Ascendant Resources Reports Robust Preliminary Economic Assessment for the Lagoa Salgada Project in Portugal

- Maiden PEA outlines a highly profitable project with low LOM cash costs of $0.44/lb ZnEq and AISC of $0.66/lb ZnEq

- Lagoa Salgada has outlined 10.3MT in M&I Resources at 9.1% ZnEq and 2.5MT in Inferred Resources at 5.9% ZnEq in the North Zone only from 60 holes totaling 13,380 metres of drilling with substantial additional resources expected from future drilling

- The South and Central Zones, with reported Resources delineated by only 20 holes totaling 9,849 meters of drilling, are not included in the current PEA, yet both zones are expected to have a significant benefit to future development

- Lagoa Salgada represents a substantial standalone project that has significant potential for growth, expansion and additional value creation

PEA Highlights (North Zone only):

-

After-tax IRR of 31% and NPV8% of $106M (C$139M @$1.31CAD/USD)

-

Nine-year mine life with production scenario of 2,700 tpd

- Average annual EBITDA of $54.2 million

- Four-year payback period of initial Capex of $162.7 million

- Average operating costs of $49.43/t milled represents low cost production scenario

- Low average annual cash costs of $0.44/lb ZnEq and average annual All-In Sustaining Cost (AISC) of $0.66/lb ZnEq

- Significant upside opportunities remain with near-resource exploration targets identified with multiple deposits open laterally and at depth, and broader targets untested

- Compelling economics at current spot prices

(All dollar amounts are in US Dollars unless otherwise specified, results are reported on a 100% basis)

TORONTO, Jan. 14, 2020 (GLOBE NEWSWIRE) -- Ascendant Resources Inc. (TSX: ASND) (OTCQX: ASDRF; FRA: 2D9) ("Ascendant" or the "Company”) is very pleased to announce exceptional results of its maiden Preliminary Economic Assessment (“PEA”) for the Lagoa Salgada VMS project located on the Iberian Pyrite Belt (“IPB”) in Portugal.

The PEA is based upon the Company’s current Mineral Resource Estimate for the North Zone reported in the recently released National Instrument 43-101 Technical Report with an effective date of September 5, 2019, and demonstrates the potential viability of mining the Measured, Indicated and Inferred Mineral Resources of the North Zone only. It outlines a robust and compelling economic assessment for Lagoa Salgada as it assumes a two-stage underground mining development scenario, with single trackless ramp access, transverse sub-level open stoping method with pastefill. Ventilation and secondary escape ways are planned through raise-bored holes to surface. Milling rates of 2,700 tonnes per day in a standard process circuit is anticipated, with primary crushing, grinding, flotation and leaching of tailings to produce concentrates including lead, zinc, copper and tin, as well as gold and silver doré. There is ample opportunity for extensive expansion from future exploration work to define additional resources to extend the mine life or increase the scale of the outlined operation.

Chris Buncic, President & CEO of Ascendant commented, "We are very pleased that our confidence and investment in the Lagoa Salgada project has been more than justified by the results of this maiden PEA. Over the short period that Ascendant has advanced the Lagoa Salgada project, we have demonstrated a long-life mine with a modest initial capital expenditure and low operating costs while also having a rapid timeline to production. This study outlines a low cost, high-margin operation which the Company intends to improve through continued growth in the size of the Resource and improvement in quality of the mineralization through further exploration work. This study highlights the tremendous intrinsic value created for our shareholders, and our expectation is that there are many further opportunities here to continue building value. We expect this project to increasingly become a major focus and priority for the Company over the coming years.

He continued, “The remaining Mineral Resources in the South and Central Zones, which were out of scope for this PEA, offer near-term growth potential with additional exploration work which we view as lower risk. We have also identified additional targets on the property using geophysical tools that are extremely encouraging and remain untested. We expect the strong correlation between geophysical testing and the subsequent high-grade drilling results experienced in the North Zone to continue into these zones. Follow up drilling is intended to support our objective of identifying additional resources to support future economic studies.”

This maiden PEA provides an initial economic assessment for the Lagoa Salgada project in the North Zone only. The Company intends to expand the current PEA with additional exploration work in the North Zone in 2020. While the North Zone currently demonstrates a robust standalone mining scenario, there remains much room for additional resource growth and a potential operational scale increase, as the deposit remains open along strike and at depth. The Central and South Zones, excluded from the PEA, remain a highly prospective source for future resource growth, as very limited drilling has been performed to date, yet these zones have already achieved a significant resource-to-drilling ratio with the identification of high-grade copper-rich massive sulphide mineralization, warranting further follow-up drilling.

