

Total compensation includes salaries, commissions and incentives, employee benefits, and payroll taxes. Total compensation has increased due to annual merit increases and an increase in commissions and incentives paid. Fluctuations in commissions and incentives are primarily driven by residential mortgage originations, which can vary significantly from period to period, however, commissions are expected to decline throughout 2021 as mortgage originations decline.

Furniture and equipment and occupancy expenses primarily consist of depreciation, repairs and maintenance, property taxes, utilities, insurance, certain service contracts, and other related items. These expenses are expected to increase with the size and complexity of the Corporation.

Professional services include expenses relating to third-party professional services. These services include, but are not limited to, regulatory, auditing, consulting, and legal. These expenses are expected to increase in future periods to ensure compliance with audit and regulatory requirements.

Data processing primarily includes the expenses relating to the Corporation's core data processor. These expenses are expected to increase throughout 2021 with the size and complexity of the Corporation.

Loan and collection includes expenses related to the origination and collection of loans. The increase in expenses throughout 2020 and into the first quarter of 2021 is a direct result of increased loan volume due to the low interest rate environment created by the Federal Reserve Bank's response to the COVID-19 pandemic. Loan and collection expenses will likely moderate throughout the remainder of 2021, due to diminishing residential mortgage refinancing demand.

Advertising and promotional includes the Corporation's media costs and any donations or sponsorships made on behalf of the Corporation. The annual increase in expenses is a direct result of the Corporation enhancing its marketing efforts to attract new and expand existing customer loan and deposit accounts. In addition to traditional marketing strategies, the Corporation rolled out a new branding strategy in 2020, which resulted in elevated advertising and promotional expenses. Total advertising and promotional expenses are expected to increase in 2021 due to the growth of the Corporation.

FDIC insurance premiums typically fluctuate based on the size of the Corporation's balance sheet, capital position, overall risk profile, and examination ratings. FDIC insurance premiums are expected to increase throughout the remainder of 2021 primarily due to the Corporation's growth in total assets.

ATM and debit card expenses fluctuate based on customer and non-customer utilization of ATMs and customer debit card volumes. The Corporation expects these fees to increase modestly throughout 2021.

Telephone and communication includes expenses relating to the Corporation's communication systems. These expenses are expected to increase throughout 2021 primarily due to the growth of the Corporation.

Amortization of core deposit intangibles relates to the core deposits acquired from Community Bancorp, Inc. on December 31, 2016 and is expected to continue to decline as the core deposit intangible is being amortized based on the sum-of-years-digits method.

During the fourth quarter of 2020, the Corporation paid off three Federal Home Loan Bank borrowings, totaling $30,000. The Corporation incurred a one-time early payoff fee in the amount $1,907. The payoff was executed to enhance net interest income and net interest margins in each of the next three years. The weighted average rate of the three FHLB borrowings was 2.17%. As a result of the early payoffs, the Corporation is expected to reduce interest expense by approximately $660 during 2021.

Other general and administrative includes miscellaneous other expense items, none of which are typically significant. Other general and administrative expenses are expected to approximate current levels into the foreseeable future.

Balance Sheet Breakdown and Analysis

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| ASSETS | ||||||||||||||||||||

| Cash and cash equivalents | $ | 121,477 | $ | 46,757 | $ | 75,032 | $ | 35,190 | $ | 71,140 | ||||||||||

| Total investment securities | 89,772 | 76,111 | 78,179 | 75,526 | 76,312 | |||||||||||||||

| Residential mortgage loans held-for-sale, at fair value | 26,322 | 27,306 | 34,833 | 46,354 | 21,154 | |||||||||||||||

| Gross loans | 1,028,117 | 1,066,562 | 1,060,885 | 1,044,564 | 865,577 | |||||||||||||||

| Less allowance for loan losses | 11,100 | 10,900 | 10,100 | 8,991 | 7,250 | |||||||||||||||

| Net loans | 1,017,017 | 1,055,662 | 1,050,785 | 1,035,573 | 858,327 | |||||||||||||||

| All other assets | 48,206 | 45,610 | 46,016 | 45,051 | 44,247 | |||||||||||||||

| Total assets | $ | 1,302,794 | $ | 1,251,446 | $ | 1,284,845 | $ | 1,237,694 | $ | 1,071,180 | ||||||||||

| LIABILITIES AND SHAREHOLDERS' EQUITY | ||||||||||||||||||||

| Total deposits | $ | 1,122,508 | $ | 1,071,976 | $ | 1,061,470 | $ | 1,018,287 | $ | 883,837 | ||||||||||

| Total borrowed funds | 49,000 | 49,000 | 96,217 | 96,217 | 71,500 | |||||||||||||||

| Accrued interest payable and other liabilities | 12,227 | 14,602 | 13,077 | 14,221 | 11,015 | |||||||||||||||

| Total liabilities | 1,183,735 | 1,135,578 | 1,170,764 | 1,128,725 | 966,352 | |||||||||||||||

| Total shareholders' equity | 119,059 | 115,868 | 114,081 | 108,969 | 104,828 | |||||||||||||||

| Total liabilities and shareholders' equity | $ | 1,302,794 | $ | 1,251,446 | $ | 1,284,845 | $ | 1,237,694 | $ | 1,071,180 | ||||||||||

| 3/31/2021 vs 12/31/2020 | 3/31/2021 vs 3/31/2020 | |||||||||||||||||

| Variance | Variance | |||||||||||||||||

| Amount | % | Amount | % | |||||||||||||||

| ASSETS | ||||||||||||||||||

| Cash and cash equivalents | $ | 74,720 | 159.80 | % | $ | 50,337 | 70.76 | % | ||||||||||

