Critical Elements Announces Positive Feasibility Study with a Pre-Tax NPV 8% of $1.257 B and a Pre-Tax IRR of 48.2% for Its Rose Lithium Project

/EINPresswire.com/ -- MONTREAL, QUEBEC--(Marketwired - Sep 6, 2017) - Critical Elements Corporation (the "Company" or "Critical Elements") (TSX VENTURE:CRE)(OTCQX:CRECF)(FRANKFURT:F12) is pleased to announce results of a Feasibility Study on the Rose Lithium-Tantalum project ("Rose" or the "Project") in James Bay, Québec. Unless otherwise stated, all figures are quoted in Canadian dollars ("$") and are reported on a 100% equity project basis.

Highlights

- Average annual production of 186,327 tonnes of chemical grade lithium concentrate

- Average annual production of 50,205 tonnes of technical grade lithium concentrate

- Average annual production of 429 tonnes of tantalum concentrate

- Expected life of mine of 17 years

- Average operating costs of $66.56 per tonne milled, $458 (US$344) per tonne of concentrate (all concentrate production combined)

- Estimated initial capital cost $341.2 million before working capital

- 100% equity basis for project

- Average gross margin 63.6%

- After-tax NPV of $726 million (at 8% discount rate), after-tax IRR of 34.9% and price assumption of US$1,500 per tonne technical grade lithium concentrate, US$750 per tonne chemical grade lithium concentrate, US$130 per kg tantalum pentoxide

- Anticipated construction time to start of production of 21 months

"The feasibility study is a major milestone for Critical Elements, which explains our superior competitive situation. The excellent gross margin is a key indicator for the quality of this project," said Dr. Steffen Haber, President of Critical Elements Corporation.

"I'm very pleased with the delivery and the results of the most important milestone of Critical Elements to date," said Jean-Sébastien Lavallée, CEO and Chairman of the Board. "I would like to thank the joint effort of our team to deliver a very strong feasibility study that shows a very solid project."

The Rose Lithium-Tantalum Project is 100% owned by Critical Elements. The company's market strategy is to enter the lithium market with a low-risk approach. The completion of the feasibility on the spodumene plant is the first step to enter the market and establish the company as a reliable high quality lithium supplier. The low-risk approach is characterised by simple open-pit mining and conventional lithium processing technologies.

The feasibility is based on a conventional truck and shovel open pit operation and a conventional milling process to produce technical and chemical grade spodumene concentrates and a tantalite concentrate.

The mine will excavate a total of 26.8M tonnes ore grading an average of 0.85% Li2O and 133 ppm Ta2O5 after dilution. The mill will process 1.61M tonnes of ore per year to produce an annual average of 236,532 tonnes of technical and chemical grade spodumene concentrates and 429 tonnes of tantalite concentrate.

The ore is contained in several parallel and continuous low dipping pegmatite veins outcropping on surface. The ore zones are open at depth and a future underground operation is possible.

Over the life of mine, the open pit will excavate a total of 182.4M tonnes of waste rock and 11.0 M tonnes of overburden. The average strip ratio is 7.2 tonnes of stripping per tonne of ore.

The environmental and social impact study was submitted to the federal and provincial environmental agencies at the end of July. Permitting is expected to take 18 months. During this time, Critical Elements will carry out detailed engineering, select the construction contractors, and purchase long lead time items. Construction and start-up is expected to take 21 months. Construction is expected to commence Q4 2018 while commercial production is expected to commence in Q3 2020. The Rose project will have a peak of 575 employees during construction and an average of 290 employees for commercial production.

Table 1: Rose Key FS Results

| Item | Units | Value | ||

| Production | ||||

| Project life (from start of construction to closure) | years | 19 | ||

| Mine life | years | 17 | ||

| Total mill feed tonnage | M t | 26.8 | ||

| Average mill feed grade | ||||

| Li2O | % Li2O | 0.85 | ||

| Ta2O5 | ppm Ta2O5 | 133 | ||

| Lithium Concentrate Production | ||||

| % of Production, Chemical Grade | % | 75 | ||

| % of Production, Technical Grade | % | 25 | ||

| Mill recoveries | ||||

| Li2O, Chemical Grade | % | 90 | ||

| Li2O, Technical Grade | % | 87 | ||

| Ta2O5 | % | 40 | ||

| Payable | ||||

| 5% Li2O Concentrate, Chemical Grade | t | 3,070,000 | ||

| 6% Li2O Concentrate, Technical Grade | t | 827,000 | ||

| Ta2O5 contained in concentrate | kg | 1,431,000 | ||

| Commodity Prices | ||||

| 5% Li2O Concentrate, Chemical Grade FOB port | US$/t conc. | 750 | ||

| 6% Li2O Concentrate, Technical Grade FOB port | US$/t conc. | 1,500 | ||

| Ta2O5 contained in concentrate FOB mine site | US$/kg contained | 130 | ||

| Exchange rate | 1 US$: | 1.33 CAN$ | ||

| 0.75 US$: | 1 CAN$ | |||

| Project Costs | CA$ | US$ | ||

| Average Mining Cost | $/t milled | 30.69 | 23.02 | |

| Average Milling Cost | $/t milled | 16.14 | 12.11 | |

| Average General & Administrative Cost | $/t milled | 12.15 | 9.12 | |

| Average Concentrate Transport Costs | $/t milled | 7.57 | 5.68 | |

| Project Economics | CA$ | US$ | ||

| Gross Revenue | $M | 4,973 | 3,729 | |

| Total Selling Cost Estimate | $M | 152 | 114 | |

| Total Operating Cost Estimate | $M | 1,785 | 1,339 | |

| Total Sustaining Capital Cost Estimate | $M | 127 | 95 | |

| Total Capital Cost Estimate | $M | 341 | 256 | |

| Duties and Taxes | $M | 1,000 | 750 | |

| Pre-Tax Cash Flow | $M | 2,567 | 1,926 | |

| After-Tax Cash Flow | $M | 1,567 | 1,175 | |

| Effective tax rate | 39% | |||

| Discount Rate | 8% | |||

| Pre-Tax Net Present Value @ 8% | $M | 1,257 | 943 | |

| Pre-Tax Internal Rate of Return | 48.2% | |||

| Pre-Tax Payback Period | years | 2.3 | ||

| After-Tax Net Present Value @ 8% | $M | 726 | 545 | |

| After-Tax Internal Rate of Return | 34.9% | |||

| After-Tax payback period | years | 2.8 | ||

Property

The Rose property is located in northern Québec's administrative region, on the territory of Eeyou Istchee James Bay. It is located on Category III land, on the Traditional Lands of the Eastmain Community, approximately 40 kilometers north of the Cree village of Nemaska. The latter is located approximately 300 km north-west of Chibougamau.