Results from the PEA supports the Company’s investment thesis for acquiring the Lagoa Salgada project as it demonstrates a long-term, economically viable project with the potential to generate significant increased value and is demonstrating the characteristics of a high-quality flagship asset. With historic exploration work indicating low-risk, near-term growth potential, the Company is confident in the ability to improve the economics of this initial PEA through resource growth, optimization and improved recoveries with additional metallurgical work. The Company will perform additional metallurgical testing in parallel with its future exploration and development programs.

PEA Overview

Highlights of the key project metrics are provided in the following table on a 100% basis:

| PEA Key Highlights | |

| Project IRR pre-tax | 37% |

| NPV8% pre-tax | $137 million |

| Project IRR after-tax | 31% |

| NPV8% after-tax | $106 million |

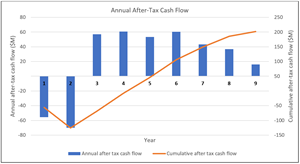

| Life of mine pre-tax cash flow | $ 250 million |

| Life of mine after-tax cash flow | $ 202 million |

| Construction period | 2 years |

| Payback period | 4 years |

| Life of mine | 9 years |

| Average Annual Production | 1.0 million tonnes |

| Initial Capital Expenditure | $ 162.7 million |

| LOM Sustaining Capital Expenditure & Closure | $ 20.2 million |

| Average annual operating costs | $ 49.43 /t milled |

| Average Annual operating costs (C1) | $0.44 /lb ZnEq |

| Average annual All-In Sustaining Costs (AISC) | $0.66 /lb ZnEq |

| Metal Price Assumptions1 | |

| Zinc | $1.20/lb |

| Lead | $1.05/lb |

| Copper | $2.70/lb |

| Silver | $18/oz |

| Gold | $1,400/oz |

| Tin | $7.50/lb |

| Recovery Assumptions | Massive Sulphide |

| Zn | 80% |

| Pb | 65% |

| Cu | 25% |

| Ag | 75% |

| Au | 75% |

| Sn | 30% |

| Recovery Assumptions | Gossan |

| Pb | 65% |

| Sn | 40% |

| Ag | 86% |

| Au | 66% |

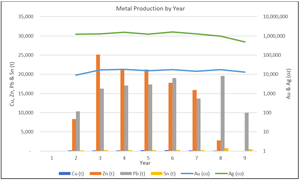

| Average Annual Metal Production | |

| Zn | 12.5kt |

| Pb | 13.7kt |

| Cu | 0.2kt |

| Ag | 1.1Moz |

| Au | 13koz |

| Sn | 0.3kt |

Notes to Table:

1 The project economics have been calculated using consensus prices at the time of the Resource Estimate report in September 2019.

The PEA was prepared by AMC Mining Consultants (Canada) Ltd (AMC) with contributions from Resource Development Inc (RDI) for Mineral Processing and Micon International Limited (Micon), who estimated the Mineral Resources.

The PEA is preliminary in nature, as it includes Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as Mineral Reserves, and there is no certainty that the preliminary economic assessment will be realized.

Mining

The mine design is based on a single decline access from surface at a 12.6% gradient. Decline access is via a 30-meter deep boxcut. Stopes are accessed from level access drives in the north and the south of the deposit. Interlevel spacing varies between 24 meters and 35 meters. All mineralized material and waste development is mined with a 4.5 meter by 4.5 meter end profile. Ore and waste will be hauled to surface using 30 tonne trucks.

The deposit is planned to be mined using transverse sub-level open stoping with pastefill at a production rate of approximately 1 Mtpa. Crosscuts will access the deposit with drives developed laterally across the mineralization. Drives in mineralization will be placed 12.5 meters apart along strike, with stopes approximately 25 meters to 35 meters high, 12.5 meters wide and 25 meters in length. Stope heights in the Gossan tend to be generally less, approximately 20 meters high. A slot will be cut at the end of the mineralization and consecutive rings blasted in a retreating fashion over the full stope length back to the crosscut. Uphole drill rings from the existing drives in the Massive Sulphide will be drilled to extract the mineralization from the overlying Gossan deposit. Ventilation and escape raises will be raise-bored from surface.

The mine life of 9 years is based on a 2,700 tonne per day mining rate. Mine life is based on average head grades of 2.44% Zn, 2.85% Pb, 0.34% Cu, 0.16% Sn, 0.75 g/t Au, 69.8 g/t Ag. Unplanned dilution due to the extraction of the stope was assumed to be 8% for the Gossan zone and 5% for the Massive Sulphide zone. Mining recovery of 90% was assumed for the Gossan and 93% for the Massive Sulphide.