| Total investment securities | 13,661 | 17.95 | % | 13,460 | 17.64 | % | ||||||||||||

| Residential mortgage loans held-for-sale, at fair value | (984 | ) | (3.60 | ) | % | 5,168 | 24.43 | % | ||||||||||

| Gross loans | (38,445 | ) | (3.60 | ) | % | 162,540 | 18.78 | % | ||||||||||

| Less allowance for loan losses | 200 | 1.83 | % | 3,850 | 53.10 | % | ||||||||||||

| Net loans | (38,645 | ) | (3.66 | ) | % | 158,690 | 18.49 | % | ||||||||||

| All other assets | 2,596 | 5.69 | % | 3,959 | 8.95 | % | ||||||||||||

| Total assets | $ | 51,348 | 4.10 | % | $ | 231,614 | 21.62 | % | ||||||||||

| LIABILITIES AND SHAREHOLDERS' EQUITY | ||||||||||||||||||

| Total deposits | $ | 50,532 | 4.71 | % | $ | 238,671 | 27.00 | % | ||||||||||

| Total borrowed funds | — | — | % | (22,500 | ) | (31.47 | ) | % | ||||||||||

| Accrued interest payable and other liabilities | (2,375 | ) | (16.26 | ) | % | 1,212 | 11.00 | % | ||||||||||

| Total liabilities | 48,157 | 2.18 | % | 217,383 | 11.75 | % | ||||||||||||

| Total shareholders' equity | 3,191 | 2.75 | % | 14,231 | 13.58 | % | ||||||||||||

| Total liabilities and shareholders' equity | $ | 51,348 | 4.10 | % | $ | 231,614 | 21.62 | % | ||||||||||

Cash and cash equivalents

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| Cash and cash equivalents | ||||||||||||||||||||

| Noninterest bearing | $ | 25,698 | $ | 23,102 | $ | 22,108 | $ | 20,369 | $ | 33,312 | ||||||||||

| Interest bearing | 95,779 | 23,655 | 52,924 | 14,821 | 37,828 | |||||||||||||||

| Federal funds sold | — | — | — | — | — | |||||||||||||||

| Cash and cash equivalents | $ | 121,477 | $ | 46,757 | $ | 75,032 | $ | 35,190 | $ | 71,140 | ||||||||||

| 3/31/2021 vs 12/31/2020 | 3/31/2021 vs 3/31/2020 | |||||||||||||||||||

| Variance | Variance | |||||||||||||||||||

| Amount | % | Amount | % | |||||||||||||||||

| Cash and cash equivalents | ||||||||||||||||||||

| Noninterest bearing | $ | 2,596 | 11.24 | % | $ | (7,614 | ) | (22.86 | )% | |||||||||||

| Interest bearing | 72,124 | 304.90 | % | 57,951 | 153.20 | % | ||||||||||||||

| Federal funds sold | — | — | % | — | — | % | ||||||||||||||

| Cash and cash equivalents | $ | 74,720 | 159.80 | % | $ | 50,337 | 70.76 | % | ||||||||||||

Cash and cash equivalents, which is comprised of cash and due from banks and federal funds sold, fluctuate from period to period based on loan demand and variances in deposit accounts. In recent periods, the Corporation has experienced an inflow of customer deposits resulting in historically high levels of cash and cash equivalents. The increase in interest bearing cash in the first quarter of 2021 is primarily due to funds received from the SBA for forgiveness of PPP loans. The Corporation expects cash and cash equivalents to remain elevated over the remainder of the year due to additional forgiveness of outstanding PPP loans and the current interest rate environment.

Primary and secondary liquidity sources

While the Corporation continues to maintain a strong liquidity position, it is important to monitor all liquidity sources. The following table outlines the Corporation's primary and secondary sources of liquidity as of:

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| Cash and cash equivalents | $ | 121,477 | $ | 46,757 | $ | 75,032 | $ | 35,190 | $ | 71,140 | ||||||||||

| Unpledged investment securities | 76,384 | 59,025 | 58,739 | 52,647 | 51,889 | |||||||||||||||

| FHLB borrowing availability | 140,000 | 140,000 | 97,500 | 97,500 | 42,500 | |||||||||||||||

| Federal funds purchased lines of credit | 21,500 | 21,500 | 21,500 | 21,500 | 17,500 | |||||||||||||||

| Funds available through the Fed Discount Window | 10,000 | 10,000 | 10,000 | 10,000 | 10,000 | |||||||||||||||

| PPPLF | 122,583 | 177,845 | 206,343 | 202,184 | — | |||||||||||||||

| Total liquidity sources | $ | 491,944 | $ | 455,127 | $ | 469,114 | $ | 419,021 | $ | 193,029 | ||||||||||

Total investment securities

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||||||

| Available-for-sale | ||||||||||||||||||||||||

| U.S. Government and federal agency | $ | 5,942 | $ | 7,935 | $ | 19,311 | $ | 21,339 | $ | 23,610 | ||||||||||||||

| State and municipal | 17,080 | 15,768 | 15,729 | 14,115 | 10,657 | |||||||||||||||||||

| Mortgage backed residential | 32,135 | 19,101 | 20,886 | 12,335 | 10,176 | |||||||||||||||||||

| Certificates of deposit | 4,932 | 5,180 | 5,921 | 6,665 | 8,644 | |||||||||||||||||||

| Collateralized mortgage obligations - agencies | 25,505 | 23,110 | 11,141 | 15,736 | 18,288 | |||||||||||||||||||

