Restructured Barrick Picks Up Speed as New Executive Teams Get Down to Business

All amounts expressed in U.S. dollars unless otherwise indicated

TORONTO, Feb. 13, 2019 (GLOBE NEWSWIRE) -- Barely six weeks after its merger with Randgold, Barrick (NYSE:GOLD)(TSX:ABX) is making good progress in achieving its short-term priority goals as well as its full year objectives, president and CEO Mark Bristow said here today.

|

||||||||||||||||||||||||||||||||||||||||||||||||||

Bristow, who has already visited most of the group’s operations in the Americas, some of them twice, said one of his first priorities had been to establish regional executive teams for North America, Latin America, and Africa and the Middle East. These are now in place and are already making a significant impact on the way Barrick operates.

He announced that Barrick’s production guidance for 2019 was between 5.1 and 5.6 million ounces of gold and between 375 and 430 million pounds of copper. During 2019, the reserves and resources of newly-acquired Randgold will be combined with Barrick’s on the basis of common calculation criteria, and will be reported on that basis at the end of the year.

Turning to the operations, the higher cost of sales1 guidance for gold in 2019, of $880-$940 per ounce and all-in sustaining costs2 guidance of $870-$920 per ounce, primarily reflects the planned completion of mining at the comparatively high-grade, low-cost Cortez Hills open pit in the first half of the year. Lower costs at Turquoise Ridge, as well as the addition of lower-cost production from Loulo-Gounkoto and Kibali, are expected to partially offset this impact in 2019. Higher grades, improved efficiencies, and tight cost discipline are expected to reverse this trend over the next two to three years.

Bristow said the Nevada assets, including Turquoise Ridge, were now being operated as a single complex, and were already delivering efficiencies. Still in Nevada, the recent Fourmile discovery has now been combined with the nearby Goldrush in a single project which has the potential to become Barrick’s next Tier One3 gold mine. Shaft sinking and construction at Turquoise Ridge is also on track, and along with a focus on improved efficiencies and cost discipline, it too has the potential for Tier One status.

In Argentina, a concerted effort to drive Veladero back to Tier One status is under way as Barrick looks to expand its Latin American business. At Pueblo Viejo in the Dominican Republic, a scoping study and pilot plant support the expansion of what is already one of the world’s largest open pit gold mines. Bristow said there was a renewed focus on exploration across the group’s Latin American portfolio.

The core African assets—the Loulo-Gounkoto complex in Mali, and Kibali in the Democratic Republic of Congo—continue to reinforce their Tier One status, and both are maintaining the grade of their reserves. The feasibility study on the Massawa project in Senegal has been completed, and an application for a mining permit has been submitted to the government.

Bristow said the company was continuing to engage in constructive discussions with the Tanzanian government on the impasse regarding Acacia, and noted that it was in the interest of all stakeholders, including the government, to find a solution to this issue.

On the new business front, Bristow said Nevada was a destination with enormous upside through brownfield extensions, new discoveries, and combination opportunities with other operators in the area. The recently-announced strategic alliance with, and additional investment in, Reunion Gold opens up a new frontier for Barrick in the Guiana Shield. Exploration continues across the group’s global portfolio.

Similarly, work continues on the rationalisation of the group asset portfolio. Bristow said the identification and sale of non-core assets would be based on a carefully-considered and value-based process.

“The new Barrick has a unique ability to grow three-dimensionally: through its large and high-quality exploration portfolio and geological capability; the brownfields extension potential at its existing operations; and new projects destined to become Tier One mines,” Bristow said.

“This growth will be driven and directed by a management team with a mix of skills and experience that few other gold mining companies can match. In the short time that we’ve been together, the combined team has already made great progress in applying Randgold’s proven strategy to a new global group that I am confident will soon earn its place as the industry’s most valued company.”