Approximately 55% of tailings (up to 540,000 tpa at a dry bulk density of 1.4) will be placed underground as paste fill to meet an annual demand of 400,000 m3 of void and the remaining tailings placed in the dry stack TSF. The paste plant will have an annual utilisation of just below 50% for the mine the balance being taken up in producing paste for the dry stacked tailings. Paste fill will be transported underground using a combination of pumping and gravity via boreholes and high-pressure pipelines to the stopes.

Metallurgy and Processing

The company has completed initial scoping level metallurgical study with Empresa de Perfuração e Desenvolvimento Mineiro, S.A. (EPDM), Portugal, Grinding Solutions Ltd (GSL), UK, and Wardell Armstrong (WAI), UK in 2019. These non-optimized results indicated that conventional polymetallic process flowsheet is capable of recovering copper, lead, zinc, gold and silver. The flotation tailings will be leached for additional gold and silver values. The oxide ore can be leached to recover precious metals. The leach residue can be sulphidized to recover oxide lead. The final tailing has sufficient tin values and can be recovered by flotation.

The projected recoveries and concentrate grades in the table below are estimated for the project based on extensive experience working with polymetallic ores. Additional testing is planned to confirm the concentrate recoveries and grades.

| Massive Sulphide |

Flotation |

Leached tailings | |||||||

| Zn | Pb | Sn | Cu in Pb conc. | Ag in Pb conc. | Au in Pb conc. | Ag in Zn conc. | Ag | Au | |

| Processing recovery | 80% | 65% | 30% | 25% | 35% | 10% | 20% | 20% | 65% |

| Concentrate grade | 48% | 45% | 10% | 2.5% | |||||

| Gossan | Flotation | Leaching | |||||||

| Pb | Sn | Ag | Au | ||||||

| Processing recovery | 65% | 40% | 66% | 86% | |||||

| Concentrate grade |

60% | 10% | |||||||

Off-site charges include transport of concentrates either to a European smelter or to the port of Lisbon. Additional charges have been considered for lead and tin overseas. Life-of-mine concentrate treatment (including penalties) and transport charges were assumed to be $240/dmt for lead, $270/dmt for zinc and $530/dmt for tin, with standard offtake and refining terms for all metals.

Infrastructure

Lagoa Salgada is situated in southern Portugal about 100km south west of Lisbon, in close proximity to the town of Grândola, and is currently accessed via paved roads to Cilha do Pascoal, followed by 4 km of gravel roads to the mine site. Some improvement to the gravel road to the mine site may be required to accommodate heavy construction traffic.

The site will require an office, changeroom, shop and warehouse as well as storage for fuel, laydown areas, site fencing, and security building. An allowance for a total of 2,600 m2 of building space has been included in the PEA.

Total power requirement for the mine and mill is estimated to be 15 MW. There is ample opportunity to connect to the national grid with both 400 kV and 30 kV transmission lines operating within 7 km of the project site. However, for this study, a conservative allowance has been made to run a 30 kV, 20 MVA transmission line from the existing sub-station at Grândola.

Tailings and waste rock will be disposed of through the use of a dry-stack facility. Total tailings for life of mine are estimated at 7.5 Mt with a further 0.7 Mt of waste rock. Approximately 55% of tailings will be disposed of in the mined-out stopes via the pastefill system. The remaining 4.1 Mt of tailings and waste must be accommodated in the dry stack facility. The base of the facility will be lined, and a low perimeter berm and ditch will capture any precipitation run off during the life of mine. Run off will be collected in a settling pond for use by the mine as service water.

Regional precipitation averages 700 mm per year, and it is anticipated that the site will have a net neutral water balance once the initial dewatering of the mine is complete. All water from the mill will be reused. Total annual water gain through precipitation and mine dewatering is estimated to be approximately 325,000 m3. Loss to the tailings is estimated at 250,000 m3 per year with evaporation accounting for the remaining loss. A complete climate and water balance study is required.

It is anticipated that any make-up water that may be required will be obtained via local wells on site. Should this not be adequate, water can be obtained from the Sado River approximately 5 km from the project site.

A settling pond with capacity of 100,000 m3 will be established to hold precipitation run-off during the rainy season as well as mine and mill water discharge.

AMC has assumed ground water inflow of 5 L/s. Water will be discharged via a staged pump system with pumps located on 3 levels staging to surface.