| Unrealized gain/(loss) on available-for-sale securities | 1,117 | 1,932 | 2,099 | 2,242 | 1,735 | |||||||||||||||||||

| Total available-for-sale | 86,711 | 73,026 | 75,087 | 72,432 | 73,110 | |||||||||||||||||||

| Held-to-maturity state and municipal | 1,968 | 1,973 | 1,977 | 1,981 | 2,091 | |||||||||||||||||||

| Equity securities | 1,093 | 1,112 | 1,115 | 1,113 | 1,111 | |||||||||||||||||||

| Total investment securities | $ | 89,772 | $ | 76,111 | $ | 78,179 | $ | 75,526 | $ | 76,312 | ||||||||||||||

| 3/31/2021 vs 12/31/2020 | 3/31/2021 vs 3/31/2020 | |||||||||||||||||||||||

| Variance | Variance | |||||||||||||||||||||||

| Amount | % | Amount | % | |||||||||||||||||||||

| Available-for-sale | ||||||||||||||||||||||||

| U.S. Government and federal agency | $ | (1,993 | ) | (25.12 | ) | % | $ | (17,668 | ) | (74.83 | ) | % | ||||||||||||

| State and municipal | 1,312 | 8.32 | % | 6,423 | 60.27 | % | ||||||||||||||||||

| Mortgage backed residential | 13,034 | 68.24 | % | 21,959 | 215.79 | % | ||||||||||||||||||

| Certificates of deposit | (248 | ) | (4.79 | ) | % | (3,712 | ) | (42.94 | ) | % | ||||||||||||||

| Collateralized mortgage obligations - agencies | 2,395 | 10.36 | % | 7,217 | 39.46 | % | ||||||||||||||||||

| Unrealized gain/(loss) on available-for-sale securities | (815 | ) | (42.18 | ) | % | (618 | ) | (35.62 | ) | % | ||||||||||||||

| Total available-for-sale | 13,685 | 18.74 | % | 13,601 | 18.60 | % | ||||||||||||||||||

| Held-to-maturity state and municipal | (5 | ) | (0.25 | ) | % | (123 | ) | (5.88 | ) | % | ||||||||||||||

| Equity securities | (19 | ) | (1.71 | ) | % | (18 | ) | (1.62 | ) | % | ||||||||||||||

| Total investment securities | $ | 13,661 | 17.95 | % | $ | 13,460 | 17.64 | % | ||||||||||||||||

The amortized cost and fair value of AFS investment securities as of March 31, 2021 were as follows:

| Maturing | ||||||||||||||||||||||||

| Due in One Year or Less | After One Year But Within Five Years | After Five Years But Within Ten Years | After Ten Years | Securities with Variable Monthly Payments or Noncontractual Maturities | Total | |||||||||||||||||||

| U.S. Government and federal agency | $ | 4,975 | $ | 967 | $ | — | $ | — | $ | — | $ | 5,942 | ||||||||||||

| State and municipal | 3,239 | 5,952 | 6,005 | 1,884 | — | 17,080 | ||||||||||||||||||

| Mortgage backed residential | — | — | — | — | 32,135 | 32,135 | ||||||||||||||||||

| Certificates of deposit | 1,726 | 3,206 | — | — | — | 4,932 | ||||||||||||||||||

| Collateralized mortgage obligations - agencies | — | — | — | — | 25,505 | 25,505 | ||||||||||||||||||

| Total amortized cost | $ | 9,940 | $ | 10,125 | $ | 6,005 | $ | 1,884 | $ | 57,640 | $ | 85,594 | ||||||||||||

| Fair value | $ | 10,125 | $ | 10,728 | $ | 6,066 | $ | 2,110 | $ | 57,682 | $ | 86,711 | ||||||||||||

The amortized cost and fair value of HTM investment securities as of March 31, 2021 were as follows:

| Maturing | ||||||||||||||||||||||||

| Due in One Year or Less | After One Year But Within Five Years | After Five Years But Within Ten Years | After Ten Years | Securities with Variable Monthly Payments or Noncontractual Maturities | Total | |||||||||||||||||||

| State and municipal | $ | 783 | $ | 805 | $ | 380 | $ | — | $ | — | $ | 1,968 | ||||||||||||

| Fair value | $ | 792 | $ | 840 | $ | 400 | $ | — | $ | — | $ | 2,032 | ||||||||||||

During the first quarter of 2021, the the Corporation expanded its investment portfolio to generate additional interest income. Total investment securities are expected to continue to grow throughout 2021 as management expects deposits to continue to grow at historically high levels while competition for quality loans remains robust. The following table summarizes information as of March 31, 2021 for investment securities purchased YTD:

| Book Value | Fully Taxable Equivalent Weighted Average Yield |

||||||

| U.S. Government and federal agency | $ | — | — | % | |||

| State and municipal | 1,360 | 0.96 | % | ||||

| Collateralized mortgage obligations - agencies | 4,906 | 1.08 | % | ||||

| Certificates of deposit | — | — | % | ||||

| Mortgage backed residential | 15,328 | 1.52 | % | ||||

| Held-to-maturity state and municipal | — | — | % | ||||

| Total | $ | 21,594 | 1.38 | % | |||

Residential mortgage loans held-for-sale, at fair value

Loans HFS represent the fair value of loans that have been committed to be sold to the secondary market, but have not yet been delivered. The level of loans HFS fluctuates based on loan demand as well as the timing of loan deliveries to the secondary market.