The Rose property is accessible by road via the Route du Nord, usable all year round from Chibougamau. The mine site can also be reached by Matagami, via Route 109 and Route du Nord. Figure 1 shows the regional location of the project. The project is located 80 km south of Goldcorp's Éléonore gold mine and 45 km north-west of Nemaska's Whabouchi lithium project and 20 km south of Hydro Québec's Eastmain 1 hydroelectricity generating plant. The Nemiscau airport services the regions air travel needs. The Rose property site is located 50 km by road from the Nemiscau airport.

The Rose property comprises 500 claims spread over a 26,100 ha area. Geologically, the Rose property is located at the north-east end of the Archean Lake Superior Province of the Canadian Shield.

To view Figure 1 – Rose Property Location: http://media3.marketwire.com/docs/1_Rose_Property_Location.jpg

{kind=link}

Reserve Estimate

A Mineral Reserve Estimate for 17 mineralized zones was prepared during this study. The estimation assumed the production of a chemical grade spodumene concentrate with a price of 15.66 US$ per kg Li2O and a tantalite concentrate with a price of 130 US$ per Ta2O5. The recoveries were fixed at 85% and 64% for Li and Ta respectively. The grade-recovery curve used for resource estimate, which became available after the mineral reserves were evaluated, was verified and found to have little influence on the reserve estimate. The production of a higher value technical grade spodumene concentrate was not assumed in the reserve estimate.

Based on compilation status, metal price parameters, and metallurgical recovery inputs, the effective date of the estimate is August 4, 2017.

The estimate was prepared in accordance with CIM's standards and guidelines for reporting mineral resources and reserves.

Table 2 displays the results of the Mineral Reserve Estimate for the Rose Project at the $29.7 NSR per tonne cut-off for the open-pit scenario.

Table 2 - Mineral Reserve Estimate

| Tonnage | NSR | Li2O_eq | Li2O | Ta2O5 | |

| Category | (Mt) | ($) | (%) | (%) | (ppm) |

| Probable | 26.8 | 148.99 | 0.96 | 0.85 | 133 |

| Total | 26.8 | 148.99 | 0.96 | 0.85 | 133 |

- The Independent and Qualified Person for the Mineral Reserve Estimate, as defined by NI 43-101, is Patrick Frenette, P.Eng, M.Sc.A, of InnovExplo Inc. The effective date of the estimate is August 4, 2017.

- The model includes 17 mineralized zones.

- Calculations used metric units (metres, tonnes and ppm).

- The number of metric tons was rounded to the nearest thousand. Any discrepancies in the totals are due to rounding effects. Rounding followed the recommendations in NI 43-101.

- InnovExplo is not aware of any known environmental, permitting, legal, title-related, taxation, socio-political, marketing or other relevant issue that could materially affect the Mineral Reserve Estimate.

Resource Estimate

InnovExplo updated the mineral resource estimate from the 2011 PEA for 23 mineralized zones. The mineral resource was updated on a block value basis using current pricing and cost parameters.

The effective date of the estimate is August 29, 2017, based on compilation status, metal price parameters, and metallurgical recovery inputs.

Given the density of the processed data, the search ellipse criteria, the drill hole density and the specific interpolation parameters, InnovExplo is of the opinion that the current mineral resource estimate can be classified as Indicated and Inferred resources. The estimate was prepared in accordance with CIM's standards and guidelines for reporting mineral resources and reserves.

Table 3 displays the results of the Mineral Resource Estimate for the Rose Project using $30 NSR per tonne cut-off for the open-pit mine and $110 NSR cut-off for the underground mine.

Table 3 – Mineral Resource Estimate

| Tonnage | NSR | Li2O_eq | Li2O | Ta2O5 | ||

| Category | (Mt) | ($) | (%) | (%) | (ppm) | |

| Pit-constrained | 30.0 | 161 | 1.04 | 0.93 | 150 | |

| Indicated | Underground | 1.9 | 159 | 1.02 | 0.94 | 114 |

| Total Indicated | 31.9 | 161 | 1.04 | 0.93 | 148 | |

| Pit-constrained | 2.0 | 137 | 0.90 | 0.79 | 153 | |

| Inferred | Underground | 0.8 | 149 | 0.96 | 0.88 | 126 |

| Total Inferred | 2.8 | 141 | 0.92 | 0.82 | 145 |

- The Independent and Qualified Person for the Mineral Resource Estimate, as defined by NI 43-101, is Pierre-Luc Richard, P.Geo., M.Sc., of InnovExplo Inc. The effective date of the estimate is August 29, 2017.

- These Mineral Resources are not Mineral Reserves as they do not have demonstrated economic viability.

- The model includes 23 mineralized zones.

- Results are presented in situ and undiluted.

- Sensitivity was assessed using cut-off NSR values for $5-10 increments from $20 to $150. The mineral resource is reported at a cut-off of $30 NSR for the open-pit and of $110 NSR for the underground potential based on market conditions (metal price, exchange rate and production cost).

- A range of densities was used on a per-zone basis based on statistical analysis of all available data.

- A minimum true thickness of 2.0 metres was applied, using the grade of the adjacent material when assayed or a value of zero when not assayed.

- High grade capping was done on raw assay data based on the statistical analyses of individual mineralized zones.

- Compositing was done on drill hole intercepts falling within mineralized zones (composite lengths vary from 1.5 m to 3 m in order to distribute the tails adequately).

- Resources were evaluated from drill holes using a 2-pass OK interpolation method in a block model (block size = 5 m x 5 m x 5 m).