Operating Costs

The LOM unit operating costs are estimated to be $49.43/t milled. Costs are based on benchmark data from other local operations and local labour costs. Mining is estimated to be $16.84/t milled, Processing $29.17/t milled and General and Administration $3.42/t milled.

| Average LOM Unit Costs | |||||||

| Cost Description |

Operating Costs $/tonne milled |

Operating Costs $/lb ZnEq Payable |

|||||

| Mining | $16.84 | $0.15 | |||||

| Processing | $29.17 | $0.26 | |||||

| Admin (G&A) | $3.42 | $0.03 | |||||

| Total Unit Costs | $49.43/tonne | $0.44/lb ZnEq | |||||

Capital Costs

The total capital cost estimate is $183 million, or $25.23/t milled. Initial Capex of $162.7 million with a four-year payback period and $20.2 million ($3.03/t milled) in sustaining capital.

| Capital Cost Item | Initial | Sustaining | Closure | Total |

| Mining Fleet | 14.20 | 14.20 | ||

| Ramp Box Cut | 1.00 | 1.00 | ||

| Waste Development | 9.85 | 11.61 | 21.46 | |

| Maintenance | 5.50 | 1.25 | 6.75 | |

| Backfill Plant | 12.00 | 12.00 | ||

| Process Plant | 60.00 | 0.60 | 60.60 | |

| Tailings Storage Facility | 12.00 | 0.30 | 12.30 | |

| Infrastructure & Services | 10.62 | 1.46 | 12.08 | |

| Contingency | 37.55 | 37.55 | ||

| Closure | 5.00 | 5.00 | ||

| TOTAL CAPEX | 182.94 |

Project Economics

The project shows robust economic results with a pre-tax NPV at 8% of $137 million and an IRR of 37%, and an after tax NPV at 8% of $106 million and IRR of 31%.

Project economics are based on a 9-year mine life with a 4-year payback period, with positive after-tax cash flow commencing in Year 3.

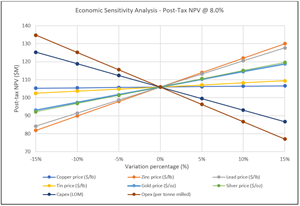

Sensitivities

Project economics are most leveraged to the zinc price yet also highly leveraged to the lead price. A 15% increase to the zinc price results in a post-tax NPV8% increase of 23% to $130 million. Similarly, a 15% increase to the lead price results in a post-tax NPV8% increase of 20% to $127.7 million.

The project economics have been calculated using consensus prices at the time of the Resource Estimate report in September 2019. Based on current spot prices of $1.08/lb Zn, $0.86/lb Pb, $2.78/lb Cu, $18/oz Ag, $1,560/oz Au and $7.68/ln Sn, the project economics remain robust with an After-tax IRR of 24% and NPV8% of $73M (C$96M @$1.31CAD/USD).

Environmental & Permitting

In terms of Environmental Licensing, an Environmental Scoping Proposal (PDA) has already been prepared and submitted to the Environmental authorities for the start of the Environmental Impact Assessment (EIA), in accordance with Portuguese regulations, which has already been approved by the Environmental Impact Assessment Authority (APA).

Mineral Resource Estimate

A summary of the Mineral Resource Estimate is set out in Table 1 below. The PEA was based only upon the Mineral Resource Estimate for the North Zone.

Table 1: Lagoa Salgada Updated Mineral Resource Estimate

North Zone Mineral Resource Estimate - Effective September 5, 2019

| Average Grade | Contained Metal | |||||||||||||||||

| Deposit | Category | Min | Tonnes | Cu | Zn | Pb | Sn | Ag | Au | ZnEq | AuEq | Cut-off | Cu | Zn | Pb | Sn | Ag | Au |

| Zones | (kt) | (%) | (%) | (%) | (%) | (g/t) | (g/t) | (%) | (g/t) | ZnEq% | (kt) | (kt) | (kt) | (kt) | (koz) | (koz) | ||

| North | Measured(M) | GO | 234 | 0.13 | 0.70 | 4.32 | 0.36 | 51 | 1.50 | 11.38 | 7.18 | 2.5 | 0.3 | 1.6 | 10.1 | 0.9 | 385.2 | 11.3 |

| Indicated(I) | GO | 1,462 | 0.08 | 0.43 | 2.55 | 0.26 | 37 | 0.51 | 6.63 | 4.18 | 2.5 | 1.2 | 6.2 | 37.3 | 3.8 | 1,742.1 | 23.8 | |