Loans and allowance for loan losses

The following tables outline the composition and changes in the loan portfolio as of:

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| Commercial | $ | 183,276 | $ | 241,424 | $ | 271,113 | $ | 260,440 | $ | 67,731 | ||||||||||

| Commercial real estate | 541,428 | 517,054 | 483,275 | 469,039 | 462,561 | |||||||||||||||

| Total commercial loans | 724,704 | 758,478 | 754,388 | 729,479 | 530,292 | |||||||||||||||

| Residential mortgage | 258,333 | 262,770 | 261,375 | 268,295 | 285,392 | |||||||||||||||

| Home equity | 40,205 | 39,900 | 39,456 | 40,114 | 43,222 | |||||||||||||||

| Total residential real estate loans | 298,538 | 302,670 | 300,831 | 308,409 | 328,614 | |||||||||||||||

| Consumer | 4,875 | 5,414 | 5,666 | 6,676 | 6,671 | |||||||||||||||

| Gross loans | 1,028,117 | 1,066,562 | 1,060,885 | 1,044,564 | 865,577 | |||||||||||||||

| Allowance for loan losses | (11,100 | ) | (10,900 | ) | (10,100 | ) | (8,991 | ) | (7,250 | ) | ||||||||||

| Loans, net | $ | 1,017,017 | $ | 1,055,662 | $ | 1,050,785 | $ | 1,035,573 | $ | 858,327 | ||||||||||

| 3/31/2021 vs 12/31/2020 | 3/31/2021 vs 3/31/2020 | |||||||||||||||||||

| Variance | Variance | |||||||||||||||||||

| Amount | % | Amount | % | |||||||||||||||||

| Commercial | $ | (58,148 | ) | (24.09 | )% | $ | 115,545 | 170.59 | % | |||||||||||

| Commercial real estate | 24,374 | 4.71 | % | 78,867 | 17.05 | % | ||||||||||||||

| Total commercial loans | (33,774 | ) | (4.45 | )% | 194,412 | 36.66 | % | |||||||||||||

| Residential mortgage | (4,437 | ) | (1.69 | )% | (27,059 | ) | (9.48 | )% | ||||||||||||

| Home equity | 305 | 0.76 | % | (3,017 | ) | (6.98 | )% | |||||||||||||

| Total residential real estate loans | (4,132 | ) | (1.37 | )% | (30,076 | ) | (9.15 | )% | ||||||||||||

| Consumer | (539 | ) | (9.96 | )% | (1,796 | ) | (26.92 | )% | ||||||||||||

| Gross loans | (38,445 | ) | (3.60 | )% | 162,540 | 18.78 | % | |||||||||||||

| Allowance for loan losses | (200 | ) | 1.83 | % | (3,850 | ) | 53.10 | % | ||||||||||||

| Loans, net | $ | (38,645 | ) | (3.66 | )% | $ | 158,690 | 18.49 | % | |||||||||||

The following table presents historical loan balances by portfolio segment and impairment evaluation as of:

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| Loans collectively evaluated for impairment | ||||||||||||||||||||

| Commercial | $ | 183,203 | $ | 241,424 | $ | 271,113 | $ | 260,440 | $ | 67,731 | ||||||||||

| Commercial real estate | 532,294 | 508,182 | 481,071 | 465,749 | 460,903 | |||||||||||||||

| Residential mortgage | 257,543 | 262,017 | 260,665 | 267,632 | 284,662 | |||||||||||||||

| Home equity | 40,141 | 39,874 | 39,456 | 40,114 | 43,222 | |||||||||||||||

| Consumer | 4,875 | 5,412 | 5,663 | 6,673 | 6,666 | |||||||||||||||

| Subtotal | 1,018,056 | 1,056,909 | 1,057,968 | 1,040,608 | 863,184 | |||||||||||||||

| Loans individually evaluated for impairment | ||||||||||||||||||||

| Commercial | 73 | — | — | — | — | |||||||||||||||

| Commercial real estate | 9,134 | 8,872 | 2,204 | 3,290 | 1,658 | |||||||||||||||

| Residential mortgage | 790 | 753 | 710 | 663 | 730 | |||||||||||||||

| Home equity | 64 | 26 | — | — | — | |||||||||||||||

| Consumer | — | 2 | 3 | 3 | 5 | |||||||||||||||

| Subtotal | 10,061 | 9,653 | 2,917 | 3,956 | 2,393 | |||||||||||||||

| Gross Loans | $ | 1,028,117 | $ | 1,066,562 | $ | 1,060,885 | $ | 1,044,564 | $ | 865,577 | ||||||||||

The following table presents historical allowance for loan losses allocations by portfolio segment and impairment evaluation as of:

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| Loans collectively evaluated for impairment | ||||||||||||||||||||

| Commercial | $ | 626 | $ | 673 | $ | 633 | $ | 536 | $ | 479 | ||||||||||

| Commercial real estate | 6,026 | 5,602 | 5,152 | 4,595 | 3,655 | |||||||||||||||

| Residential mortgage | 3,280 | 3,480 | 3,479 | 3,278 | 2,607 | |||||||||||||||

| Home equity | 453 | 440 | 438 | 372 | 298 | |||||||||||||||

| Consumer | 92 | 97 | 101 | 102 | 89 | |||||||||||||||

| Subtotal | 10,477 | 10,292 | 9,803 | 8,883 | 7,128 | |||||||||||||||

| Loans individually evaluated for impairment | ||||||||||||||||||||

| Commercial | — | — | — | — | — | |||||||||||||||

| Commercial real estate | 619 | 602 | 289 | 100 | 111 | |||||||||||||||

| Residential mortgage | 4 | 4 | 5 | 5 | 6 | |||||||||||||||

| Home equity | — | — | — | — | — | |||||||||||||||

| Consumer | — | 2 | 3 | 3 | 5 | |||||||||||||||

| Subtotal | 623 | 608 | 297 | 108 | 122 | |||||||||||||||

| Allowance for loan losses | $ | 11,100 | $ | 10,900 | $ | 10,100 | $ | 8,991 | $ | 7,250 | ||||||||||