- The inferred category is only defined within the areas where blocks were interpolated during pass 1 or pass 2 where continuity is sufficient to avoid isolated blocks being interpolated by only one drill hole. The indicated category is only defined by blocks interpolated by a minimum of two drill holes in areas where the maximum distance to the closest drill hole composite is less than 40 metres for blocks interpolated in pass 1.

- The number of metric tons was rounded to the nearest thousand. Any discrepancies in the totals are due to rounding effects. Rounding followed the recommendations in NI 43-101.

- InnovExplo is not aware of any known environmental, permitting, legal, title-related, taxation, socio- political, marketing or other relevant issue that could materially affect the Mineral Resource Estimate.

Feasibility Study

The parameters used for the feasibility study are the following:

- Open pit mining rate of 1,610,000 tpy

- Spodumene process plant with a 4,900 tpd nominal capacity

Mining Operation

The mineralization is hosted within outcropping pegmatite dykes subparallel to surface. The ore body is relatively flat, close to surface and comprised of north oriented stacked lenses. Mineralization recognized to date on the Rose property includes rare element of Lithium-Cesium-Tantalum or LCT-type pegmatites and molybdenum occurrences.

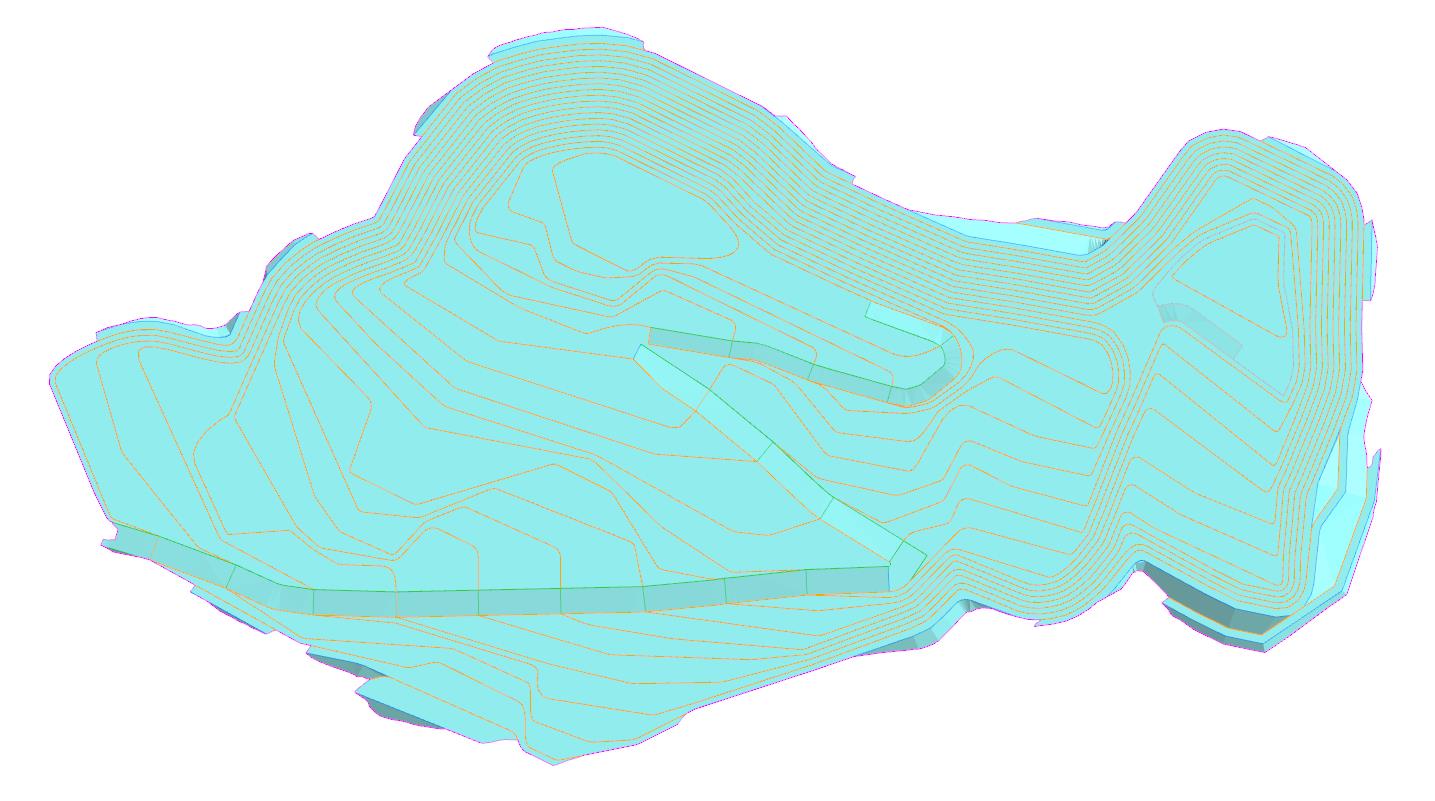

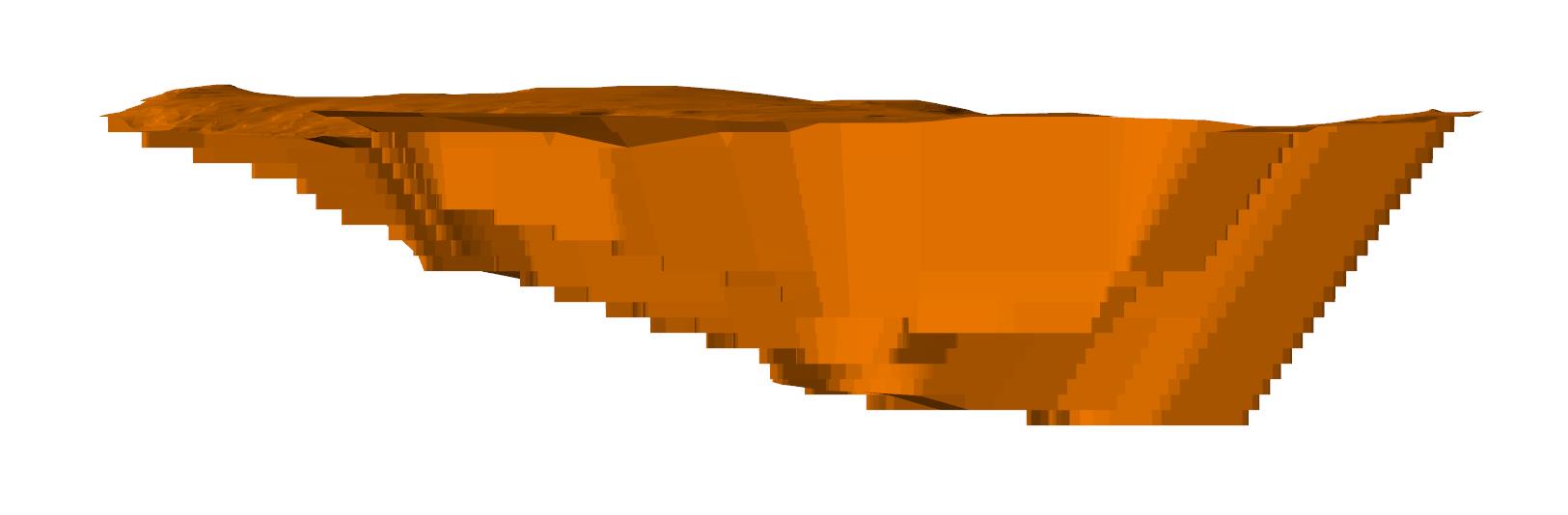

A conventional truck and shovel open-pit approach was considered to mine the Rose Lithium-Tantalum Project's Probable Mineral Reserves. The dimensions of the engineered pit design are approximately 1,620m long x 900m wide x 200m deep.