2019 Operating and Capital Expenditure Guidance

| GOLD PRODUCTION AND COSTS | ||||

| Production (000s ounces) |

Cost of sales1 ($ per ounce) |

Cash costs2 ($ per ounce) |

All-in sustaining costs2 ($ per ounce) |

|

| Barrick Nevada4 | 1,750 - 1,900 | 920 - 970 | 640 - 690 | 850 - 900 |

| Pueblo Viejo (60%) | 550 - 600 | 780 - 830 | 465 - 510 | 610 - 650 |

| Loulo-Gounkoto (80%)5 | 520 - 570 | 800 - 850 | 575 - 625 | 810 - 850 |

| Kibali (45%)5 | 330 - 350 | 890 - 940 | 555 - 605 | 670 - 730 |

| Kalgoorlie (50%) | 280 - 300 | 920 - 970 | 740 - 790 | 920 - 960 |

| Turquoise Ridge (75%) | 270 - 310 | 655 - 705 | 550 - 600 | 680 - 730 |

| Tongon (89.7%)5 | 250 - 270 | 945 - 995 | 710 - 760 | 780 - 820 |

| Porgera (47.5%) | 240 - 260 | 980 – 1,030 | 800 - 850 | 985 - 1,025 |

| Veladero (50%) | 230 - 250 | 1,250 - 1,350 | 770 - 820 | 1,150 - 1,250 |

| Hemlo | 200 - 220 | 890 - 940 | 765 - 815 | 1,100 - 1,200 |

| Acacia (63.9%) | 320 - 350 | 920 - 970 | 665 - 710 | 860 - 920 |

| Other Sites6 | 190 - 250 | 1,075 - 1,165 | 895 - 945 | 1,055 - 1,115 |

| Total Gold5,7,8,9 | 5,100 - 5,600 | 880 - 940 | 650 - 700 | 870 - 920 |

| COPPER PRODUCTION AND COSTS | ||||

| Production (millions of pounds) |

Cost of sales ($ per pound) |

C1 cash costs10 ($ per pound) |

All-in sustaining costs10 ($ per pound) |

|

| Lumwana | 210 - 240 | 2.25 - 2.50 | 1.80 - 2.10 | 2.75 - 3.15 |

| Zaldívar (50%) | 120 - 130 | 2.40 - 2.70 | 1.65 - 1.85 | 2.00 - 2.20 |

| Jabal Sayid (50%) | 45 - 60 | 2.00 - 2.30 | 1.60 - 1.90 | 1.60 - 1.90 |

| Total Copper9 | 375 - 430 | 2.30 - 2.70 | 1.70 - 2.00 | 2.40 - 2.90 |

| CAPITAL EXPENDITURES | ||||

| Mine site sustaining | 1,100 - 1,300 | |||

| Project | 300 - 400 | |||

| Total Attributable Capital Expenditures11 | 1,400 - 1,700 | |||

2019 Outlook Assumptions

| 2019 Guidance Assumption |

Hypothetical Change |

Impact on Revenue (millions) |

Impact on Cost of sales (millions) |

Impact on All-in sustaining Costs2 |

|

| Gold revenue, net of royalties | $1,250/oz | +/- $100/oz | +/- $535 | +/- $17 | +/- $3/oz |

| Copper revenue, net of royalties | $2.75/lb | +/- $0.50/lb | +/- $201 | +/- $18 | +/- $0.04/lb |

Note #1

Cost of sales applicable to gold per ounce is calculated using cost of sales applicable to gold on an attributable basis (removing the non-controlling interest of 40% Pueblo Viejo, 36.1% Acacia, 40% South Arturo, 20% Loulo-Gounkoto and 10.3% of Tongon from cost of sales), divided by attributable gold ounces sold. Cost of sales applicable to copper per pound is calculated using cost of sales applicable to copper including our proportionate share of cost of sales attributable to equity method investments (Zaldívar and Jabal Sayid), divided by consolidated copper pounds sold (including our proportionate share of copper pounds sold from our equity method investments).

Note #2

“Cash costs” per ounce and “All-in sustaining costs” per ounce are non-GAAP financial performance measures. “Cash costs” per ounce starts with cost of sales applicable to gold production, but excludes the impact of depreciation, the non-controlling interest of cost of sales, and includes by-product credits. “All-in sustaining costs” per ounce begin with “Cash costs” per ounce and add further costs which reflect the additional costs of operating a mine, primarily sustaining capital expenditures, general & administrative costs, minesite exploration and evaluation costs, and reclamation cost accretion and amortization. Barrick believes that the use of “cash costs” per ounce and “all-in sustaining costs” per ounce will assist investors, analysts and other stakeholders in understanding the costs associated with producing gold, understanding the economics of gold mining, assessing our operating performance and also our ability to generate free cash flow from current operations and to generate free cash flow on an overall Company basis. “Cash costs” per ounce and “All-in sustaining costs” per ounce are intended to provide additional information only and do not have any standardized meaning under IFRS. Although a standardized definition of all-in sustaining costs was published in 2013 by the World Gold Council (a market development organization for the gold industry comprised of and funded by 26 gold mining companies from around the world, including Barrick), it is not a regulatory organization, and other companies may calculate this measure differently. These measures should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS. Further details on these non-GAAP measures are provided in the MD&A accompanying Barrick’s financial statements filed from time to time on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Note #3

A Tier One Gold Asset is a mine with a stated life in excess of 10 years with 2017 production of at least 500,000 ounces of gold and 2017 total cash cost per ounce within the bottom half of Wood Mackenzie’s cost curve tools (excluding state-owned and privately-owned mines). For purposes of determining Tier One Gold Assets, Total cash cost per ounce is based on data from Wood Mackenzie as of August 31, 2018. The Wood Mackenzie calculation of Total cash cost per ounce may not be identical to the manner in which Barrick calculates comparable measures. Total cash cost per ounce is a non-GAAP financial performance measure with no standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Total cash cost per ounce should not be considered by investors as an alternative to operating profit, net profit attributable to shareholders, or to other IFRS measures. Barrick believes that Total cash cost per ounce is a useful indicator for investors and management of a mining company’s performance as it provides an indication of a company’s profitability and efficiency, the trends in cash costs as the company’s operations mature, and a benchmark of performance to allow for comparison against other companies. Wood Mackenzie is an independent third party research and consultancy firm that provides data for, among others, the metals and mining industry. Wood Mackenzie does not have any affiliation to Barrick.

Note #4

Reflects production and sales from Goldstrike, Cortez, and South Arturo on a 60% basis, which reflects our equity share.

Note #5

2019 forecast cost of sales does not include the impact of the Randgold purchase price allocation.