| Commercial | $ | 626 | $ | 673 | $ | 633 | $ | 536 | $ | 479 | ||||||||||

| Commercial real estate | 6,645 | 6,204 | 5,441 | 4,695 | 3,766 | |||||||||||||||

| Residential mortgage | 3,284 | 3,484 | 3,484 | 3,283 | 2,613 | |||||||||||||||

| Home equity | 453 | 440 | 438 | 372 | 298 | |||||||||||||||

| Consumer | 92 | 99 | 104 | 105 | 94 | |||||||||||||||

| Allowance for loan losses | $ | 11,100 | $ | 10,900 | $ | 10,100 | $ | 8,991 | $ | 7,250 | ||||||||||

The following table summarizes the Corporation's current, past due, and nonaccrual loans as of:

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| Accruing interest | ||||||||||||||||||||

| Current | $ | 1,018,343 | $ | 1,057,404 | $ | 1,058,437 | $ | 1,042,589 | $ | 862,581 | ||||||||||

| Past due 30-89 days | 1,636 | 1,165 | 1,703 | 948 | 2,152 | |||||||||||||||

| Past due 90 days or more | 120 | 50 | 86 | 361 | 166 | |||||||||||||||

| Total accruing interest | 1,020,099 | 1,058,619 | 1,060,226 | 1,043,898 | 864,899 | |||||||||||||||

| Nonaccrual | 8,018 | 7,943 | 659 | 666 | 678 | |||||||||||||||

| Total loans | $ | 1,028,117 | $ | 1,066,562 | $ | 1,060,885 | $ | 1,044,564 | $ | 865,577 | ||||||||||

| Total loans past due and in nonaccrual status | $ | 9,774 | $ | 9,158 | $ | 2,448 | $ | 1,975 | $ | 2,996 | ||||||||||

The following table summarizes the Corporation's nonperforming assets as of:

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| Nonaccrual loans | $ | 8,018 | $ | 7,943 | $ | 659 | $ | 666 | $ | 678 | ||||||||||

| Accruing loans past due 90 days or more | 120 | 50 | 86 | 361 | 166 | |||||||||||||||

| Total nonperforming loans | 8,138 | 7,993 | 745 | 1,027 | 844 | |||||||||||||||

| Other real estate owned | — | — | — | — | 400 | |||||||||||||||

| Total nonperforming assets | $ | 8,138 | $ | 7,993 | $ | 745 | $ | 1,027 | $ | 1,244 | ||||||||||

The following table summarizes the Corporation's primary asset quality measures as of:

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | |||||||||||

| Nonperforming loans to gross loans | 0.79 | % | 0.75 | % | 0.07 | % | 0.10 | % | 0.10 | % | |||||

| Nonperforming assets to total assets | 0.62 | % | 0.64 | % | 0.06 | % | 0.08 | % | 0.12 | % | |||||

| Allowance for loan losses to gross loans | 1.08 | % | 1.02 | % | 0.95 | % | 0.86 | % | 0.84 | % | |||||

| Allowance for loan losses to gross loans, less PPP loans | 1.23 | % | 1.23 | % | 1.19 | % | 1.07 | % | 0.84 | % | |||||

During the fourth quarter of 2020, the Corporation transferred one commercial real estate loan with an outstanding principal balance of $7,214 to nonaccrual. The underlying collateral for this loan is an extended stay hotel. The hotel's current cash flow is insufficient to service the debt in accordance with the contractual terms of the note and, as such, the loan continues to be on payment deferrals. A specific reserve has been established for the estimated collateral deficiency (based on a current appraisal), net of a 70% USDA guarantee.

The following table summarizes the balance of net unamortized discounts on purchased loans as of:

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| Net unamortized discount on purchased loans | $ | 580 | $ | 773 | $ | 877 | $ | 1,058 | $ | 1,233 | ||||||||||

The following table summarizes the balance of PPP loans included in commercial loans as of:

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| Outstanding PPP loans | $ | 122,583 | $ | 177,845 | $ | 211,060 | $ | 206,901 | $ | — | ||||||||||

Despite historically strong credit quality indicators, there continues to be significant uncertainty surrounding the overall impact of the COVID-19 pandemic on the loan portfolio. This uncertainty resulted in the Corporation increasing the ALLL by $3,850, or 53.10%, since March 31, 2020. Management will continue to monitor the loan portfolio to ensure that the ALLL remains appropriate.

The following table summarizes the average loan size as of:

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| Commercial | $ | 206 | $ | 169 | $ | 166 | $ | 171 | $ | 214 | ||||||||||

| Commercial real estate | 727 | 707 | 672 | 654 | 644 | |||||||||||||||

| Total commercial loans | 444 | 351 | 321 | 325 | 513 | |||||||||||||||

| Residential mortgage | 183 | 182 | 180 | 177 | 194 | |||||||||||||||

| Home equity | 46 | 45 | 45 | 45 | 46 | |||||||||||||||

| Total residential real estate loans | 131 | 130 | 129 | 128 | 137 | |||||||||||||||

| Consumer | 22 | 22 | 22 | 25 | 26 | |||||||||||||||

| Gross loans | $ | 249 | $ | 226 | $ | 215 | $ | 213 | $ | 234 | ||||||||||

COVID-19, CARES Act and SBA activity

The communities which the Corporation serves are not immune to the fallout of the COVID-19 pandemic. The Corporation has committed significant efforts to work with customers through temporary loan modifications and participation in the PPP loan program through the SBA.