The life of mine plan (LOM) proposes to mine 26.8 Mt of ore, 182.4 Mt of waste, and 11.0 Mt of overburden for a total of 220.2 Mt of material. The average stripping ratio is 7.2 tonnes of stripping per tonne of ore. The nominal production rate is estimated at 4,600 tonnes per day and 350 operating days per year.

The mining operation production rate is set to approximately 15 Mt of material per year. An open pit mining schedule was planned and resulted in a mine life of 17 years.

Contract mining will be used for the removal of the overburden while Critical Elements will undertake the mining of all hard rock material with its own equipment fleet and operators.

The main production fleet will consist of one (1) backhoe excavator, one (1) electric front shovel, one (1) wheel loader, seven (7) haul trucks (65t), seven (7) haul trucks (135t), two (2) rotary drills, one (1) DTH drill, two (2) bulldozers, one (1) wheel dozer, two (2) graders, and two (2) water trucks.

The Rose project pit was designed with a 10m single benching arrangement. A 57° inter-ramp angle and an overall pit slope angle of 55° were utilized for the ultimate pit design. A berm width of 7.0m corresponding to the recommended overall slope angle was used. The pit slopes in overburden have a face ratio of 2.5:1 with a 10m berm width.

The main in-pit haulage ramp is designed at 30.9m wide to allow a double-lane traffic, except for the last benches at the pit bottom that are designed at 20.4m wide for single lane traffic. A 2m drainage ditch is included to allow for water drainage and pipe installation. The maximum gradient of the inner curvature of all ramp segments is 10%.

To view Figure 2 - Rose Pit Plan View: http://media3.marketwire.com/docs/2_Rose_Pit_Plan.jpg

{kind=link}

To view Figure 3 - Rose Pit Side View Looking West: http://media3.marketwire.com/docs/3_Rose_Pit_Side.jpg