Note #6

Includes Lagunas Norte, Golden Sunlight and Morila on a 40% basis.

Note #7

Operating unit guidance ranges reflect expectations at each individual operating unit, and may not add up to the corporate-wide guidance range total. Guidance ranges exclude Pierina, which is mining incidental ounces as it enters closure.

Note #8

Total gold cash costs and all-in sustaining costs per ounce include the impact of hedges and/or costs allocated to non-operating sites.

Note #9

Includes corporate administration costs.

Note #10

“C1 cash costs” per pound and “All-in sustaining costs” per pound are non-GAAP financial performance measures. “C1 cash costs” per pound is based on cost of sales but excludes the impact of depreciation and royalties and includes treatment and refinement charges. “All-in sustaining costs” per pound begins with “C1 cash costs” per pound and adds further costs which reflect the additional costs of operating a mine, primarily sustaining capital expenditures, general & administrative costs and royalties. Barrick believes that the use of “C1 cash costs” per pound and “all-in sustaining costs” per pound will assist investors, analysts, and other stakeholders in understanding the costs associated with producing copper, understanding the economics of copper mining, assessing our operating performance, and also our ability to generate free cash flow from current operations and to generate free cash flow on an overall Company basis. “C1 cash costs” per pound and “All-in sustaining costs” per pound are intended to provide additional information only, do not have any standardized meaning under IFRS, and may not be comparable to similar measures of performance presented by other companies. These measures should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Further details on these non-GAAP measures are provided in the MD&A accompanying Barrick’s financial statements filed from time to time on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Note #11

These amounts include our 60% share of Pueblo Viejo and South Arturo, our 80% share of Loulo-Gounkoto, our 89.7% share of Tongon, our 63.9% share of Acacia and our 50% share of Zaldívar and Jabal Sayid.

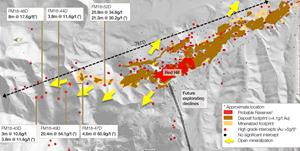

GOLDRUSH AND FOURMILE PROJECTS COMBINED WITH POTENTIAL FOR TIER ONE STATUS

Ongoing exploration within the Horse Canyon/Cortez Unified Exploration Plan in Nevada has identified and extended ore grade mineralization such that the Goldrush and Fourmile resource areas are coalescing on the same geological trend. The two are now being treated as one project which has increased the optionality for this project and the potential to become another Tier One mine for Barrick within the footprint of the Cortez district.

While the geological, geotechnical and geo-metallurgical aspects of the mineralized corridor are being reviewed, ongoing development of the twin exploration declines at Goldrush will provide access to the heart of the orebody for further drilling and the conversion of resources to reserves. The exploration declines can be converted to production declines later.

Rod Quick, Barrick’s mineral resource management and evaluation executive, confirmed that the project’s feasibility study is currently scheduled for completion in early 2020, although the latest developments have afforded the feasibility team the opportunity to re-evaluate and optimize the project design, on the back of the increased resources. Current indicated mineral resources outside of reserves stand at 30.9Mt at 9.4g/t for 9.35 million ounces and a further 11.9Mt at 9.3g/t for 3.55 million ounces in the inferred category4. Current probable reserves on the Redhill portion of project stand at 6.4Mt at 9.7g/t for 2.0 million ounces4.

Rob Krcmarov, executive vice-president exploration and growth, says the project has demonstrated the enormous potential of the Cortez region, which has historically produced more than 24 million ounces, and has 10.7 million ounces of reserves and 12.5 million ounces of M&I resources and a significant mineral inventory yet to be defined4. Barrick believes it could deliver further discoveries of a similar size to Goldrush, and therefore while continuing to explore the area, the company is also evaluating increasing processing capacity in the region.

Goldrush-Fourmile: Our Next Potential Tier One Mine1

- Delivered initial inferred resource of 1.167Mt @ 18.58 g/t at Fourmile within significantly mineralized footprint

- Open mineralization

- Integrating latest discovery with Goldrush2

- See Appendix A for additional details including assay results for the significant intercepts.

- Probable reserves: 2 Moz (6.4Mt at 9.7 g/t); indicated resources: 9.35Moz (30.9 Mt @ 9.4g/t); inferred resources (including Fourmile): 3.55Moz (11.9Mt @ 9.3g/t).

Appendix A – Fourmile Significant Intercepts1

Drill Results Highlighted in Q4 2018 Presentation

| Core Drill Hole2 | Azimuth | Dip | Interval (m) | Width (m)3 | Au (g/t) |

| FM18-43D | 14 | -87 | 909.5 - 910.7 | 1.2 | 5.0 |

| 916.8 - 918.3 | 1.5 | 5.4 | |||

| 932.4 - 935.4 | 3.0 | 10.6 | |||

| 957.7 - 960.7 | 3 | 18.8 | |||

| FM18-44D | 92 | -86 | 1,079.3 - 1,083.1 | 3.8 | 11.6 |

| FM18-47D | 151 | -83 | 627.3 - 628.8 | 1.5 | 5.9 |

| 772 - 776.6 | 4.6 | 60.9 | |||

| 779.5 - 781.3 | 1.8 | 11.7 | |||

| FM18-48D | 119 | -83 | 1,102.8 - 1,105.8 | 3 | 17.6 |

| FM18-49D | 84 | -86 | 921.1 - 922 | 0.91 | 16.8 |

| 957.7 - 978.1 | 20.4 | 54.1 | |||

| FM18-52D | 62 | -83 | 873.1 - 899 | 25.9 | 34.6 |

| 935.6 - 956.9 | 21.3 | 30.2 |

- All intercepts calculated using a 5g/t Au cutoff and are uncapped; minimum intercept width is 0.8m; internal dilution is less than 20% total width.