The Corporation considered the modification type on a loan-by-loan basis. Most modifications for loans held within the Corporation's loan portfolio resulted in the deferment of principal and interest payments for 6 months or less.

The Corporation also provides a variety of accommodations for loans that the Corporation services for FHLMC including providing mortgage forbearance for up to 12 months, waiving assessments of penalties and late fees, halting foreclosure actions and evictions, and offering loan modification options that lower payments or keep payments the same after the forbearance period.

As outlined in the following table, the majority of the Corporation's portfolio and serviced loans have returned to normal principal and interest payments. The balance of those loans with deferrals are actively monitored and specific reserves have been established where appropriate.

The table below outlines the active COVID-19 related loan modifications as of March 31, 2021:

| Number of Modifications |

Outstanding Balance |

% of Portfolio | ||||||||

| Commercial | 3 | $ | 1,507 | 0.82 | % | |||||

| Commercial real estate | 5 | 10,506 | 1.94 | % | ||||||

| Total commercial loan modifications | 8 | 12,013 | 1.66 | % | ||||||

| Portfolio residential mortgage loans | 6 | 928 | 0.36 | % | ||||||

| Home equity | 1 | 21 | 0.05 | % | ||||||

| Total residential real estate loan modifications | 7 | 949 | 0.32 | % | ||||||

| Consumer | — | — | — | % | ||||||

| Total portfolio modifications | 15 | $ | 12,962 | 1.26 | % | |||||

| Residential mortgage loans serviced for FHLMC | 32 | $ | 7,002 | 1.29 | % | |||||

The accommodation industry was particularly impacted by the COVID-19 pandemic. Due to executive action put in place by the government, including stay-at-home orders and travel restrictions, hotel occupancy rates were reduced drastically. The Corporation has 18 commercial loans in its portfolio in the accommodation industry with a book balance of $20,033. Of these loans, approximately 53% are government-backed by guarantees from either the SBA or USDA.

The Corporation was extremely active in participating in the PPP loan program. The Corporation funded 1,370 loans totaling $216,205. During the fourth quarter of 2020, the SBA began processing PPP forgiveness applications, which reduced the outstanding balance of PPP loans to $122,583 as of March 31, 2021. As of March 31, 2021, the Corporation received forgiveness payments for 721 PPP loans from the SBA.

The Corporation generated $6,799 in fees from the SBA through the PPP loan program. The income is being recognized over the life of the PPP loans (24 to 60 months) based on the level yield method. As of March 31, 2021, the Corporation has recognized $5,337 in income, with $1,462 remaining as unearned income.

During the first quarter of 2021, the SBA began processing applications for a second round of PPP loans. The Corporation is utilizing a third-party for the processing of applications and funding of these loans. The Corporation is generating referral fee income for the second round of the PPP loan program. As of March 31, 2021, the Corporation generated $351 in referral fees.

All other assets

The following tables outline the composition and changes in other assets as of:

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||

| Premises and equipment, net | $ | 15,969 | $ | 15,461 | $ | 15,267 | $ | 15,323 | $ | 15,533 | ||||||||||

| Corporate owned life insurance | 10,354 | 10,291 | 10,225 | 10,115 | 10,380 | |||||||||||||||

| Accrued interest receivable | 5,451 | 5,068 | 5,645 | 5,266 | 3,124 | |||||||||||||||

| Mortgage servicing rights | 5,023 | 4,885 | 4,376 | 3,816 | 3,980 | |||||||||||||||

| Federal Home Loan Bank stock | 3,488 | 3,488 | 3,488 | 3,488 | 3,150 | |||||||||||||||

| Goodwill | 3,219 | 3,219 | 3,219 | 3,219 | 3,219 | |||||||||||||||

| Right-of-use assets | 1,139 | 364 | 387 | 409 | 432 | |||||||||||||||

| Derivatives | 1,009 | 1,331 | 1,772 | 1,311 | 1,063 | |||||||||||||||

| Core deposit intangibles | 474 | 541 | 632 | 722 | 812 | |||||||||||||||

| Other real estate owned | — | — | — | — | 400 | |||||||||||||||

| Other assets | 2,080 | 962 | 1,005 | 1,382 | 2,154 | |||||||||||||||

| All other assets | $ | 48,206 | $ | 45,610 | $ | 46,016 | $ | 45,051 | $ | 44,247 | ||||||||||

| 3/31/2021 vs 12/31/2020 | 3/31/2021 vs 3/31/2020 | |||||||||||||||||||

| Variance | Variance | |||||||||||||||||||

| Amount | % | Amount | % | |||||||||||||||||

| Premises and equipment, net | $ | 508 | 3.29 | % | $ | 436 | 2.81 | % | ||||||||||||

| Corporate owned life insurance | 63 | 0.61 | % | (26 | ) | (0.25 | )% | |||||||||||||

| Accrued interest receivable | 383 | 7.56 | % | 2,327 | 74.49 | % | ||||||||||||||

| Mortgage servicing rights | 138 | 2.82 | % | 1,043 | 26.21 | % | ||||||||||||||

| Federal Home Loan Bank stock | — | — | % | 338 | 10.73 | % | ||||||||||||||

| Goodwill | — | — | % | — | — | % | ||||||||||||||

| Right-of-use assets | 775 | 212.91 | % | 707 | 163.66 | % | ||||||||||||||

| Derivatives | (322 | ) | (24.19 | )% | (54 | ) | (5.08 | )% | ||||||||||||

| Core deposit intangibles | (67 | ) | (12.38 | )% | (338 | ) | (41.63 | )% | ||||||||||||

| Other real estate owned | — | — | % | (400 | ) | (100.00 | )% | |||||||||||||

| Other assets | 1,118 | 116.22 | % | (74 | ) | (3.44 | )% | |||||||||||||

| All other assets | $ | 2,596 | 5.69 | % | $ | 3,959 | 8.95 | % | ||||||||||||

Mortgage servicing rights are servicing assets that are recognized from the sales of mortgage loans. The increase in mortgage servicing rights is due to the increased volume of residential mortgage loan sales. The Corporation expects the serviced loan portfolio to continue to grow throughout the remainder of 2021.