| M & I | GO | 1,696 | 0.09 | 0.47 | 2.79 | 0.27 | 39 | 0.64 | 7.28 | 4.60 | 2.5 | 1.5 | 7.9 | 47.4 | 4.6 | 2,127.2 | 35.1 | |

| Inferred | GO | 831 | 0.08 | 0.48 | 2.62 | 0.17 | 27 | 0.37 | 5.66 | 3.57 | 2.5 | 0.7 | 4.0 | 21.8 | 1.4 | 727.6 | 9.9 | |

| Measured(M) | MS | 2,444 | 0.40 | 3.12 | 2.97 | 0.15 | 72 | 0.74 | 10.95 | 6.91 | 3.0 | 9.7 | 76.3 | 72.5 | 3.7 | 5,623.9 | 58.4 | |

| Indicated(I) | MS | 5,457 | 0.45 | 2.35 | 2.30 | 0.13 | 75 | 0.67 | 9.55 | 6.03 | 3.0 | 24.5 | 128.1 | 125.6 | 7.3 | 13,221.5 | 116.9 | |

| M & I | MS | 7,902 | 0.43 | 2.59 | 2.51 | 0.14 | 74 | 0.69 | 9.98 | 6.30 | 3.0 | 34.2 | 204.4 | 198.1 | 10.9 | 18,845.5 | 175.2 | |

| Inferred | MS | 1,529 | 0.23 | 1.96 | 1.32 | 0.09 | 45 | 0.49 | 6.36 | 4.01 | 3.0 | 3.6 | 30.0 | 20.2 | 1.4 | 2,219.7 | 24.0 | |

| Measured(M) | Str | 94 | 0.37 | 0.88 | 0.28 | 0.05 | 17 | 0.12 | 3.08 | 1.94 | 2.5 | 0.3 | 0.8 | 0.3 | 0.0 | 51.0 | 0.4 | |

| Indicated(I) | Str | 643 | 0.34 | 0.90 | 0.23 | 0.09 | 17 | 0.06 | 3.23 | 2.04 | 2.5 | 2.2 | 5.8 | 1.5 | 0.6 | 354.0 | 1.3 | |

| M & I | Str | 737 | 0.34 | 0.90 | 0.24 | 0.09 | 17 | 0.07 | 3.21 | 2.03 | 2.5 | 2.5 | 6.6 | 1.7 | 0.6 | 405.0 | 1.7 | |

| Inferred | Str | 142 | 0.24 | 1.12 | 0.39 | 0.04 | 17 | 0.09 | 2.95 | 1.86 | 2.5 | 0.3 | 1.6 | 0.6 | 0.1 | 75.6 | 0.4 | |

| North | M & I | All zones | 10,334 | 0.37 | 2.12 | 2.39 | 0.16 | 64 | 0.64 | 9.06 | 5.72 | 2.9 | 38.2 | 219.0 | 247.2 | 16.2 | 21,377.7 | 212.0 |

| North | Inferred | All zones | 2,502 | 0.18 | 1.42 | 1.70 | 0.12 | 38 | 0.43 | 5.93 | 3.74 | 2.8 | 4.6 | 35.6 | 42.6 | 2.9 | 3,022.8 | 34.3 |

Central and South Zones Mineral Resource Estimate - Effective September 5, 2019

| Average Grade |

Contained Metal |

|||||||||||||||||||

| Deposit | Category | Min | Tonnes | Cu | Zn | Pb | Sn | Ag | Au | CuEq | Cut-off | Cu | Zn | Pb | Sn | Ag | Au | |||

| Zones | (kt) | (%) | (%) | (%) | (%) | (g/t) | (g/t) | (%) | CuEq% | (kt) | (kt) | (kt) | (kt) | (koz) | (koz) | |||||

| Central | Inferred | Str | 1,707 | 0.15 | 0.16 | 0.06 | 0 | 12 | 2.22 | 1.66 | 0.9 | 2.5 | 2.7 | 1.0 | - | 635.2 | 121.9 | |||

| South | Measured(M) | Str/Fr | 0 | — | — | — | — | — | — | — | 0.9 | |||||||||

| Indicated(I) | Str/Fr | 2,473 | 0.47 | 1.53 | 0.83 | 0.00 | 19 | 0.06 | 1.54 | 0.9 | 11.5 | 37.9 | 20.6 | 0.0 | 1,484.7 | 4.7 | ||||

| South | M & I | Str/Fr | 2,473 | 0.47 | 1.53 | 0.83 | 0.00 | 19 | 0.06 | 1.54 | 0.9 | 11.5 | 37.9 | 20.6 | 0.0 | 1,484.7 | 4.7 | |||

| South | Inferred | Str/Fr | 6,085 | 0.40 | 1.34 | 0.80 | 0.00 | 17 | 0.05 | 1.37 | 0.9 | 24.6 | 81.6 | 48.7 | 0.0 | 3,285.2 | 10.0 | |||