- Fourmile drill hole nomenclature: FM (Fourmile) followed by the year (18 for 2018).

- True width of intercepts are uncertain at this stage.

The drilling results for the Fourmile property contained in this press release have been prepared in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects. All drill hole assay information has been manually reviewed and approved by staff geologists and re-checked by the project manager. Sample preparation and analyses are conducted by an independent laboratory. Procedures are employed to ensure security of samples during their delivery from the drill rig to the laboratory. The quality assurance procedures, data verification and assay protocols used in connection with drilling and sampling on the Fourmile property conform to industry accepted quality control methods.

SOLAR HYBRID PLANT FOR LOULO-GOUNKOTO

As part of its cost-reduction program and drive to manage its carbon footprint, Loulo is to install a 24MW off-grid solar hybrid plant to support its existing 63MW thermal power station, by harnessing Mali’s abundant solar resource.

This renewable energy project is part of Barrick’s strategy of moving away from thermal power in Africa, where lack of infrastructure means that many mines need to rely on self-generated diesel energy, making this their largest cost item.

Utilizing hydropower in the Democratic Republic of Congo, grid power in Côte d’Ivoire, and heavy-fuel baseload generators in Mali, Barrick has already cut its energy costs significantly, and the continuing roll-out of renewable energy sources will ensure that its future needs are met in the most cost-efficient and environmentally friendly manner.

The solar feasibility study forecasts that the photovoltaic plant will replace 50,000MWh/y of thermal generation, saving 10 million liters of fuel per year and reducing CO² emissions by 42,000 tonnes over the same period. The introduction of the solar component will cut the complex’s energy cost by around 2 cents/kWh.

Construction of the project—which meets Barrick’s investment criteria of 20% IRR—will start later this year, and it is scheduled for commissioning in late 2020. The plant will use the latest weather prediction models, which will enable the power management system to switch between thermal and solar without compromising the micro-grid.

AUTOMATION DRIVES MINING INTO THE FUTURE

Autonomous production systems and projects throughout Barrick are being advanced as the group focuses on becoming the global leader in mining efficiency.

Chief executive Mark Bristow says to achieve its goal of being the world’s most valued gold company, in a rapidly evolving environment where the industry’s shift to developing countries will continue, Barrick will have to be at the leading edge of automation.

“Kibali in the Democratic Republic of Congo is currently at the forefront, with its mission control system which manages the underground ore handling logistics without human intervention from the surface, but across Barrick there are many automated operations and developments which are now being unified in a group strategy,” he says.

These include underground drills that can be run from surface during shift changes; automated underground and open pit haulage trucks; fully autonomous backfill systems; remote-controlled open pit drills; and autonomous drilling of development and production blast holes by multiple units controlled by a single remote operator.

Glenn Heard, senior vice president mining, says ongoing projects currently cover five main areas: underground development and production drilling, production and haulage, and open pit haulage and production.

“At present all our systems have barriers which prevent human access to the autonomous operating zones. Our next big step will be to create a situation where autonomous and manned units can work together seamlessly within the same active areas, and we’re working with Sandvik and other providers to achieve this,” he says.

LUMWANA SEEKS LONG-TERM PARTNERSHIP WITH ZAMBIAN GOVERNMENT

Barrick, owners of the Lumwana copper mine, says it is continuing to engage with the Zambian government and community stakeholders about a mutually-beneficial way forward for the operation.

Subsequent to the first Lumwana board meeting following the Barrick/Randgold merger, Barrick’s chief operating officer for Africa and the Middle East, Willem Jacobs, said the company was mindful that the Government was under pressure to increase its revenue. At the same time, however, its proposed tax changes would put Lumwana in a challenging situation.

“The proposed changes to taxes and royalties would imperil the mine’s ability to sustain returns to all stakeholders, such as the significant contribution of more than $3.3 billion it has already made to the Zambian economy over the past 10 years,” Jacobs said.

“Lumwana has made detailed proposals to the Government about a partnership approach which would provide the State with an improved share in the economics of Lumwana without overburdening the mine. Finding a win-win solution between the industry and Government would without doubt increase investor confidence in Zambia and safeguard the long-term prospects of its mining industry.”

Jacobs said media reports that Barrick had sold Lumwana were untrue, but given the challenging conditions the mine was facing, all options would have to be considered.

WILLOW CREEK TO REOPEN TO THE PUBLIC

The Willow Creek Reservoir Restoration Project, designed to create a natural spawning habitat for fish and to provide a recreational resource for the surrounding communities, is nearing completion and will reopen to the public early this year.

