Pipestone Energy Corp. Provides Its 2020 Capital Budget and Guidance, an Operations Update and Announces the Exercise of an Option to Expand the 8-15 Compression Station

PDF available: http://ml.globenewswire.com/Resource/Download/65a27f45-cd8a-441f-9f16-70ef3df5e984

CALGARY, Alberta, Jan. 16, 2020 (GLOBE NEWSWIRE) -- (PIPE – TSX-V) Pipestone Energy Corp. (“Pipestone Energy” or the “Company”) is pleased to provide an update to our operations as well as the release of our 2020 guidance and development plan.

“I am very pleased to announce that Pipestone Energy produced approximately 17,700 boe/d during December 2019, well in excess of the top-end of our 2019 exit guidance. Well performance has been strong and in-line with our type curve expectations. Our 2020 capital program is 85% weighted to DCE&T expenditures with development concentrated in areas where we expect to realize the highest condensate yields. Exit 2020 production is forecast to grow by approximately 20% over exit 2019, while maintaining a strong balance sheet with a target exit debt to last twelve months EBITDA ratio of less than 1.5x.” stated Paul Wanklyn, President and CEO. “This year’s development places us firmly on a path to fill our installed in-field infrastructure capacity of 33,000 boe/d and generate attractive returns on capital employed over the foreseeable future.”

Q4 and Exit 2019 Production Volumes:

Based on field estimates, Pipestone Energy production averaged 17,700 boe/d (~37% liquids) during December 2019, successfully exceeding its exit 2019 production guidance of 14,000 to 16,000 boe/d. Average Q4 2019 volumes were approximately 15,100 boe/d (~41% total liquids).

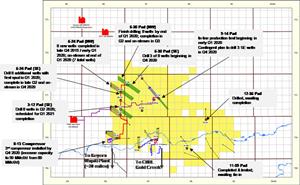

On-stream performance of the new 3rd party infrastructure in late Q3 2019 through Q4 2019 was intermittent while commissioning, leading to significant variability and pad production restrictions. Notwithstanding the infrastructure challenges, aggregate performance from the 20 new wells brought on during 2019 are meeting type curve expectations. On the 3-1 pad (9 wells), over the first 90 days of production (“IP90”), the average well produced ~1,045 boe/d (sales) with a raw gas condensate-gas-ratio (“CGR”) of 108 bbl/MMcf with consistent liquids yields in the Montney ‘B’ and ‘C’. On the 15-14 pad (10 wells), the average well IP90 production rate was ~910 boe/d (sales). The 15-14 pad was the first pad brought on-stream and was disproportionately affected by the 3rd party infrastructure start-up. The average well has produced ~975 boe/d (sales) over the latest 30 producing days. The 15-14 pad has a higher CGR gradation between the Montney benches as compared to the 3-1 pad. The Montney ‘B’ wells (5) on this pad have liquids ratios performing at type curve expectations, with an average IP90 raw gas CGR of 82 bbl/MMcf, while the Montney ‘C’ wells (4) averaged 35 bbl/MMcf over the same period. Thus far, gas productivity from the 15-14 pad Montney ‘C’ wells are outperforming type curve expectations. The single producing well on the 6-24 pad, which was completed in early 2017 utilizing a low intensity frac design, averaged ~1,260 boe/d (sales) over its first 45 producing days with a cumulative raw gas condensate-gas-ratio (“CGR”) of ~160 bbl/MMcf. The focus of Pipestone Energy’s 2020 development program will be in the northwest area and adjacent to our existing gathering systems offsetting the Company’s highest liquids yields observed to date.

Operations Update:

In December, the Company has successfully completed six wells drilled at its 6-24 pad-site using Pipestone’s limited entry or “XLE” design, with an average lateral length of 2,600 metres, and an average proppant loading of 2.9 T/M. These wells were completed at an average total cost of $4.0 million per well. All six wells will be tied-in and on-stream at the end of Q1 2020. An optimized equip & tie-in design on the 6-24 pad is estimated to reduce facility costs from $1.2 million to $0.8 million per well. As a result of these savings, Pipestone Energy is reducing its type well capital cost from $7.5 million to $7.1 million going forward (for a 2,500-metre lateral length well). These incremental cost savings further demonstrate the Company’s track record of reducing well costs while increasing frac intensity; total well costs have been improved by $2.6 million from the initial type well estimate of $9.7 million (~27% savings) since early 2019.