Notes to tables:

(1) Mineralized Zones: GO=Gossan, MS=Massive Sulphide, Str=Stringer, Str/Fr=Stockwork

(2) ZnEq% = ((Zn Grade*25.35)+(Pb Grade*23.15)+(Cu Grade*67.24)+(Au Grade*40.19)+(Ag Grade*0.62)+(Sn Grade*191.75))/25.35

(3) CuEq% = ((Zn Grade*25.35)+(Pb Grade*23.15)+(Cu Grade*67.24)+(Au Grade*40.19)+(Ag Grade*0.62))/67.24

(4) AuEq(g/t) = ((Zn Grade*25.35)+(Pb Grade*23.15)+(Cu Grade * 67.24)+(Au Grade*40.19)+(Ag Grade*0.62) )+(Sn Grade * 191.75))/40.19

(5) Metal Prices: Cu $6,724/t, Zn $2,535/t, Pb $2,315/t, Au $1,250/oz, Ag $19.40/oz, Sn $19,175/t

(6) Densities: GO=3.12, MS=4.76, Str=2.88, Str/Fr=2.88

The effective date of this Mineral Resource estimate is September 5, 2019, and it is based on 3 contiguous areas (North, Central and South Zones within the LS West region) of VMS style mineralization defined by 76 diamond drill holes up to August 31, 2019. Leapfrog Geo 4.5.2 software was used to construct three dimensional (“3D”) solid models of massive sulphide, gossan, stringer and stockwork mineralization reflecting a minimum grade of 3% ZnEq, 2.5% ZnEq, 2.5% ZnEq and 0.9% CuEq, respectively and to assign block grades for copper (%), zinc (%), lead (%), tin (%), silver (g/t), gold (g/t) and density (g/cm3) for Measured, Indicated and Inferred Mineral Resources using Ordinary Kriging interpolation methodology and capped 2 m hole assay composites. Two interpolation passes were applied using progressively increasing ellipsoid ranges to cover the range of 3D solid model sizes present. Block size is 5 m across strike (x) by 10 m along strike (y) by 5 m vertically (z). Mineral Resource categorization was applied using geometric criteria, i.e. spacing between drill holes/assay composites.

The Technical Report to disclose the Mineral Resource Estimate was prepared in accordance with National Instrument 43-101 (“NI 43-101”) and the CIM Standards for mineral disclosure by Micon. The Technical Report is available on the Company’s website and SEDAR.

Quality Assurance and Quality Control

Analytical work was carried out by ALS Laboratories. Drill core samples were prepared in the ALS Lab, in Seville, Spain. Pulp samples were then sent to their analytical Laboratory in Ireland for analysis. The core samples are analyzed for gold (ppm) by fire assay (Au‐AA25), and for the other elements by multi element analysis of base metal ores and mill products by optical emission spectrometry using the Varian Vista inductively coupled plasma spectrometer (ME-ICPORE). Samples from the Main Resource, LS_MS_DH ID, are also assayed for Tin (Sn) by ICP-AES after Sodium Peroxide Fusion (Sn-ICP81x).

ALS Laboratories has routine quality control procedures which ensure that every batch of samples includes three sample repeats, two commercial standards and blanks. ALS Laboratories is independent from Ascendant. Ascendant used standard QA/QC procedures when inserting reference standards and blanks for the drilling program.

Technical Disclosure

The reader is advised that the PEA summarized in this press release is intended to provide only an initial, high-level review of the project potential and design options. The PEA mine plan and economic model include numerous assumptions and the use of Inferred Mineral Resources. Inferred Mineral Resources are considered to be too speculative to be used in an economic analysis except as allowed for by Canadian Securities Administrators’ National Instrument 43-101 in PEA studies. There is no guarantee that Inferred Mineral Resources can be converted to Indicated or Measured Mineral Resources, and as such, there is no guarantee the project economics described herein will be achieved.

Ascendant will file with regulatory authorities within 45 days a Technical Report prepared in accordance with NI 43-101 that documents the PEA study and supports the current disclosure.

Qualified Persons

This PEA was prepared for Ascendant Resources Ltd by AMC and other industry consultants, all Qualified Persons (“QP”) under National Instrument 43-101. The scientific and technical information in this press release has been reviewed by the following QPs as described below:

- The Mineral Resource estimate contents of this press release have been reviewed and approved by Charley Murahwi, M.Sc., P.Geo., Pr. Sci. Nat., FAusIMM, Senior Geologist, Micon International Limited.