The Barrick-owned reservoir was built in the 1920s but drained in December 2017 as a result of a gate malfunction. Since then, the company has invested $1.7 million and 20,000 man-hours in restoring the man-made lake. Among other things, Barrick volunteers have helped to install the proper fish habitats. Nevada Bighorns Unlimited, a sportsmen’s group and Barrick partner, will fund the fish restocking in the North American spring this year. While the fishery will take a while to return to its original level, the public will, at the same time, be given access to the reservoir.

Barrick and the Nevada Department of Wildlife (NDOW) have formed a partnership to manage the maintenance of the reservoir and the restoration of fish stocks and habitats.

“Barrick has a record of responsible water management and this agreement again demonstrates its desire to be a good corporate citizen,” says Caleb McAdoo, Eastern Region habitat supervisor for the NDOW. “The reservoir is important to Nevadans and our agreement will ensure its longevity and optimal use.”

BRISTOW HITS GROUND RUNNING IN AMERICAS

A fortnight after the merger between Barrick and Randgold was completed, new president and CEO Mark Bristow and members of the combined executive team set out on a tour of the North- and Latin-American operations to accelerate the process of integration.

In Latin America they visited Pueblo Viejo and Veladero twice, and Lagunas Norte and Pierina each once. Bristow also met Governor Sergio Uñac of San Juan province to stress Barrick’s commitment to Argentina and the importance of a mutually-beneficial partnership with government.

The North American leg of the tour took in Hemlo, Cortez, Goldstrike, and Turquoise Ridge. Catherine Raw, COO North America notes: “Visiting these sites in January meant we had to deal with harsh weather conditions—particularly at Hemlo, where temperatures reached -40 degrees Celsius, before windchill!”

In his meetings with employees, Bristow reviewed 2018 performances and 2019 budgets, and spelled out what Barrick would have to do to achieve its new goal of becoming the world’s most valued gold company. He explained that the rationalization of the business was not merely a rightsizing exercise, but designed to ensure that the company was truly “fit for purpose”. Senior executives have been embedded across the operations to facilitate decision-making at source, and people were being aligned with each other and with corporate goals.

Colin Bower, the new EGM of the expanded Barrick Nevada, which includes Cortez, Goldstrike, and Turquoise Ridge, noted: “The pragmatism of Bristow’s approach to the business coupled with the direct communication was much appreciated. The Nevada team finished the visit with clarity of purpose, direction, and clear expectations of our contribution going forward.”

KIBALI BREAKS RECORDS ACROSS BOARD, ALL KEY PRODUCTION PARAMETERS ABOVE PLAN

The Kibali gold mine produced 807,2515 ounces of gold in 2018, above its target of 750,000 ounces and 35% higher than its output the previous year. This was achieved on the back of the successful ramp-up in underground production and a steady improvement in the processing plant recovery and throughput.

Barrick president and chief executive Mark Bristow told a media briefing in Kinshasa that the record production was driven by the shaft operating at nameplate specification and the optimization of the underground materials handling system which has placed Kibali at the leading edge of gold mine automation in Africa.

Despite the high activity level, the mine recorded its safest year to date, with no lost-time injuries in the fourth quarter and no significant environmental incident. Bristow said the mine continued to offset the impact of its operations through environmental projects such as the 10,130 indigenous trees planted on the site last year, as well as biodiversity initiatives. On the health front, the malaria and HIV prevalence rates continued to decrease and stood at 12.9% and 2.8% respectively at the year end.

The resettlement of 1,478 families from the Gorumbwa site to a new village has been successfully completed and will allow the development of the next satellite pit in the mine plan. In addition, continuing brownfields exploration around the mine has identified numerous opportunities for reserve replacement along the KZ trend and around KCD.

Bristow noted that Kibali’s partnership philosophy was continuing to deliver dividends to the local economy, with $39 million paid to Congolese contractors in the last quarter of 2018 alone.

“Our commitment to the DRC, made 10 years ago when Randgold started developing Kibali, has not dimmed, and under the new banner of Barrick we expect to continue to make a significant and growing contribution to the country’s economy and to unlock further value for all our stakeholders,” he said.

TONGON ACHIEVES REVISED GUIDANCE AFTER OVERCOMING MAJOR CHALLENGES

After nine months of intermittent production caused by illegal strikes and social unrest, the Tongon gold mine returned to normal in the last quarter of 2018 and achieved its revised production target of 230,000 ounces for the year.

Speaking at a media briefing in Abidjan, Barrick president and chief executive Mark Bristow said the Government-endorsed reconciliation agreement between the mine, the employees and the community was designed to create a climate in which operations would run as normal and good relations could be rebuilt.

“This should mark a new beginning for Tongon, and it is significant that the Minister of Mines, Jean Claude Kouassi, visited the mine to sign this agreement in the presence of representatives of all the stakeholders,” he said.

Bristow said Barrick was committed to continuing the Randgold policy of investment in community projects and noted that despite the many challenges it had faced, Tongon had to date spent some $10 million on these initiatives. All eight villages in the mine’s ambit now have primary schools, medical care facilities and potable water, and the development of an agribusiness as a sustainable source of economic activity after the mine’s closure is progressing.

During the year, the mine’s grid power supply was frequently interrupted by the roll-out of the power utility’s new ring circuit, which also impacted production. Bristow said that the situation was much improved after the commissioning of the new circuit and Tongon was looking forward to a more stable supply as well as a more constructive engagement with the utility.