On the 6-30 pad, the Company set surface casing for six new wells during December 2019 and is currently drilling the second well on the pad. Drilling is expected to finish by the end of Q1 2020, with completions to follow during Q2 2020.

Additional Keyera Wapiti Gas Plant Capacity:

In response to growing production expectations, on January 14th, 2020, the Company exercised its option to secure an additional 30 MMcf/day of Priority 1 natural gas gathering, compression, and processing capacity at the Keyera Wapiti Plant beginning in Q4 2020. The additional compressor required to expand the existing 8-15 compressor station will be supplied by Keyera and a significant portion of the facilities work necessary to expand the site was pre-built in 2019. This agreement secures a total of 90 MMcf/d of priority one access to the Keyera Wapiti plant in addition to its existing 30 MMcf/d of priority one access through the Tidewater Pipestone plant for a total of 120 MMcf/d beginning in Q4 2020. Pipestone’s gas plant take-or-pay commitment with Keyera will increase with this additional capacity to 72 MMcf/d in April 2021, from 24 MMcf/d currently. This represents an important step in the continued growth of Pipestone Energy.

Key Highlights:

| Full Year Production | 18,000 boe/d | - | 20,000 boe/d |

| % Liquids | 40 - 45% | - | 40 - 45% |

| Exit Production (1) | 20,000 boe/d | - | 22,000 boe/d |

| Capital Spending | $145 million | - | $155 million |

| Cash Flow (2) | $125 million | - | $135 million |

- Exit production defined as December 2020 average production.

- Cash flow is net of general & administrative and estimated interest costs. Incorporates the following price deck to forecast cash flow: US$57.50 WTI, C$1.75/GJ AECO. Cash Flow is a non-GAAP measure, please see the Advisory Regarding Non-GAAP measures for further details.

Pipestone Energy’s 2020 budget aims to deliver significant year-over-year production growth while maintaining a strong balance sheet. The Company remains focused on efficient capital deployment with a measured growth trajectory that is expected to result in peer leading corporate returns. The focus of Pipestone Energy’s development in 2020 is concentrated in areas of the acreage with the highest projected liquids content and deliverability, while maximizing efficiencies by taking advantage of existing pads and infrastructure.

With the 2019 construction of its in-field gathering system capable of handling ~33,000 boe/d, Pipestone Energy’s capital program is primarily weighted to half-cycle development economics until this capacity is reached. The 2020 capital budget is comprised of ~85% drilling, completion and equip & tie-in expenditures. Included in the remaining capital are downhole frac and production diagnostic tools to better understand and optimize the Company’s completion approach going forward. As well, incremental in-field water management and other infrastructure optimization projects are being executed.

Expected Development Activity Summary:

|

# Wells Drilled (Rig Released) |

# Wells Completed | # New Wells on Production | DUCs at Year End | |

| 2020 Forecast | 24(1) | 12(2) | 18 | 12 |

| 2019 Actuals | 10 | 16 | 20 | - |

- The Company drilled six surface holes on the 6-30 pad in Q4 2019, with all six wells to be rig released in 2020.

- Six fracs on the 6-24 pad were pumped in Q4 2019, with approximately 20% of the completion capital incurred in early Q1 2020.

Risk Management:

The Company continues to implement a robust risk management program to reduce the volatility of its expected cash flows. At the mid-point of its guidance range, Pipestone Energy has approximately 49% of its net after-royalties production hedged for 2020. The weighted average 2020 crude oil swap price is approximately C$79 per barrel and for AECO natural gas is approximately $1.78/Mcf, with hedged gas volumes weighted towards the more volatile summer months of April – October.

2020 Outlook:

Pipestone Energy is well positioned to deliver a combination of attractive year-over-year production growth while generating robust returns on capital employed and maintaining a solid balance sheet. This year’s development expenditures are concentrated around the most condensate-rich results realized to date and weighted 85% to half-cycle DCE&T expenditures. At the mid-point, projected exit production represents growth of ~20% over 2019 exit production, which puts the Company firmly on the path to fill its installed in-field infrastructure capacity of 33,000 boe/d over the next two years.

Pipestone Energy Corp.

Pipestone Energy Corp. is an oil and gas exploration and production company with its head office located in Calgary, Alberta. The company is focused on developing its pure-play condensate-rich Montney asset in the Pipestone area near Grande Prairie, Alberta. Pipestone Energy is committed to building long term value for our shareholders and values the partnerships that it is developing within its operating community. Pipestone Energy shares trade under the symbol PIPE on the TSX Venture Exchange. For more information, visit www.pipestonecorp.com.