- The Mining Engineering content of this press release has been reviewed and approved by Gary Methven P.Eng. of AMC Mining Consultants (Canada) Ltd. who is an “Independent Qualified Person” as defined by National Instrument 43-101.

- The Infrastructure content of this press release has been reviewed and approved by George Zazzi P.Eng. of AMC Mining Consultants (Canada) Ltd. who is an “Independent Qualified Person” as defined by National Instrument 43-101.

- The Metallurgical and Process Plant technical contents of this press release have been reviewed and approved by Deepak Malhotra of as President of Pro Solv Consulting who is an “Independent Qualified Person” as defined by National Instrument 43-101.

Review of Technical Information

The scientific and technical information in this press release has been reviewed and approved by Robert Campbell, P.Geo., Vice President, Exploration and Director for Ascendant Resources Ltd, who is a Qualified Persons as defined in National Instrument 43-101.

About Ascendant Resources Inc.

Ascendant is a Toronto-based mining company focused on its 100%-owned producing El Mochito zinc, lead and silver mine in west-central Honduras and its high-grade polymetallic Lagoa Salgada VMS Project located in the prolific Iberian Pyrite Belt in Portugal.

After acquiring the El Mochito mine in December 2016, Ascendant spent 2017 and 2018 implementing a rigorous and successful optimization program restoring the historic potential of El Mochito, a mine in production since 1948, to deliver record levels of production with profitability restored. The Company now remains focused on cost reduction and further operational improvements to drive profitability in 2019 and beyond. With a significant land package of approximately 11,000 hectares in Honduras and an abundance of historical data, there are several near-mine and regional targets providing longer term exploration upside which could lead to further Mineral Resource growth.

Ascendant holds an interest (21.25%) in the high-grade Lagoa Salgada VMS Project and has an earn in opportunity to increase that position to 80%, it is located in the prolific Iberian Pyrite Belt in Portugal. Mineral & Financial Investments Limited, (Redcorp) and Empresa de Desenvolvimento Mineiro, S.A. (EDM) which is a Portuguese Government owned company for the mining sector own the asset. Redcorp holds an 85% interest and EDM holds a 15% interest. Redcorp is a 75% held subsidiary of TH Crestgate, a Swiss investment company and a 25% held subsidiary of Ascendant Resources Inc.

The Company is engaged in exploration of the Project with the goal of expanding the already-substantial defined Mineral Resources and testing additional known targets. The Company’s acquisition of its interest in the Lagoa Salgada Project offers a low-cost entry point to a potentially significant exploration and development opportunity. The Company holds an additional option to increase its interest in the Project upon completion of certain milestones.

Ascendant Resources is engaged in the ongoing evaluation of producing and development stage mineral resource opportunities, on an ongoing basis. The Company's common shares are principally listed on the Toronto Stock Exchange under the symbol "ASND". For more information on Ascendant Resources, please visit our website at www.ascendantresources.com.

Neither the Toronto Stock Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX) accepts responsibility for the adequacy or accuracy of this release.

For further information please contact:

Katherine Pryde

Director, Communications & Investor Relations

Tel: 888-723-7413

info@ascendantresources.com

Cautionary Notes to US Investors

The information concerning the Company’s mineral properties has been prepared in accordance with National Instrument 43-101 (“NI-43-101”) adopted by the Canadian Securities Administrators. In accordance with NI-43-101, the terms “mineral reserves”, “proven mineral reserve”, “probable mineral reserve”, “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are defined in the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) Definition Standards for Mineral Resources and Mineral Reserves adopted by the CIM Council on May 10, 2014. While the terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are recognized and required by NI 43-101, the U.S. Securities Exchange Commission (“SEC”) does not recognize them. The reader is cautioned that, except for that portion of mineral resources classified as mineral reserves, mineral resources do not have demonstrated economic value. Inferred mineral resources have a high degree of uncertainty as to their existence and as to whether they can be economically or legally mined. It cannot be assumed that all or any part of any inferred mineral resource will ever be upgraded to a higher category. Therefore, the reader is cautioned not to assume that all or any part of an inferred mineral resource exists, that it can be economically or legally mined, or that it will ever be upgraded to a higher category. Likewise, you are cautioned not to assume that all or any part of a measured or indicated mineral resource will ever be upgraded into mineral reserves.