{kind=link}

Mineral Processing

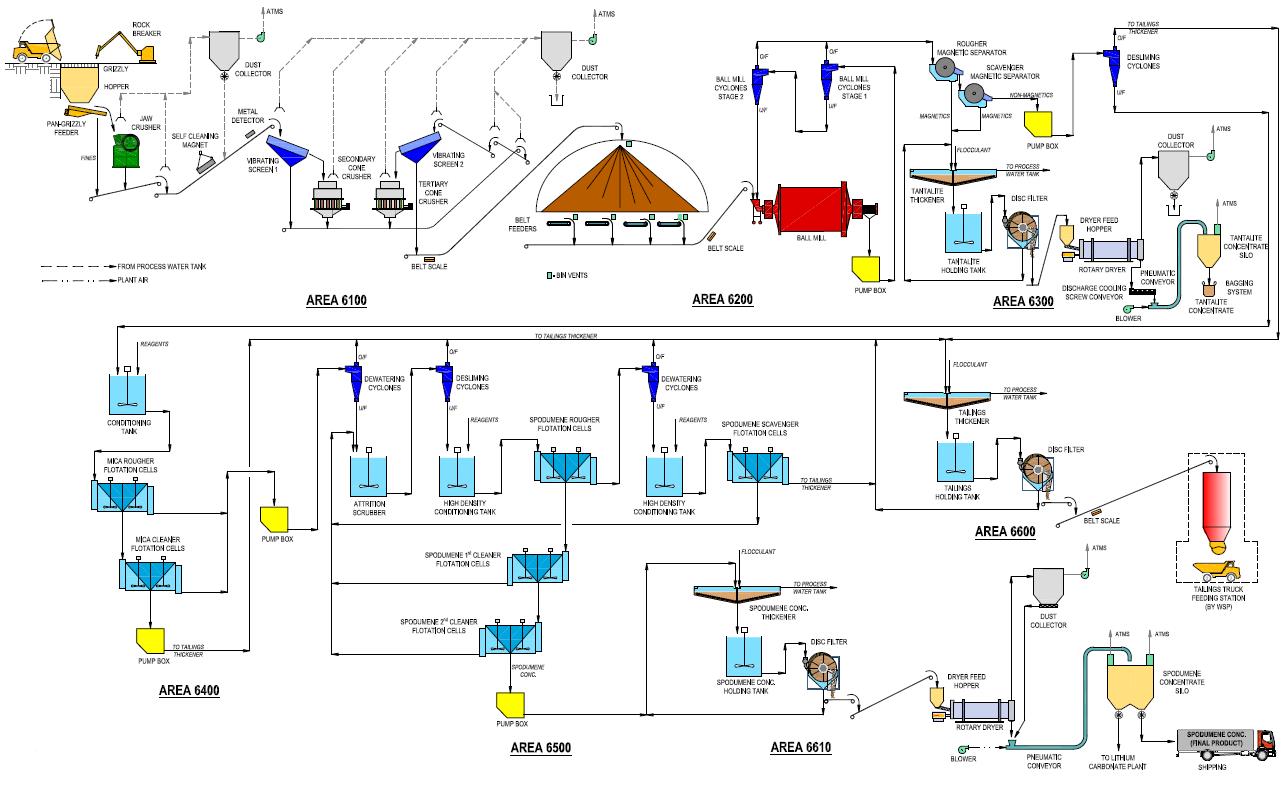

A standard froth flotation process will be utilized to produce technical grade and chemical grade lithium concentrates and a tantalum concentrate. The mineral process plant will consist of crushing, beneficiation, and dewatering areas. The technical grade lithium concentrate will grade 6.0% Li2O while the chemical grade lithium concentrate will grade 5.0% Li2O. The tantalum concentrate will grade 20% Ta2O5.

The beneficiation process includes crushing, grinding, magnetic separation and flotation. The crushing circuit will consist of a jaw crusher and two (secondary and tertiary) cone crushers, and screens. The crushed ore will have a P80 of 13mm and will be stockpiled in a 9,200 tonnes capacity dome; this is sufficient for approximately two days of mill operation. The grinding circuit will consist of a ball mill operating in a closed circuit and a two-stage cyclone cluster. The tantalum will first be recovered at a grade of 2.0% Ta2O5 by high intensity magnetic separation then upgraded further to 20.0% Ta2O5 by gravity separation. The tantalum concentrate will then be thickened, vacuum filtered, dried to 1% moisture and bagged, ready for shipping. The lithium flotation circuit will remove slimes, separate mica, and purify the lithium to the required grade. The spodumene concentrate will then be thickened, vacuum filtered, dried to 1% moisture, and stored in 1500 tonne silo from where it can be bulk loaded into trucks. The tailings will be thickened, vacuum filtered to 15% moisture, and trucked to the waste rock / tailings piles where it will be dry stacked.

The spodumene plant will operate 24 hours per day, seven (7) days per week, and 52 weeks per year. The process plant was designed with an operating availability of 90%. The crushing circuit was designed using an operating availability of 50%. The concentrator capacity has been established at a nominal throughput rate of 4 900 dry tonnes per day. The plant has a capacity of 1,610,000 per year.

The process plant flowsheet developed by Bumigeme Inc. is presented in Figure 4.

To view Figure 4: Rose Process Flowsheet: http://media3.marketwire.com/docs/4_Rose_Process_Flowsheet.jpg

{kind=link}

Metallurgy

Bench scale metallurgical testing was performed at ACME Metallurgical Limited in Vancouver in 2011. The results from these tests were used for the PEA study. Three composites; the Rose (main structure), the Rose Sud-Est (Southeast structure) and Tantalum (secondary structure with higher tantalum and lower lithium content) were subjected to various metallurgical tests.

SGS Canada Inc. in Lakefield conducted tests from 2013 to 2015 to improve lithium and tantalum recoveries. In 2015 SGS Canada Inc. developed a conceptual flowsheet based on a series of bench scale tests on various samples from the Rose deposit. The proposed flowsheet is comprised of conventional three-stage crushing and single stage grinding followed by magnetic separation for the recovery of tantalum, mica flotation, and spodumene flotation. This flowsheet was the basis of the process plant design.

SGS Canada also conducted a pilot plant program in early 2017 on two samples from the Rose project (Rose and Rose South). The main objective of the pilot plant program was to generate spodumene concentrate for testing in a lithium carbonate pilot plant which was conducted by Outotec in Germany and Finland. Secondary objectives were to prove metallurgical performance on a continuous pilot scale and to generate metallurgical and operating data for further studies. The spodumene pilot plant demonstrated the robustness of the design process.

The feasibility study assumes 87.3% and 90% recovery for technical and chemical grade lithium concentrates respectively and 40% recovery for the tantalum concentrate.

Process water will be recycled releasing minimal amounts to the equalization pond and final effluent treatment plant.

To view Bulk sampling for pilot plant work: http://media3.marketwire.com/docs/Bulk_sampling_for_pilot_plant_work.jpg

{kind=link}

Environmental and Social Impact Assessment

Baseline environmental studies were initiated in the spring 2011. In 2016, various studies were undertaken in order to update the 2011 data and to obtain the baseline information that is required to assess the project's impacts within the Environmental and Social Impact Assessment ("ESIA") of the Rose mine Project. In total, eleven different sectorial studies were completed documenting the following components:

| - | Hydrology | |

| - | Surface Water and Sediments | |

| - | Terrestrial fauna | |

| - | Aquatic fauna | |

| - | Artificial light at night | |

| - | Landscape | |

| - | Environmental Site Assessment - Phase I | |

| - | Vegetation | |

| - | Greenhouse gas | |

| - | Noise (including modelling) | |

| - | Archeology | |

| - | Air quality (including modelling) |

One study is currently ongoing for the hydrogeological environmental component.

The baseline study was completed and the ESIA was submitted to the Canadian Environmental Assessment Agency (CEAA) and the Ministère du Développement durable, de l'Environnement, et de la Lutte contre les changements climatiques (MDDELCC) of the Québec Province on July 28th, 2017. The ESIA included preliminary information regarding Hydrogeology and will be updated when modelling is completed.

Critical Elements has been working since the beginning with the Eastmain Community, on whose lands the Project lies. The company has also maintained good relations with the Grand Council of the Cree and with the neighbouring Nation of Nemaska. Consultations have been ongoing and are planned throughout the life of the Project.

The filing of the ESIA to the Federal and Provincial Authorities is the core of the Evaluation Process. The process of acquiring the required authorizations is expected to take 18 months. No major obstacles are anticipated.