Pipestone Energy Contacts:

| Paul Wanklyn President and Chief Executive Officer (587) 392-8407 paul.wanklyn@pipestonecorp.com |

Craig Nieboer Chief Financial Officer (587) 392-8408 craig.nieboer@pipestonecorp.com |

| Dan van Kessel VP Corporate Development (587) 392-8414 dan.vankessel@pipestonecorp.com |

Advisory Regarding Forward-Looking Statements

This news release contains certain information and statements (“forward-looking statements”) that constitute forward-looking information within the meaning of applicable Canadian securities laws. Forward-looking statements relate to future results or events, are based upon internal plans, intentions, expectations and beliefs, and are subject to risks and uncertainties that may cause actual results or events to differ materially from those indicated or suggested therein. All statements other than statements of current or historical fact constitute forward-looking statements. Forward-looking statements are typically, but not always, identified by words such as “anticipate”, “estimate”, “expect”, “intend”, “forecast”, “continue”, “propose”, “may”, “will”, “should”, “believe”, “plan”, “target”, “objective”, “project”, “potential” and similar or other expressions indicating or suggesting future results or events.

Forward-looking statements are not promises of future outcomes. There is no assurance that the results or events indicated or suggested by the forward-looking statements, or the plans, intentions, expectations or beliefs contained therein or upon which they are based, are correct or will in fact occur or be realized (or if they do, what benefits Pipestone Energy may derive therefrom).

In particular, but without limiting the foregoing, this news release contains forward-looking statements pertaining to: exit guidance; DCE&T expenditures; target debt to LTM EBITDA; production capacity from infrastructure build-out; drilling and completion plans, as applicable, on Pipestone Energy’s 6-24 pad,6-30 pad, and 3-12 pad; timing to bring the 6-24 wells on-stream; production testing and drilling plans on Pipestone Energy’s 9-14 pad; completion plans on Pipestone Energy’s 12-36 pad; tie-in plans for Pipestone Energy’s 11-09 pad; compressor installation plans on Pipestone Energy’s 8-15 compressor; estimates for reducing facility costs for the 6-24 pad; future productivity; estimates of capital spending and cash flow; future estimated budgets; future development; future rig release; forecasted wells drilled, completed and producing in 2020; and estimated development expenditures. With respect to the forward-looking statements contained in this news release, Pipestone Energy has assessed material factors and made assumptions regarding, among other things: future commodity prices and currency exchange rates, including consistency of future oil, natural gas liquids (NGLs) and natural gas prices with current commodity price forecasts; the ability to integrate Blackbird’s and Pipestone Oil’s historical businesses and operations and realize financial, operational and other synergies from the combination transaction completed on January 4, 2019; Pipestone Energy’s continued ability to obtain qualified staff and equipment in a timely and cost-efficient manner; the predictability of future results based on past and current experience; the predictability and consistency of the legislative and regulatory regime governing royalties, taxes, environmental matters and oil and gas operations, both provincially and federally; Pipestone Energy’s ability to successfully market its production of oil, NGLs and natural gas; the timing and success of drilling and completion activities (and the extent to which the results thereof meet expectations); Pipestone Energy’s future production levels and amount of future capital investment, and their consistency with Pipestone Energy’s current development plans and budget; future capital expenditure requirements and the sufficiency thereof to achieve Pipestone Energy’s objectives; the successful application of drilling and completion technology and processes; the applicability of new technologies for recovery and production of Pipestone Energy’s reserves and other resources, and their ability to improve capital and operational efficiencies in the future; the recoverability of Pipestone Energy's reserves and other resources; Pipestone Energy’s ability to economically produce oil and gas from its properties and the timing and cost to do so; the performance of both new and existing wells; future cash flows from production; future sources of funding for Pipestone Energy’s capital program, and its ability to obtain external financing when required and on acceptable terms; future debt levels; geological and engineering estimates in respect of Pipestone Energy’s reserves and other resources; the accuracy of geological and geophysical data and the interpretation thereof; the geography of the areas in which Pipestone Energy conducts exploration and development activities; the timely receipt of required regulatory approvals; the access, economic, regulatory and physical limitations to which Pipestone Energy may be subject from time to time; and the impact of industry competition.