“It’s worth noting that despite its troubled history, Tongon has remained profitable and has continued to pay dividends to its shareholders, including the Government,” Bristow said.

“We are committed to prolong the contribution it makes to the economy and the community by extending the mine’s life. Exploration for additional reserves is continuing around the mine and indications are that this aim is achievable. We are also maintaining our search for new world-class gold deposits in our permit portfolio elsewhere in Côte d’Ivoire.”

LOULO-GOUNKOTO COMPLEX CONTINUES TO INVEST IN ITS FUTURE AND POINTS TO ONGOING IMPROVEMENT IN PRODUCTION

The Loulo-Gounkoto complex in Mali posted a fourth consecutive quarterly improvement in gold production, despite an illegal work stoppage that caused it to miss its full year production guidance of 690,000 ounces by 4%. In addition to this, 2018 was a record throughput year of more than 5 million tonnes at close to the complex’s reserve grade.

Speaking at a briefing at the mine for local media, Barrick president and chief executive Mark Bristow noted that the complex, which ranks among the recently merged Barrick/Randgold group’s Tier One assets, was continuing to invest in its future by exploring for additional reserves and upgrading plant and equipment.

“A preliminary economic assessment of the Loulo 3 open pit and underground project has been completed and drilling continues to expand the area of high-grade mineralization south of the Yalea orebody. Exploration of the Faraba structure on the Gounkoto permit has shown the potential for multiple zones of mineralization to be extended,” Bristow said.

“At the existing operations, we’ve commissioned the second crusher at Yalea, the full integration of the automated dispatch system at Gounkoto and the second radar for the geotechnical monitoring of the Gounkoto pit. The complex has also completed the striker belts project at Gara and moved ahead with the expansion of the tailings treatment facility.”

Bristow said the continuing profitable growth of Loulo-Gounkoto was a shining example of what could be achieved through a genuine partnership between investors, managers and governments. He cited the tax holiday recently granted for the development of the super pit at Gounkoto as a typical instance of mutually beneficial cooperation.

“As Randgold, we’ve been engaged in Mali for 25 years and have worked together productively with successive governments. We look forward to continuing this relationship as Barrick with the recently elected government and the new minister of mines. Our differences over the tax issue remain on the agenda and we trust that through amicable mediation we’ll arrive at a solution acceptable to both parties,” he said.

Bristow noted that the complex continued to improve its safety and environmental management, and had obtained the new version of the ISO 14001 environmental certification while retaining its OHSAS 18001 health and safety rating.

The group was also maintaining its support for community development programs and projects. At its other Malian asset, Morila, the government has formally endorsed its plan to establish an agribusiness designed to mitigate the social and economic impact of the operations closure.

ENQUIRIES

President and CEO

Mark Bristow

+1 647 205 7694

+44 788 071 1386

Senior Executive Vice-President and Chief Financial Officer

Graham Shuttleworth

+44 1534 735 333

+44 779 771 1338

Investor and Media Relations

Kathy du Plessis

+44 20 7557 7738

Email: barrick@dpapr.com

TECHNICAL INFORMATION

The scientific and technical information contained in this press release has been reviewed and approved by: Rodney Quick, mineral resource management and evaluation executive of Barrick; Simon Bottoms, mineral resources manager: Africa and Middle East of Barrick; Rick Sims, Registered Member SME, vice president, reserves and resources of Barrick; and Robert Krcmarov ,FAusIMM, executive vice president, exploration and growth of Barrick—each a “Qualified Person” as defined in National Instrument 43-101 - Standards of Disclosure for Mineral Projects.

ENDNOTES

Endnote 1

Cost of sales applicable to gold per ounce is calculated using cost of sales related to gold on an attributable basis (removing the non-controlling interest of 40% Pueblo Viejo, 36.1% Acacia, 40% South Arturo, 20% Loulo-Gounkoto and 10.3% of Tongon from cost of sales), divided by attributable gold ounces sold. Cost of sales applicable to copper per pound is calculated using cost of sales applicable to copper including our proportionate share of cost of sales attributable to equity method investments (Zaldívar and Jabal Sayid), divided by consolidated copper pounds sold (including our proportionate share of copper pounds sold from our equity method investments).

Endnote 2

“Cash costs” per ounce and “All-in sustaining costs” per ounce are non-GAAP financial performance measures. “Cash costs” per ounce starts with cost of sales applicable to gold production, but excludes the impact of depreciation, the non-controlling interest of cost of sales, and includes by-product credits. “All-in sustaining costs” per ounce begin with “Cash costs” per ounce and add further costs which reflect the additional costs of operating a mine, primarily sustaining capital expenditures, general & administrative costs, minesite exploration and evaluation costs, and reclamation cost accretion and amortization. Barrick believes that the use of “cash costs” per ounce and “all-in sustaining costs” per ounce will assist investors, analysts and other stakeholders in understanding the costs associated with producing gold, understanding the economics of gold mining, assessing our operating performance and also our ability to generate free cash flow from current operations and to generate free cash flow on an overall Company basis. “Cash costs” per ounce and “All-in sustaining costs” per ounce are intended to provide additional information only and do not have any standardized meaning under IFRS. Although a standardized definition of all-in sustaining costs was published in 2013 by the World Gold Council (a market development organization for the gold industry comprised of and funded by 26 gold mining companies from around the world, including Barrick), it is not a regulatory organization, and other companies may calculate this measure differently. These measures should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS. Further details on these non-GAAP measures are provided in the MD&A accompanying Barrick’s financial statements filed from time to time on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Endnote 3