Right-of-use assets were established pursuant to the adoption of ASU 2016-02, "Leases (Topic 842)", on January 1, 2019. Right-of-use assets are recognized at the lease commencement date based on the estimated present value of the lease payments over the lease term, for leases that are longer than 12 months. The increase in the Corporation's right-of-use assets in the first quarter of 2021 is due to the recognition of two additional lease obligations.

Derivatives represent the fair value of interest rate lock commitments and mandatory forward loan sales commitments that are in a gain position. These balances can fluctuate from period to period based on changes in interest rates and the volume of the Corporation's loan pipeline.

Other assets includes miscellaneous other asset items, none of which are individually significant.

Total deposits

The following tables outline the composition and changes in the deposit portfolio as of:

| 3/31/2021 | 12/31/2020 | 9/30/2020 | 6/30/2020 | 3/31/2020 | ||||||||||||||||||

| Noninterest bearing demand | $ | 422,013 | $ | 378,733 | $ | 391,706 | $ | 383,452 | $ | 281,848 | ||||||||||||

| Interest bearing | ||||||||||||||||||||||

| Savings | 309,454 | 290,343 | 269,051 | 245,957 | 215,748 | |||||||||||||||||

| Money market demand | 109,101 | 113,729 | 99,252 | 90,504 | 79,070 | |||||||||||||||||

| NOW | 103,342 | 101,419 | 120,681 | 122,477 | 83,910 | |||||||||||||||||

| Time deposits | 178,598 | 187,752 | 180,780 | 175,897 | 223,261 | |||||||||||||||||

| Total deposits | $ | 1,122,508 | $ | 1,071,976 | $ | 1,061,470 | $ | 1,018,287 | $ | 883,837 | ||||||||||||

| 3/31/2021 vs 12/31/2020 | 3/31/2021 vs 3/31/2020 | |||||||||||||||||||||

| Variance | Variance | |||||||||||||||||||||

| Amount | % | Amount | % | |||||||||||||||||||

| Noninterest bearing demand | $ | 43,280 | 11.43 | % | $ | 140,165 | 49.73 | % | ||||||||||||||

| Interest bearing | ||||||||||||||||||||||

| Savings | 19,111 | 6.58 | % | 93,706 | 43.43 | % | ||||||||||||||||

| Money market demand | (4,628 | ) | (4.07 | )% | 30,031 | 37.98 | % | |||||||||||||||

| NOW | 1,923 | 1.90 | % | 19,432 | 23.16 | % | ||||||||||||||||

| Time deposits | (9,154 | ) | (4.88 | )% | (44,663 | ) | (20.00 | )% | ||||||||||||||

| Total deposits | $ | 50,532 | 4.71 | % | $ | 238,671 | 27.00 | % | ||||||||||||||

The Corporation has continued its focus of growing non-contractual deposits while supplementing funding with time deposits. The Corporation has been able to drive this meaningful increase through enhanced organic growth strategies. Total deposits also increased due to government related stimulus programs. The Corporation will continue to monitor deposit growth and adjust interest rates in order to minimize downward pressure on margins.

Schedule of time deposit maturities

The following table summarizes the contractual maturities of the time deposits as of March 31, 2021:

| Maturity Buckets | ||||||||||||||||||||

| 3 Months or Less | 3 to 6 Months | 6 to 9 Months | 9 to 12 Months | Beyond 12 Months | ||||||||||||||||

| Balance | $ | 55,976 | $ | 41,742 | $ | 17,035 | $ | 17,217 | $ | 46,628 | ||||||||||

| Weighted average yield | 0.50 | % | 0.69 | % | 0.53 | % | 0.55 | % | 0.77 | % | ||||||||||

| Cumulative Maturities | ||||||||||||||||||||

| 3 Months or Less | Up to 6 Months | Up to 9 Months | Up to 12 Months | Total | ||||||||||||||||

| Balance | $ | 55,976 | $ | 97,718 | $ | 114,753 | $ | 131,970 | $ | 178,598 | ||||||||||

| Weighted average yield | 0.50 | % | 0.58 | % | 0.57 | % | 0.57 | % | 0.62 | % | ||||||||||

The repricing of time deposits will have a significant impact on their weighted average yield. Current rates offered by the Corporation have time deposit rates ranging from 0.05% to 0.55% depending on the term and opening balance.