Infrastructure

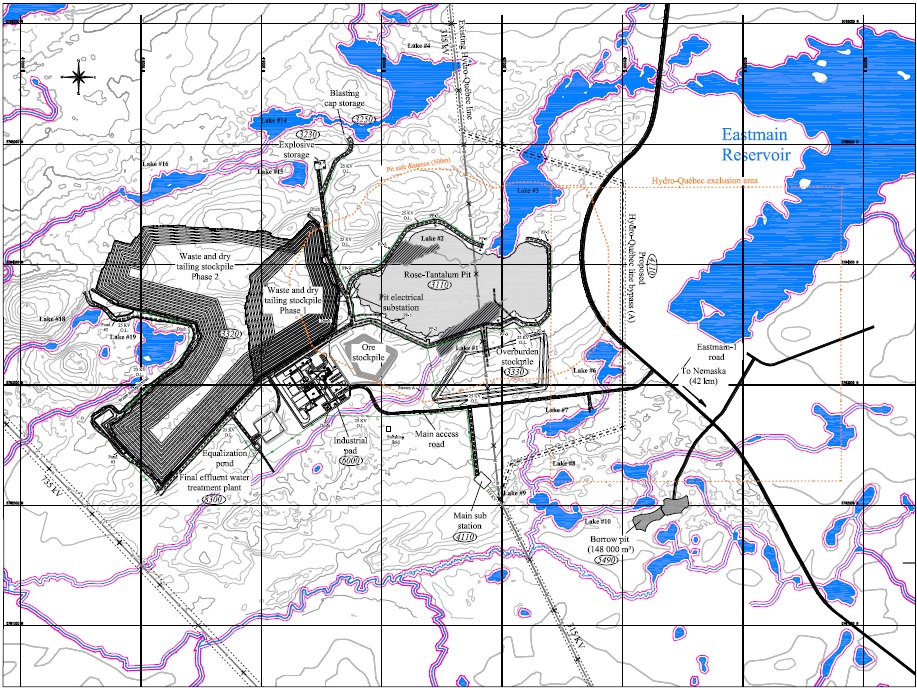

The project infrastructure includes site main services and haulage roads, explosive and detonator storage, a spodumene processing plant, a pit equipment maintenance facility, a warehouse, diesel and gasoline storage, LNG storage and distribution, ore stockpile pad, waste rock and dry tailings stockpile, overburden stockpile, main electrical substation and distribution, fresh and potable water supply, sewage, surface water management, final effluent treatment, communication system, gate house, and an administrative building. A lithium carbonation plant is not included in the feasibility study, but additional space is provided on the industrial pad and services are planned for future installation.

The mine site layout is shown in figure 5.

To view Figure 5 - Rose Site Layout: http://media3.marketwire.com/docs/5_Rose_Site_Layout.jpg

{kind=link}

Waste rock and tailings samples were analysed at the SGS Canada's laboratory in Lakefield and both were found to be non-acid generating. The dry tailings and the waste rock will be stored in the same facility which has sufficient capacity for the life of mine. Rain and melt water will be collected in ditches and pumped to the water treatment plant.

The ore pad will have a 3.9M tonne capacity where low grade material may be stored.

The industrial pad has an area of 296,000 m2 and will contain the process plant, the maintenance facility, warehouse, administration building, diesel and gasoline storage tanks, LNG storage and distribution, and all associated services. LNG will be used for buildings heating and for the drying of the lithium and tantalum concentrates. The LNG facility will be in place for the kiln of a lithium carbonate plant if required, necessitating the addition of only one additional reservoir.

The hydrology study has suggested that water inflow to the open pit is to be expected. In order to maximize pit slopes, water wells will be constructed around the pit periphery to lower the water table below the pit floor. One of these wells will be used to supply the mine site with fresh water. Water from the other wells will be directed directly to the final effluent.

Impacted water from the waste rock / dry tailings pad, the open pit, the industrial pad, and roads will be collected in an equalization pond and treated before being released as final effluent.

The mine site will have a 2.7 km main access road from the Eastmain 1 road to the industrial pad. Including the service roads, the site will total 15.8 km of roads.

Electricity will be provided by Hydro-Québec. A 315 kV electrical transport line (L3176), owned by Hydro- Québec, runs North-South over the eastern side of the Rose Property. It runs over the planned open pit. The portion running over the open pit will be rerouted to allow open pit operation. Critical Elements and Hydro-Québec have signed an agreement to conduct a technical study for the supply of electricity to the mine and the rerouting of the power line. Hydro-Québec is currently conducting this study. In a previous study Hydro-Québec provided costs for preparation work in supplying electrical power and for the rerouting of the power line which is to be incurred by the mine. These costs were incorporated in the FS. The schedule of the power line relocation fits with Critical Elements construction schedule such that electrical power will be available from the main grid in time for the mill commissioning and start-up. The 315kV power line reroute will total 4.2 km.

The power demand for the project has been estimated at about 13,486 kW (15,615 kVA) and a reserve of up to 20 MVA has been accepted by Hydro-Québec. Two 15 MW transformers will operate at the same time to feed the site and the processing plant. The transformers will feed the 25 kV mine site electrical network. Power lines are necessary to feed the processing plant, the industrial pad, the final water treatment plant, the open pit and wells, the pumps at the waste rock / dry tailings water collecting ponds, and the explosives and detonator storage facilities. A total of 15.5 km of power lines are planned.

To view Power line at Rose site: http://media3.marketwire.com/docs/Power_line_at_Rose_site.jpg

{kind=link}

Capital Costs

The capital and operating costs were estimated in Canadian dollars. An economic analysis was conducted with a discounted cash-flow before and after tax. The initial capital cost is estimated at CA$341.2M including all infrastructures described earlier with a 10% contingency. The sustaining capital is estimated at CA$126.8M over the life of mine.

The total payable products are estimated at 3,070,006 tonnes of chemical grade Li2O concentrate, 827,196 tonnes of technical grade Li2O concentrate, and 7,157 tonnes of Ta2O5 concentrate.