The forward-looking statements contained herein reflect management's current views, but the assessments and assumptions upon which they are based may prove to be incorrect. Although Pipestone Energy believes that its underlying assessments and assumptions are reasonable based on currently available information, undue reliance should not be placed on forward-looking statements, which are inherently uncertain, depend upon the accuracy of such assessments and assumptions, and are subject to known and unknown risks, uncertainties and other factors, both general and specific, many of which are beyond Pipestone Energy’s control, that may cause actual results or events to differ materially from those indicated or suggested in the forward-looking statements. Such risks and uncertainties include, but are not limited to, volatility in market prices and demand for oil, NGLs and natural gas and hedging activities related thereto; the ability to successfully integrate Blackbird’s and Pipestone Oil’s historical businesses and operations; general economic, business and industry conditions; variance of Pipestone Energy’s actual capital costs, operating costs and economic returns from those anticipated; the ability to find, develop or acquire additional reserves and the availability of the capital or financing necessary to do so on satisfactory terms; and risks related to the exploration, development and production of oil and natural gas reserves and resources. Additional risks, uncertainties and other factors are discussed in Blackbird’s management information circular dated November 21, 2018, a copy of which is available electronically on Pipestone Energy’s SEDAR at www.sedar.com.

Certain information in this news release is “financial outlook” within the meaning of applicable securities laws. The purpose of this financial outlook is to provide readers with disclosure of the company’s reasonable expectations of our anticipate results. The financial outlook is provided as of the date of this news release. Readers are cautioned that this financial outlook may not be appropriate for other purposes.

The forward-looking statements contained in this news release are made as of the date hereof and Pipestone Energy assumes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, unless required by applicable securities laws. All forward-looking statements herein are expressly qualified by this advisory

Advisory Regarding Non-GAAP Measures

This news release contains a reference to “Debt to LTM EBITDA” and “Cash Flow”, which are terms commonly used in the oil and natural gas industry but without any standardized meaning or method of calculation prescribed by International Financial Reporting Standards (“IFRS”) or applicable law. Accordingly, Pipestone Energy’s determination of this metric may not be comparable to similar measures presented by other issuers.

Debt to LTM EBITDA

Debt to LTM EBITDA is calculated as net debt to trailing twelve-month EBITDA. EBITDA is calculated as profit or loss before interest, income taxes, depletion, depreciation and amortization, adjusted for certain non-cash and extraordinary items primarily relating to unrealized gains and losses on financial instruments. Debt to LTM EBITDA is considered to be a useful measure in assisting management and investors to evaluate the Company’s financial strength.

Cash Flow

Cash flow is calculated as EBITDA less interest and financing expenses.

Oil and Gas Measures

Basis of Barrel of Oil Equivalent

Petroleum and natural gas reserves and production volumes are stated as a “barrel of oil equivalent” (boe), derived by converting natural gas to oil equivalency in the ratio of 6,000 cubic feet of gas to one barrel of oil. Readers are cautioned that boe figures may be misleading, particularly if used in isolation. A boe conversion ratio of 6,000 cubic feet of gas to one barrel of oil is based on energy equivalency, which is primarily applicable at the burner tip, and does not represent a value equivalency at the wellhead.

DCE&T

This news release contains certain other oil and gas metrics, including DCE&T (drilling, completion, equip and tie-in costs), which does not have a standardized meaning or standard method of calculation and therefore such a measure may not be comparable to similar measures used by other companies and should not be used to make comparisons. This metric has been included herein to provide readers with an additional measure to evaluate the Company's performance; however, this measure is not a reliable indicator of the future performance and future performance may not compare to the performance in previous periods and therefore such a metric should not be unduly relied upon. DCE&T includes all capital spent to drill, complete, equip and tie-in a well.

Initial Production Rates

This news release includes disclosure on initial production (IP) rates for certain wells. These initial production rates are preliminary and not determinative of the rates at which those or any other wells will commence production and thereafter decline. Initial production rates are not necessarily indicative of long-term well or reservoir performance or of ultimate recovery. Although such rates are useful in confirming the presence of hydrocarbons, they are preliminary in nature, are subject to a high degree of predictive uncertainty as a result of limited data availability, and may not be representative of stabilized on-stream production rates.

Production over a longer period will also experience natural decline rates, which can be high in the Montney play and may not be consistent over the longer term with the decline experienced over an initial production period. Initial production may also include recovered “load” fluids used in well completion stimulation operations. Actual results will differ from those realized during an initial production period or short-term test period, and the difference may be material.

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/e9a7a2a0-5231-4876-b76e-13c360d519c2

![]()

2020 Guidance and Development Plan

Refer to map

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.