A Tier One gold asset is a mine with a stated life in excess of 10 years with 2017 production of at least 500,000 ounces of gold and 2017 total cash cost per ounce within the bottom half of Wood Mackenzie’s cost curve tools (excluding state-owned and privately-owned mines). For purposes of determining Tier One gold assets, “Total cash cost” per ounce is based on data from Wood Mackenzie as of August 31, 2018. The Wood Mackenzie calculation of “Total cash cost” per ounce may not be identical to the manner in which Barrick calculates comparable measures. “Total cash cost” per ounce is a non-GAAP financial performance measure with no standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. “Total cash cost” per ounce should not be considered by investors as an alternative to operating profit, net profit attributable to shareholders, or to other IFRS measures. Wood Mackenzie is an independent third party research and consultancy firm that provides data for, among others, the metals and mining industry. Wood Mackenzie does not have any affiliation to Barrick.

Endnote 4

Estimated in accordance with National Instrument 43-101 as required by Canadian securities regulatory authorities. Estimates are as of December 31, 2018, unless otherwise noted. Includes Cortez proven reserves of 17.6 million tonnes grading 2.01g/t, representing 1.1 million ounces of gold and probable reserves of 127 million tonnes grading 1.86g/t representing 7.6 million ounces of gold; Cortez measured resources of 3.3 million tonnes grading 1.84g/t, representing 198,000 ounces of gold and indicated resources of 53 million tonnes grading 1.73g/t, representing 3.0 million ounces of gold; Goldrush probable reserves of 6 million tonnes grading 9.69g/t, representing 2.0 million ounces of gold; Goldrush indicated resources of 30.9 million tonnes grading 9.40g/t, representing 9.35 million ounces of gold. Goldrush inferred resources of 11.9 million tonnes grading 9.3g/t, representing 3.55 million ounces of gold.

Endnote 5

100% basis. In 2018, Randgold’s 45% equity share of gold production from Kibali was 363,000 ounces.

CAUTIONARY STATEMENT ON FORWARD-LOOKING INFORMATION

Certain information contained or incorporated by reference in this press release, including any information as to our strategy, projects, plans, or future financial or operating performance, constitutes “forward-looking statements”. All statements, other than statements of historical fact, are forward-looking statements. The words “believe”, “expect”, “anticipate”, “plan”, “assume”, “intend”, “project”, “continue”, “budget”, “estimate”, “potential”, “may”, “will”, “can”, “should”, “could”, “would”, and similar expressions identify forward-looking statements. In particular, this press release contains forward-looking statements including, without limitation, with respect to: Barrick’s forward-looking production guidance; estimates of future cost of sales per ounce for gold and per pound for copper, all-in-sustaining costs per ounce/pound, cash costs per ounce, and C1 cash costs per pound; projected capital, operating, and exploration expenditures; targeted debt and cost reductions, including cost reductions resulting from the installation of a solar hybrid plant at Loulo-Gounkoto; mine life and production rates; potential mineralization, including with respect to Cortez, Goldrush, Fourmile, Turquoise Ridge and Loulo-Gounkoto, and metal or mineral recoveries; the benefits of integrating the Goldrush and Fourmile operations as a single project, and completion of the project’s feasibility study; the development of potential Tier One gold assets to become Tier One gold assets; our pipeline of high confidence projects at or near existing operations; the potential to identify new reserves and resources, and our ability to convert resources into reserves, including our pipeline of greenfield projects; the combined Company’s future plans, growth potential, financial strength, investments and overall strategy; completion of mining at Cortez Hills open pit; opening and fish restocking of Willow Creek Reservoir Restoration Project; opportunities for reserve replacement along the KZ trend and around KCD; future contributions to the economy of the Democratic Republic of Congo; future investments in community projects, permitting strategy and the availability of power to the Tongon mine; potential mediation with the government of Mali with respect to tax issues and the outcome of any such mediation; expectations regarding the potential impact of the proposed tax changes in Zambia; the potential benefits resulting from a long-term partnership between Lumwana and the Zambian Government; asset sales, joint ventures, and partnerships; and expectations regarding future price assumptions, financial performance, and other outlook or guidance.