Table 4 - Initial Capital and Sustaining Capital Costs

| Initial | Sustaining | Initial | Sustaining | |

| Item | Capital | Capital | Capital | Capital |

| M CA$ | M CA$ | M US$ | M US$ | |

| Direct Capital Estimate | 235.1 | 93.8 | 176.3 | 70.4 |

| Mining | 49.3 | 89.5 | 37.0 | 67.1 |

| Power & Electrical | 27.8 | 0.6 | 20.8 | 0.4 |

| Infrastructure | 36.7 | 0.0 | 27.5 | 0.0 |

| Process plant | 111.9 | 0.0 | 83.9 | 0.0 |

| TSF and Water management | 9.5 | 3.8 | 7.1 | 2.8 |

| Indirect Capital Estimate | 74.9 | 0.4 | 56.2 | 0.3 |

| Administration & Overhead | 32.2 | 0.0 | 24.1 | 0.0 |

| Project Development (Studies) | 0.4 | 0.0 | 0.3 | 0.0 |

| PCM, Other indirects & Other costs | 42.3 | 0.4 | 31.7 | 0.3 |

| Contingency | 31.0 | 9.4 | 23.2 | 7.1 |

| Mine Rehabilitation (incl. contingency) | 0.0 | 17.8 | 0.0 | 13.4 |

| Mine Rehabilitation Bond | 0.2 | 5.4 | 0.1 | 4.0 |

| Total Capital Estimate | 341.2 | 126.8 | 255.9 | 95.1 |

Operating Costs

The operating costs are estimated at $66.56 per tonne of ore processed which include:

| - | Mining | $30.69 per tonne processed | |

| - | Processing | $16.14 per tonne processed | |

| - | G&A | $12.15 per tonne processed | |

| - | Concentrate transportation | $ 7.57 per tonne processed |

The operating costs are estimated at $458/tonne (US$344/tonne) of concentrate as summarized in table 5.

Table 5 – Operating Costs per tonne of concentrate

| Item | CA$/t Li2O concentrate |

US$/t Li2O concentrate |

| Mining | 211 | 158 |

| Processing | 111 | 83 |

| General and Administration | 84 | 63 |

| Transportation Concentrate | 52 | 39 |

| Total Operating Costs | 458 | 344 |

| SG&A | 26 | 20 |

| Royalties | 13 | 10 |

| Total Operating Costs (w. SG&A and Royalties) | 497 | 373 |

| Less: Tantalite Credit | 48 | 36 |

| Total Operating Costs (after tantalite credit) | 449 | 337 |

Energy unit costs are $0.05 per kWh for electricity, $0.95 per litre for diesel, and $0.546 per m3 for LNG.

Project Economics

The mine will process 1,610,000 tonnes ore per year grading an average of 0.85% Li2O and 133 gpt Ta2O5 over a period of 17 years. The price assumptions are US$750 per tonne and US$1,500 per tonne of chemical grade and technical grade lithium concentrates respectively (FOB port) and US$130 per kg Ta2O5 contained in the tantalum concentrate (FOB mine site). The pre-tax and after-tax NPV at various discount rates are presented in table 6.

Table 6 - Pre-Tax and After-Tax NPV

| Discount | Pre-Tax | After-Tax | Pre-Tax | After-Tax |

| Rate | M CA$ | M CA$ | M US$ | M US$ |

| NPV @ 0% | 2,567 | 1,567 | 1,926 | 1,175 |

| NPV @ 5% | 1,620 | 960 | 1,215 | 720 |

| NPV @ 8% | 1,257 | 726 | 943 | 545 |

| NPV @ 10% | 1,070 | 605 | 802 | 454 |

| NPV @ 12% | 914 | 504 | 686 | 378 |

The after tax internal rate of return is 34.9%.

Sensitivity Analysis

The sensitivity of the NPV to exchange rate and chemical grade lithium concentrate price is presented in table 7.

Table 7 - After-Tax NPV Sensitivity to exchange rate and chemical grade lithium concentrate

| After-Tax NPV @ 8% Discount Rate - M CA$ | |||||

| Exchange Rate | Li2O Price - Chemical Grade | ||||

| USD/CAD | 720 US$/t | 810 US$/t | Base Case | 990 US$/t | 1080 US$/t |

| 0.70 | 798M CA$ | 923M CA$ | 840M CA$ | 1,172M CA$ | 1,296M CA$ |

| Base Case | 687M CA$ | 805M CA$ | 726M CA$ | 1,038M CA$ | 1,154M CA$ |

| 0.80 | 590M CA$ | 701M CA$ | 627M CA$ | 920M CA$ | 1,030M CA$ |

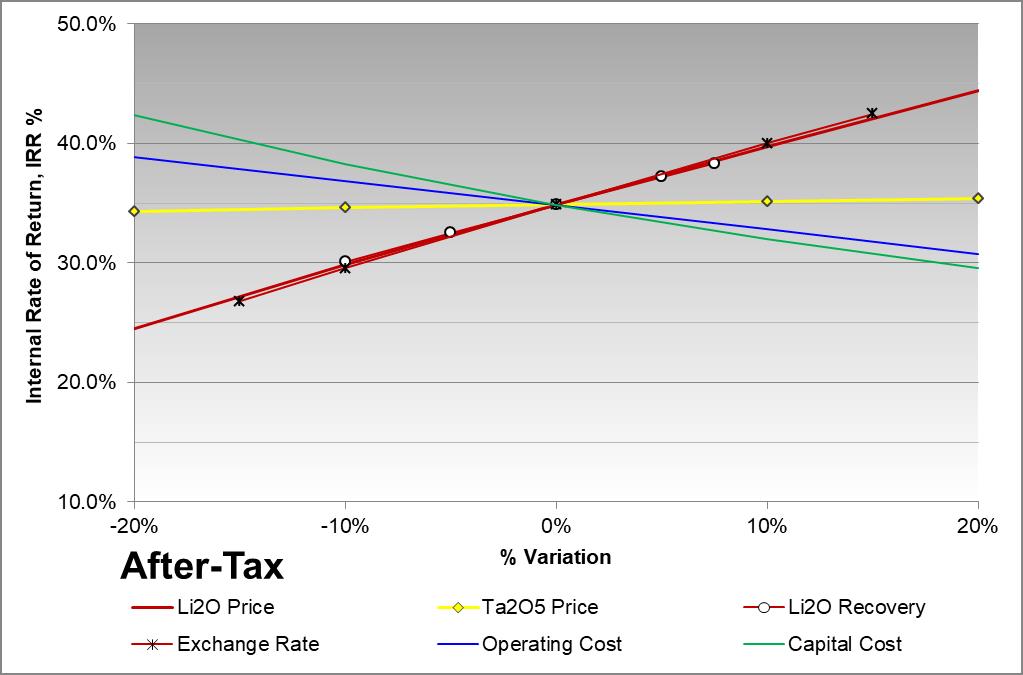

Figures 6 and 7 present the sensitivity the NPV at 8% discount rate and IRR to prices, Li2O recovery, exchange rate, operating costs, and capital cost. The economics are most sensitive to Li2O price, exchange rate, and Li recovery.