Total borrowed funds

The following tables outline the composition and changes in borrowed funds as of:

| 3/31/21 |

12/31/20 |

9/30/20 | 6/30/20 |

3/31/20 |

|||||||||||||||||

| Federal Home Loan Bank borrowings | $ | 35,000 | $ | 35,000 | $ | 77,500 | $ | 77,500 | $ | 57,500 | |||||||||||

| Subordinated debentures | 14,000 | 14,000 | 14,000 | 14,000 | 14,000 | ||||||||||||||||

| PPPLF | — | — | 4,717 | 4,717 | — | ||||||||||||||||

| Federal funds purchased | — | — | — | — | — | ||||||||||||||||

| Total borrowed funds | $ | 49,000 | $ | 49,000 | $ | 96,217 | $ | 96,217 | $ | 71,500 | |||||||||||

| 3/31/2021 vs 12/31/2020 | 3/31/2021 vs 3/31/2020 | ||||||||||||||||||||

| Variance | Variance | ||||||||||||||||||||

| Amount |

% |

Amount |

% |

||||||||||||||||||

| Federal Home Loan Bank borrowings | $ | — | — | % | $ | (22,500 | ) | (39.13 | )% | ||||||||||||

| Subordinated debentures | — | — | % | — | — | % | |||||||||||||||

| PPPLF | — | — | % | — | — | % | |||||||||||||||

| Federal funds purchased | — | — | % | — | — | % | |||||||||||||||

| Total borrowed funds | $ | — | — | % | $ | (22,500 | ) | (31.47 | )% | ||||||||||||

The Corporation utilizes a mix of borrowed funds and organic deposit growth to fund loan demand. The increase in Federal Home Loan Bank borrowings in the second quarter of 2020 was solely due to the Corporation funding PPP loans. The decrease in Federal Home Loan Bank borrowings in the fourth quarter of 2020 was primarily due to early payoffs of three FHLB borrowings totaling $30,000.

Total borrowed funds are expected to approximate current levels throughout 2021 as there are no scheduled maturities. The Corporation continually analyzes the market for opportunities and will borrow funds when deemed financially beneficial.

Wholesale funding sources

The following tables outline the composition and changes in wholesale funding sources as of:

| 3/31/21 | 12/31/20 | 9/30/20 | 6/30/20 | 3/31/20 | ||||||||||||||||||||

| Federal Home Loan Bank borrowings | $ | 35,000 | $ | 35,000 | $ | 77,500 | $ | 77,500 | $ | 57,500 | ||||||||||||||

| Brokered money market demand | — | — | 25,029 | 25,010 | — | |||||||||||||||||||

| Brokered time deposits | 20,234 | 20,000 | 28,605 | 28,837 | 28,605 | |||||||||||||||||||

| Subordinated debentures | 14,000 | 14,000 | 14,000 | 14,000 | 14,000 | |||||||||||||||||||

| Internet time deposits | 2,739 | 2,839 | 10,208 | 11,690 | 18,005 | |||||||||||||||||||

| PPPLF | — | — | 4,717 | 4,717 | — | |||||||||||||||||||

| Total wholesale funds | $ | 71,973 | $ | 71,839 | $ | 160,059 | $ | 161,754 | $ | 118,110 | ||||||||||||||

| 3/31/2021 vs 12/31/2020 | 3/31/2021 vs 3/31/2020 | |||||||||||||||||||||||

| Variance | Variance | |||||||||||||||||||||||

| Amount | % | Amount | % | |||||||||||||||||||||

| Federal Home Loan Bank borrowings | $ | — | — | % | $ | (22,500 | ) | (39.13 | ) | % | ||||||||||||||

| Brokered money market demand | — | — | % | — | — | % | ||||||||||||||||||

| Brokered time deposits | 234 | 1.17 | % | (8,371 | ) | (29.26 | ) | % | ||||||||||||||||

| Subordinated debentures | — | — | % | — | — | % | ||||||||||||||||||

| Internet time deposits | (100 | ) | (3.52 | ) | % | (15,266 | ) | (84.79 | ) | % | ||||||||||||||

| PPPLF | — | — | % | — | — | % | ||||||||||||||||||

| Total wholesale funds | $ | 134 | 0.19 | % | $ | (46,137 | ) | (39.06 | ) | % | ||||||||||||||

The Corporation utilizes wholesale funds to manage balance sheet growth. Wholesale funding has historically been more expensive than core deposits, however, due to the COVID-19 pandemic, the FRB has kept Fed funds rates near zero. The Corporation continually analyzes sources of wholesale funding when the increases in interest earning assets out-pace the increases in core deposits.

Accrued interest payable and other liabilities

Accrued interest payable and other liabilities includes accrued interest payable, federal income taxes payable, deferred federal income taxes payable, and all other liabilities (none of which are individually significant). Accrued interest payable and other liabilities are not expected to fluctuate significantly in future periods.

Total shareholders' equity

Total shareholders' equity includes common stock, retained earnings, and AOCI. Total shareholders' equity is expected to continue to grow throughout 2021 through the Corporation's earnings. In April 2020, the Corporation's Board of Directors amended its common stock repurchase plan to authorize the repurchase of up to $5,000 of common stock. During the first quarter of 2021 and the fourth quarter of 2020, the Corporation repurchased 37,315 and 5,342 shares for $880 and $110, respectively.

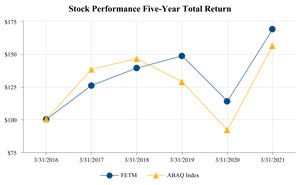

Stock Performance

The following graph compares the cumulative total shareholder return on the Corporation's common stock for the last five years with the cumulative total return on the ABA NASDAQ Community Bank Index (NASDAQ: XX:ABAQ) over the same period. The graph assumes the value of an investment in the Corporation's common stock and the ABA NASDAQ Community Bank Index was $100 at March 31, 2016 and all dividends were reinvested.

The graph accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/bc09497d-59b0-40f3-8bfa-af059451c581

| Date |

FETM |

ABAQ Index |

||||

| 3/31/2016 | 100.00 | 100.00 | ||||

| 3/31/2017 | 125.90 | 138.33 | ||||

| 3/31/2018 | 139.19 | 146.54 | ||||