Forward-looking statements are necessarily based upon a number of estimates and assumptions including material estimates and assumptions related to the factors set forth below that, while considered reasonable by the Company as at the date of this press release in light of management’s experience and perception of current conditions and expected developments, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements, and undue reliance should not be placed on such statements and information. Such factors include, but are not limited to: fluctuations in the spot and forward price of gold, copper, or certain other commodities (such as silver, diesel fuel, natural gas, and electricity); the speculative nature of mineral exploration and development; changes in mineral production performance, exploitation, and exploration successes; risks associated with the fact that certain Best-in-Class initiatives are still in the early stages of evaluation, and additional engineering and other analysis is required to fully assess their impact; risks associated with the ongoing implementation of Barrick’s digital transformation initiative, and the ability of the projects under this initiative to meet the Company’s capital allocation objectives; the duration of the Tanzanian ban on mineral concentrate exports; the ultimate terms of any definitive agreement between Acacia and the Government of Tanzania to resolve a dispute relating to the imposition of the concentrate export ban and allegations by the Government of Tanzania that Acacia under-declared the metal content of concentrate exports from Tanzania; the status of certain tax re-assessments by the Tanzanian government; the manner in which amendments to the 2010 Mining Act (Tanzania) increasing the royalty rate applicable to metallic minerals such as gold, copper and silver to 6% (from 4%), the new Finance Act (Tanzania) imposing a 1% clearing fee on the value of all minerals exported from Tanzania from July 1, 2017 and the new Mining Regulations announced by Government of Tanzania in January 2018 will be implemented and the impact of these and other legislative changes on Acacia; whether Barrick will successfully negotiate an agreement with respect to the dispute between Acacia and the Government of Tanzania and whether Acacia will approve the terms of any such final agreement; the benefits expected from recent transactions being realized, including the Randgold merger; diminishing quantities or grades of reserves; increased costs, delays, suspensions and technical challenges associated with the construction of capital projects; operating or technical difficulties in connection with mining or development activities, including geotechnical challenges and disruptions in the maintenance or provision of required infrastructure and information technology systems; failure to comply with environmental and health and safety laws and regulations; timing of receipt of, or failure to comply with, necessary permits and approvals; uncertainty whether some or all of the Best-in-Class initiatives, targeted investments and projects will meet the Company’s capital allocation objectives and internal hurdle rate; the impact of global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future cash flows; adverse changes in our credit ratings; the impact of inflation; fluctuations in the currency markets; changes in U.S. dollar interest rates; risks arising from holding derivative instruments; changes in national and local government legislation, taxation, controls or regulations and/ or changes in the administration of laws, policies and practices, expropriation or nationalization of property and political or economic developments in Canada, the United States, and other jurisdictions in which the Company or its affiliates do or may carry on business in the future; lack of certainty with respect to foreign legal systems, corruption and other factors that are inconsistent with the rule of law; damage to the Company’s reputation due to the actual or perceived occurrence of any number of events, including negative publicity with respect to the Company’s handling of environmental matters or dealings with community groups, whether true or not; the possibility that future exploration results will not be consistent with the Company’s expectations; risks that exploration data may be incomplete and considerable additional work may be required to complete further evaluation, including but not limited to drilling, engineering and socioeconomic studies and investment; risk of loss due to acts of war, terrorism, sabotage and civil disturbances; litigation and legal and administrative proceedings; contests over title to properties, particularly title to undeveloped properties, or over access to water, power and other required infrastructure; business opportunities that may be presented to, or pursued by, the Company; risks associated with the fact that certain of the initiatives described in this press release are still in the early stages and may not materialize; our ability to successfully integrate acquisitions or complete divestitures; risks associated with working with partners in jointly controlled assets; employee relations including loss of key employees; increased costs and physical risks, including extreme weather events and resource shortages, related to climate change; availability and increased costs associated with mining inputs and labor; and the organization of our previously held African gold operations and properties under a separate listed Company. In addition, there are risks and hazards associated with the business of mineral exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and gold bullion, copper cathode or gold or copper concentrate losses (and the risk of inadequate insurance, or inability to obtain insurance, to cover these risks).

Many of these uncertainties and contingencies can affect our actual results and could cause actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, us. Readers are cautioned that forward-looking statements are not guarantees of future performance. All of the forward-looking statements made in this press release are qualified by these cautionary statements. Specific reference is made to the most recent Form 40- F/Annual Information Form on file with the SEC and Canadian provincial securities regulatory authorities for a more detailed discussion of some of the factors underlying forward-looking statements and the risks that may affect Barrick’s ability to achieve the expectations set forth in the forward-looking statements contained in this press release.

The Company disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by applicable law.

Photos accompanying this announcement are available at

http://www.globenewswire.com/NewsRoom/AttachmentNg/83cb132f-4ce6-42a7-a668-9ee79b35d59f

http://www.globenewswire.com/NewsRoom/AttachmentNg/e1f4ec57-2607-45a6-81fa-992b92be78e5

http://www.globenewswire.com/NewsRoom/AttachmentNg/ef5b06a5-068c-46a5-a788-be288865136f

http://www.globenewswire.com/NewsRoom/AttachmentNg/c7772245-c1fd-488e-b831-f7b5202fdbd2

http://www.globenewswire.com/NewsRoom/AttachmentNg/8792f173-ecaa-4da4-abe0-e6a3fd971176

http://www.globenewswire.com/NewsRoom/AttachmentNg/9f322f38-c850-4488-9737-87172d3c674d

http://www.globenewswire.com/NewsRoom/AttachmentNg/52a1f629-4a18-4cd9-a9d1-193305235887

http://www.globenewswire.com/NewsRoom/AttachmentNg/a402e265-b1bb-465c-bb06-cd6060e09895

http://www.globenewswire.com/NewsRoom/AttachmentNg/ed9d280c-7c41-430f-a3cd-e048847d206d

http://www.globenewswire.com/NewsRoom/AttachmentNg/9f12016f-7fb8-4c5c-b614-39ddd78635a3

![]()