To view Figure 6 - Sensitivity on After-Tax NPV 8%: http://media3.marketwire.com/docs/6_Sensitivity_on_After-Tax_NPV.jpg

{kind=link}

To view Figure 7 - Sensitivity on After-Tax IRR: http://media3.marketwire.com/docs/7_Sensitivity_on_After-Tax_IRR.jpg

{kind=link}

Lithium Demand Outlook

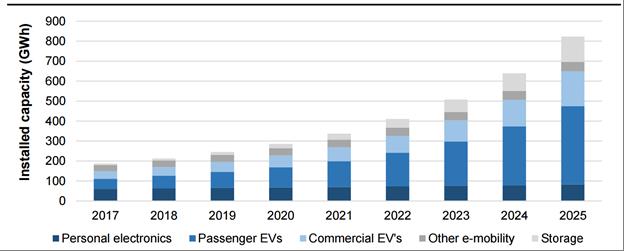

The future growth of the lithium market will clearly be dominated by e-mobility powered by Li-ion batteries but also increasingly energy storage systems (ESS). With the declining cost of Li-cells, targets for 1 kWh being now very close to 150 USD, they are also becoming attractive for use in private installations combined with increasing use of photovoltaic roof-top electricity generation (PV).

In Germany a new regulation demands that for all PV projects exceeding 1MW power generation an energy storage system has to be installed by 2025. This is in order to avoid peak energy stressing the electricity distribution systems, a phenomenon which already pushes European systems to their limits during the summer months and increasingly so with the ongoing addition of new PV systems, be they commercial or private.

The German Automobile Manufacturers Association (VDA) considers an electric vehicle penetration rate of 15% to 25% being possible by 2025. The lower range for market penetration of 15% corresponds to some 15 million cars or if we assume a market of 100 million cars by 2025 and an average of 30 kg of LCE needed for the battery 450,000 MT of LCEs required for this segment alone.

Canaccord Genuity Research, amongst others, assumes that the overall share of electric vehicles (EV) will climb to over 50% of all Li-ion batteries installed, i.e. being the driver of the expanding lithium market. The absolute growth numbers from Canaccord's forecast are higher than previous assumptions, however, in line of some forecasts from OEMs.

The current growth assumptions will if they materialize, lead to a lithium demand requirement of approximately. 750,000t of LCE. This is an additional 550,000t of LCE required from 2017 till 2025 or the equivalent of almost 70,000t per year of LCE.

In Figure 8 the individual sectors growth are described.

To view Figure 8: Lithium Ion Battery Installed Shares of Application: http://media3.marketwire.com/docs/8_Lithium%20Ion%20Battery_Installed.jpg

{kind=link}

Source: Canaccord Genuity Research (Battery Materials Update, report June 2017)

Lithium Price Outlook

In 2017, off take agreements for spodumene CG with a Lithium oxide content between 5.0 and 6.0% have been executed, whereby 120,000t of 5.5% spodumene concentrate has been contracted at US$830/t FOB. Every additional 0.1% of Li2O content will garner a premium of US$15/t, enabling prices between 750 US$/mt and 905 US$/mt for spodumene CG 5.0 and 6.0. Also, suppliers who are able to provide a higher quality spodumene CG yielding lower conversion cost will also be able to achieve higher prices.

The market for spodumene TG is a specialty chemicals market, which addresses the specific needs for customers in the glass and ceramic industry. Historically, prices have been reflecting the higher value of iron free spodumene like in Lithium carbonate and specific properties of the crystalline material.

Therefore, pricing for spodumene TG is directly linked to the Lithium oxide content in Lithium carbonate.

Ongoing Work

The Environmental and Social Impact Assessment of the project is being reviewed by the Canadian Environmental Assessment Agency (CEAA) and the Ministère du Développement Durable, de l'Environnement, et de la Lutte contre les changements climatiques (MDDELCC) of the Province of Québec.

Consultations with the local communities are ongoing and will continue for the life of the mine.

Critical Elements is proceeding to the detailed engineering phase of the project.

The hydrogeology model of the mine site is being calibrated and will be completed shortly.

Report Filing

The Company plans to file an NI 43-101 technical report that summarizes the Rose Lithium-Tantalum project on SEDAR (http://www.sedar.com) and on the Company's website (http://www.cecorp.ca/en/) within 45 days.

Qualified Persons

The feasibility study was prepared in accordance to 43-101 standards by WSP, Bumigeme inc, InnovExplo Inc., and Gerritt Fuelling. InnovExplo Inc was responsible for the resource estimate and the mine plan, Bumigeme Inc was responsible for the mineral processing, WSP was responsible for environmental study, project infrastructure, financial modelling, and report integration. Mr. Gerrit Fuelling was responsible for the market study.

The qualified persons for the study are:

| InnoExplo Inc ; | ||

| - | Pierre-Luc Richard, P.Geo, geologist | |

| - | Patrick Frenette, Eng, mining engineer | |

| Bumigeme; | ||

| - | Florent Baril, Eng, metallurgical engineer | |

| WSP; | ||

| - | Eric Poirier, Eng, electrical engineer | |

| - | Olivier Joyal, geologist | |

| - | Philippe Rio Roberge, Eng, civil engineer | |

| Others; | ||

| - | Gerrit Fuelling, mining engineer | |

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is described in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Investor relations:

Jean-Sebastien Lavallee, P. Geo.

Chairman and CEO

819-354-5146

jslavallee@cecorp.ca

www.cecorp.ca

Paradox Public Relations

514-341-0408