Readers should be aware that the Company’s financial statements (and information derived therefrom) have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board and are subject to Canadian auditing and auditor independence standards. IFRS differs in some respects from United States generally accepted accounting principles and thus the Company’s financial statements (and information derived therefrom) may not be comparable to those of United States companies.

Forward Looking Information

This news release contains "forward-looking statements" and "forward-looking information" (collectively, "forward-looking information") within the meaning of applicable Canadian securities legislation. All information contained in this news release, other than statements of current and historical fact, is forward-looking information. Often, but not always, forward-looking information can be identified by the use of words such as "plans", "expects", "budget", "guidance", "scheduled", "estimates", "forecasts", "strategy", "target", "intends", "objective", "goal", "understands", "anticipates" and "believes" (and variations of these or similar words) and statements that certain actions, events or results "may", "could", "would", "should", "might" "occur" or "be achieved" or "will be taken" (and variations of these or similar expressions). Forward-looking information is also identifiable in statements of currently occurring matters which may continue in the future, such as "providing the Company with", "is currently", "allows/allowing for", "will advance" or "continues to" or other statements that may be stated in the present tense with future implications. All of the forward-looking information in this news release is qualified by this cautionary note.

Forward-looking information in this news release includes, but is not limited to, statements regarding the exploration activities and the results of such activities at the Lagoa Salgada Project, the potential to expand mineralization and increase mineral resources and the potential to continue advancing and building value at the Lagoa Salgada Project. Forward-looking information is based on, among other things, opinions, assumptions, estimates and analyses that, while considered reasonable by Ascendant at the date the forward-looking information is provided, inherently are subject to significant risks, uncertainties, contingencies and other factors that may cause actual results and events to be materially different from those expressed or implied by the forward-looking information. The material factors or assumptions that Ascendant identified and were applied by Ascendant in drawing conclusions or making forecasts or projections set out in the forward-looking information include, but are not limited to, the success of the exploration activities at Lagoa Salgada Project, the ability of the exploration results to expand mineralization and increase mineral resources, the ability to continue advancing and building value at the Lagoa Salgada Project and other events that may affect Ascendant's ability to develop its project; and no significant and continuing adverse changes in general economic conditions or conditions in the financial markets.

The risks, uncertainties, contingencies and other factors that may cause actual results to differ materially from those expressed or implied by the forward-looking information may include, but are not limited to, risks generally associated with the mining industry, such as economic factors (including future commodity prices, currency fluctuations, energy prices and general cost escalation), uncertainties related to the development and operation of Ascendant's projects, dependence on key personnel and employee and union relations, risks related to political or social unrest or change, rights and title claims, operational risks and hazards, including unanticipated environmental, industrial and geological events and developments and the inability to insure against all risks, failure of plant, equipment, processes, transportation and other infrastructure to operate as anticipated, compliance with government and environmental regulations, including permitting requirements and anti-bribery legislation, volatile financial markets that may affect Ascendant's ability to obtain additional financing on acceptable terms, the failure to obtain required approvals or clearances from government authorities on a timely basis, uncertainties related to the geology, continuity, grade and estimates of mineral reserves and resources, and the potential for variations in grade and recovery rates, uncertain costs of reclamation activities, tax refunds, hedging transactions, uncertainty related to the results of the Company’s exploration activities at the Lagoa Salgada Project, as well as the risks discussed in Ascendant's most recent Annual Information Form on file with the Canadian provincial securities regulatory authorities and available at www.sedar.com.

Should one or more risk, uncertainty, contingency, or other factor materialize, or should any factor or assumption prove incorrect, actual results could vary materially from those expressed or implied in the forward-looking information. Accordingly, the reader should not place undue reliance on forward-looking information. Ascendant does not assume any obligation to update or revise any forward-looking information after the date of this news release or to explain any material difference between subsequent actual events and any forward-looking information, except as required by applicable law.

Photos accompanying this announcement are available at

https://www.globenewswire.com/NewsRoom/AttachmentNg/735ffee5-f591-4355-ac98-5029e9bfa73a

https://www.globenewswire.com/NewsRoom/AttachmentNg/11378141-1b5f-45b7-8978-7caae768da28

https://www.globenewswire.com/NewsRoom/AttachmentNg/8c75392e-ccae-4655-bd15-5068bd42f689

![]()

Metal Production by Year

Metal Production by Year

Annual After-Tax Cash Flow

Annual After-Tax Cash Flow

Economic Sensitivity Analysis - Post-Tax NPV @ 8.0%

Economic Sensitivity Analysis - Post-Tax NPV @ 8.0%